In wheat, the poor weather scenario for the southern hemisphere crops will likely keep dragging down world ending stocks – and probably more than market is currently expecting.

When it comes to Argentina, there’s already a gap of 3M mt between USDA current estimates and the most pessimistic local forecast – the Rosario Exchange just lowered its estimate to 13.5M mt.

For Australia, USDA’s numbers already contemplate a huge drop in yields compared to last season. Nonetheless, Australia recorded the driest October in more than 20 years due to the El Niño. Considering some of the lowest yields in this period, there’s still space for additional cuts to the Aussie output – which could come under 20M mt.

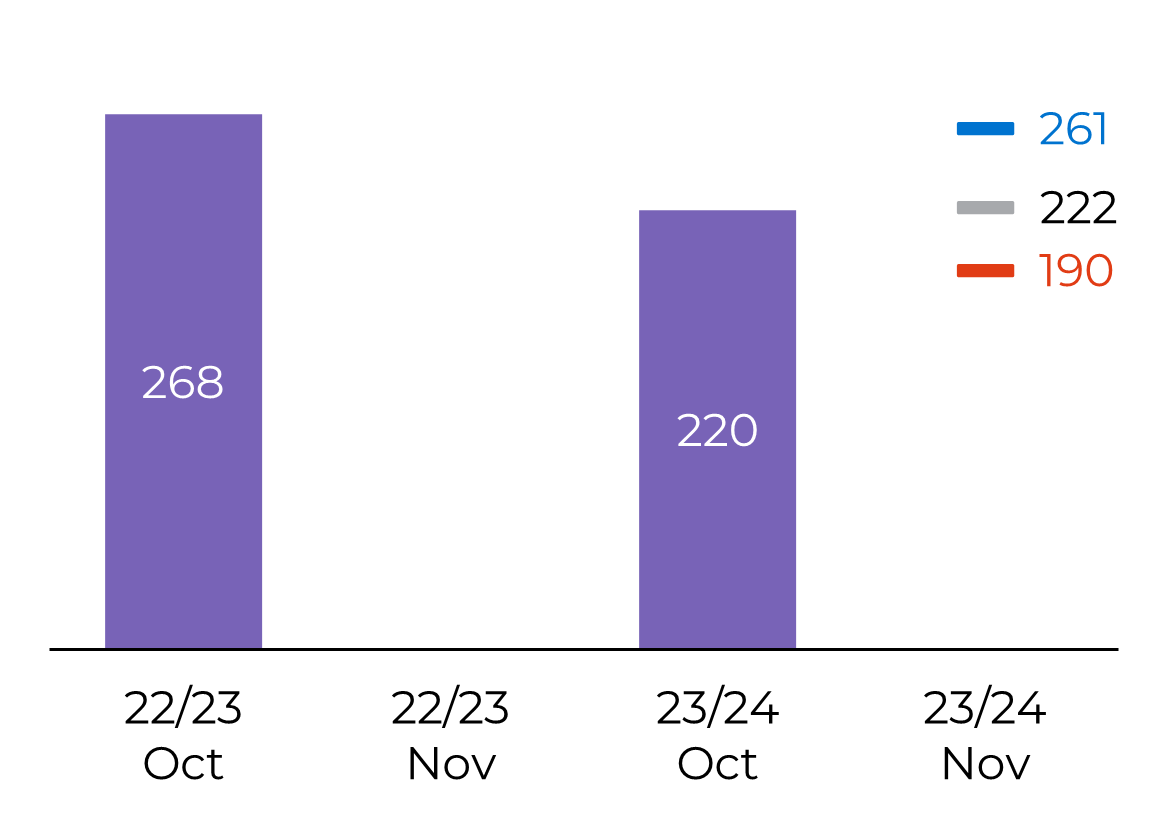

The market is not expecting much change in the US’ balance, but exporting activity is still very slow, opening space for a cut.