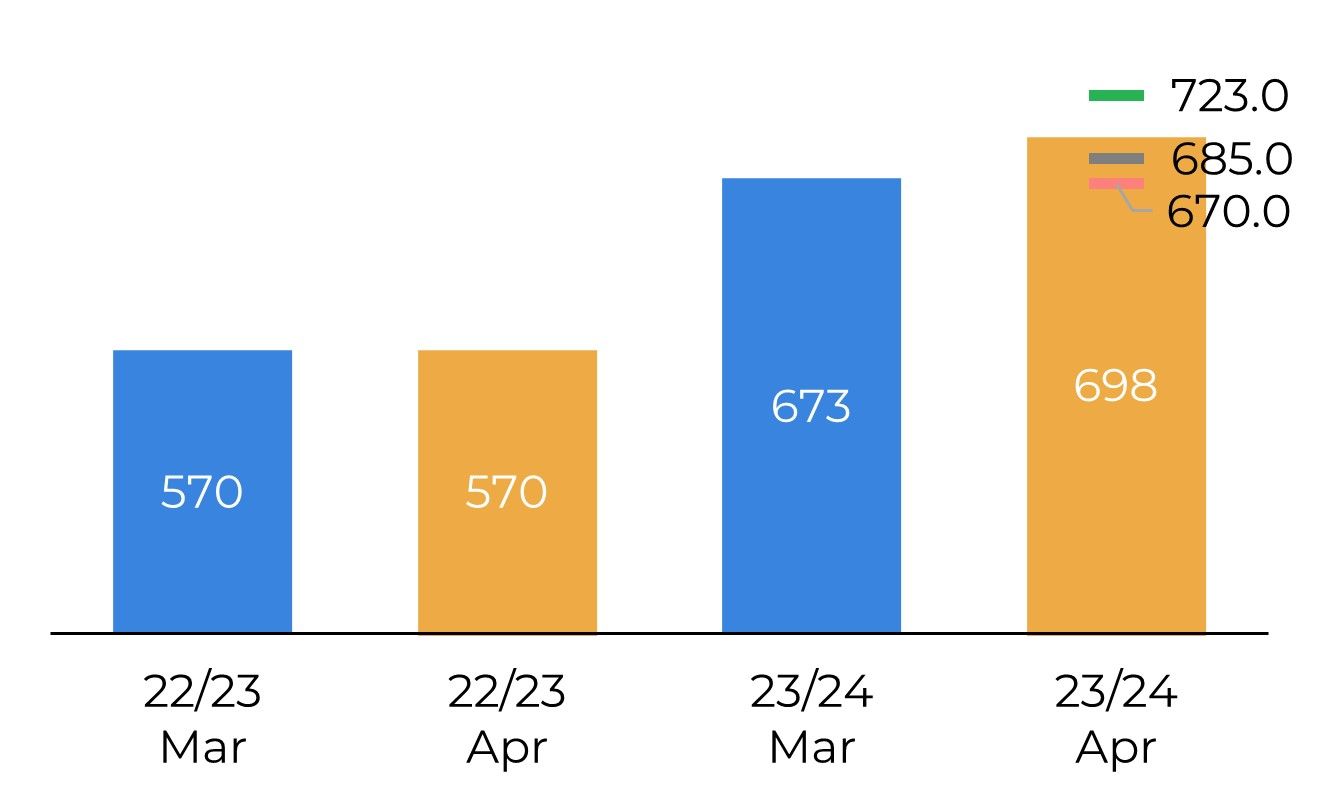

Bearish US ending stocks figures weighed on prices amid bullish global figures. On the US balance sheet, domestic consumption was reduced due to lower-than-expected implied feed and waste use in the second and third quarters, based on the latest NASS Grain Stocks report. Consequently, ending stocks were increased by 25M bu, more than the median estimate.

However, the world figures brought some bullish points to consider. Although the market was expecting higher world ending stocks, the USDA presented a cut of 0.5M mt, due to increased exports from Ukraine and domestic consumption in India.

Food, seed and industrial use in India rose by 2M mt this month to 106.2M mt. The latest monthly stock reports issued by the Food Corporation of India show continued sales on the open market, as the government of India tries to limit food price inflation ahead of the elections, which start at the end of this month.

Ukraine's exports increased by 1.5M mt to 17.5M mt, as competitive prices and longer opening hours at Odessa's ports this year allowed for an increase in export activity.