A new record for March delivery

"The volatility observed last week was primarily due to the anticipation of the March contract expiry. After the record high delivery, Brazilian availability is seen as tighter, and production issues in India and Thailand are providing short-term support for sugar prices. This situation could potentially lead to a rebound in the May contract if demand does not wait."

A new record for March delivery

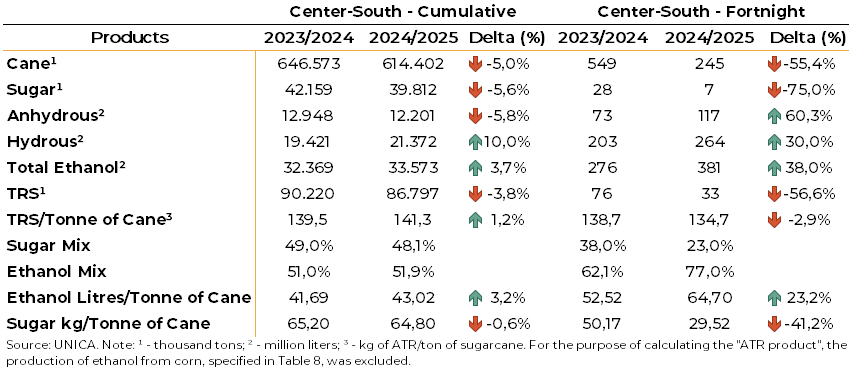

- UNICA's report showed figures in line with expectations, resulting in no price movement, with the Brazilian Center-South crushing only 245k mt of cane.

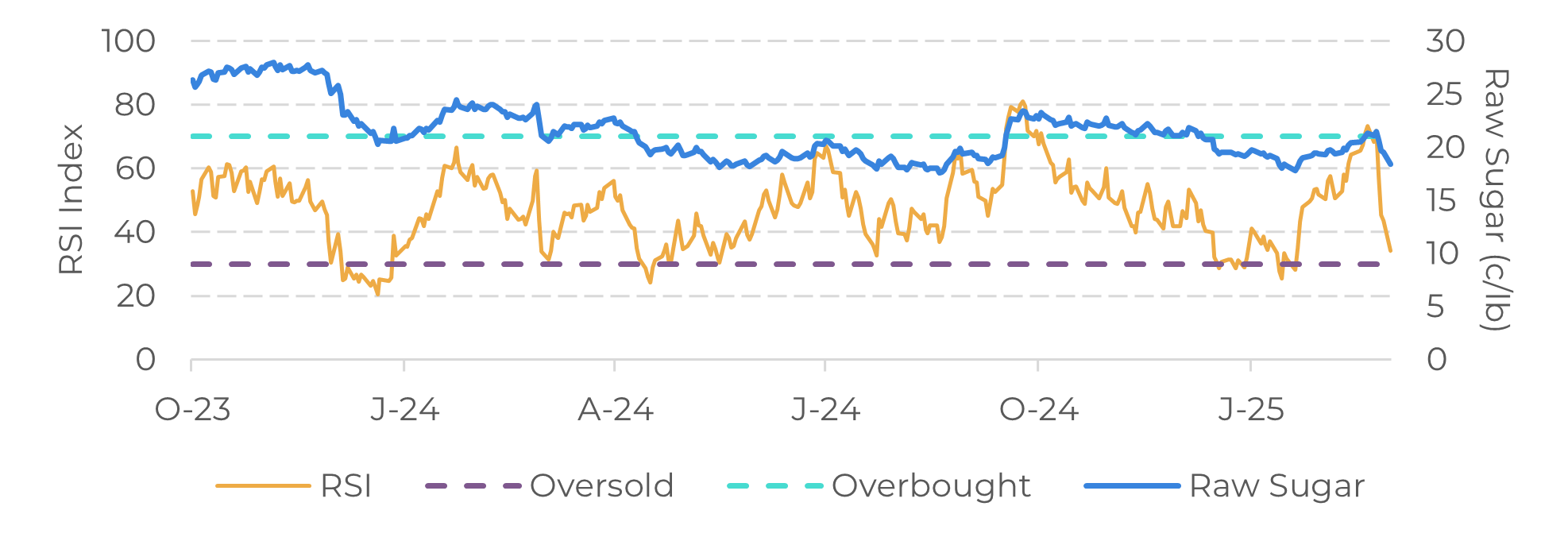

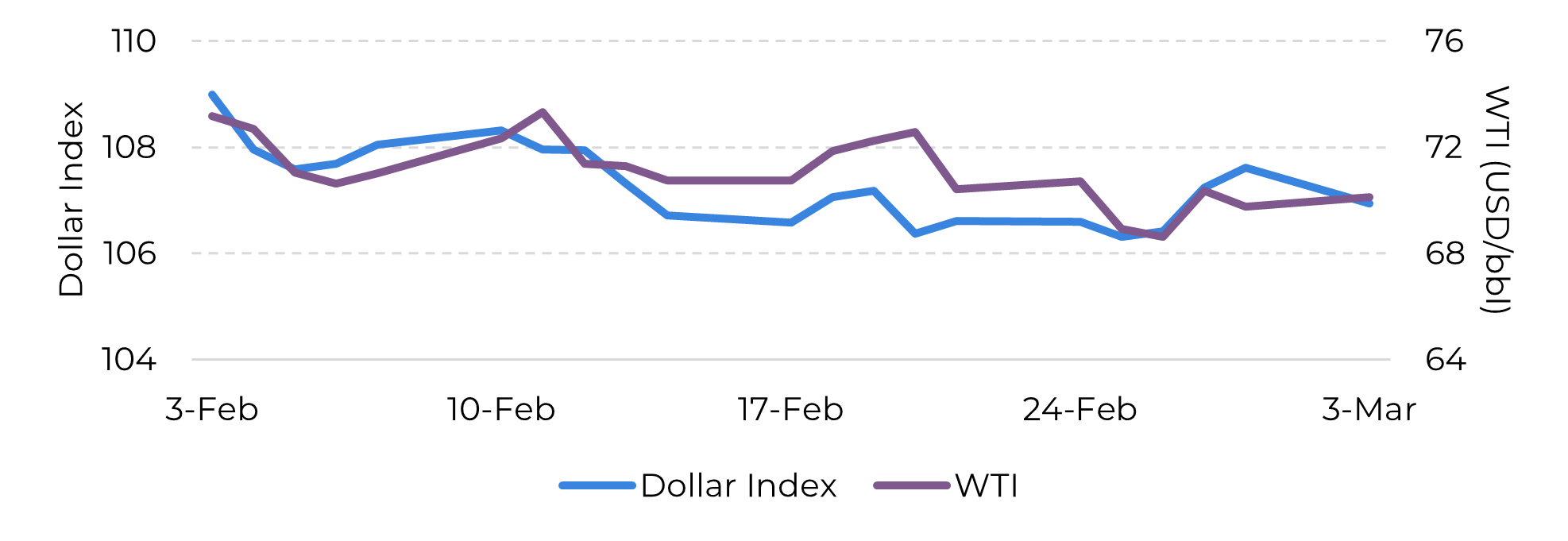

- The volatility observed last week was due to the anticipation of the March contract expiration, with Monday data showing signs of an overbought position. Coupled with a lower energy complex and a stronger dollar, sugar prices reduced 3.8% by Wednesday.

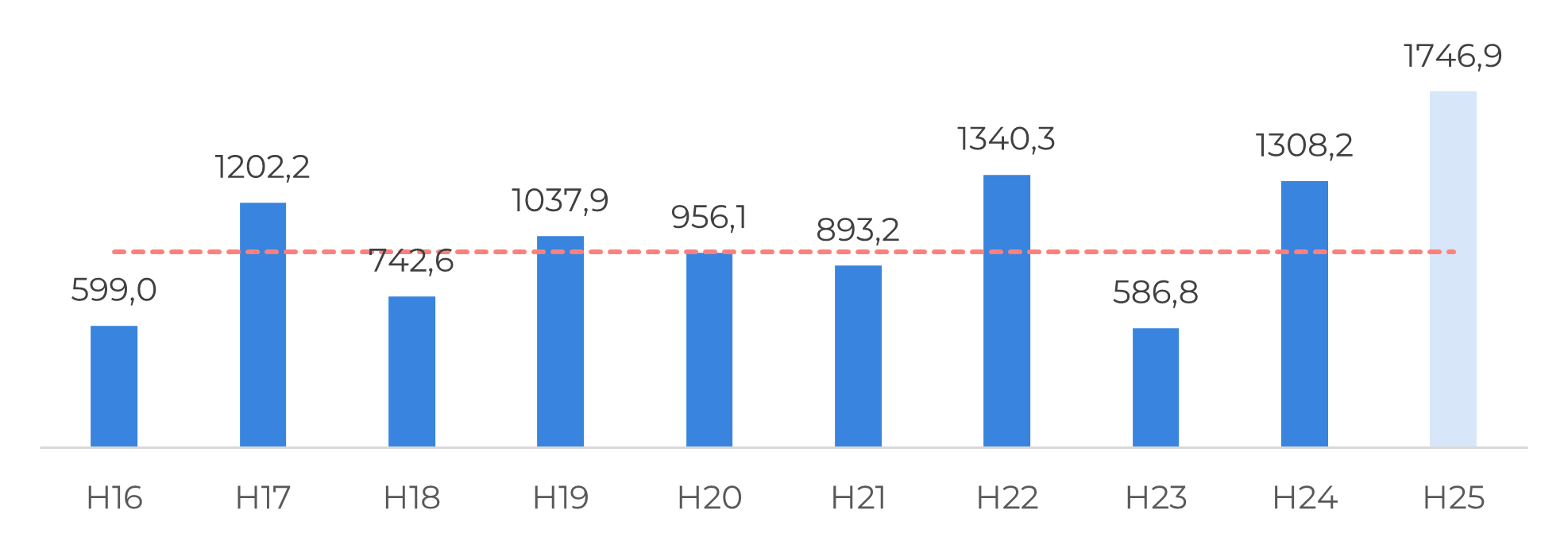

- The trend continued with a 4.6% reduction on Thursday due to active selling by Brazilian producers, and the March delivery exceeded expectations with 34,385 lots totaling 1.7Mt of sugar delivered at 19.51c/lb, setting a new record.

- Brazilian availability is seen as tighter after the delivery, and production issues in India and Thailand provide short-term support for sugar prices.

- As the market waits for the next Center-South crop, prices could still find support, with a potential rebound in the May contract depending on demand.

Last week, UNICA's report presented figures that aligned with both our and market expectations, resulting in no price movement. The Brazilian Center-South crushed only 245k mt of cane, producing a minimal output of 7k mt of sugar and 381 million liters of ethanol, all significantly lower than in 23/24 and consistent with off-season levels. Additionally, as anticipated, UNICA's director, Luciano Rodrigues, emphasized that the higher ethanol production during 24/25 from both cane and corn ensures no risks to domestic availability. This supports the outlook for another max-sugar crop in 25/26 and a bearish medium-term price trend.

Image 1: Center-South Crop Summary

Source: Unica, Hedgepoint

Image 2: Raw Sugar Relative Strength Index Analysis

Source: Refinitiv, Hedgepoint

Image 3: The Dolar Index and the Energy Complex

Source: Refinitiv, Hedgepoint

Image 4: Raw Sugar Delivery (Preliminary Data – ‘000t)

Source: Green Pool, Hedgepoint

In Summary

Weekly Report — Sugar

livea.coda@hedgepointglobal.com

laleska.moda@hedgepointglobal.com

Disclaimer

This document has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without intending to create obligations or commitments to third parties. It is not intended to promote or solicit an offer for the sale or purchase of any securities, commodities interests, or investment products. Hedgepoint and its associates expressly disclaim any liability for the use of the information contained herein that directly or indirectly results in any kind of damages. Information is obtained from sources which we believe to be reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. The trading of commodities interests, such as futures, options, and swaps, involves substantial risk of loss and may not be suitable for all investors. You should carefully consider wither such trading is suitable for you in light of your financial condition. Past performance is not necessarily indicative of future results. Customers should rely on their own independent judgment and/or consult advisors before entering into any transactions. Hedgepoint does not provide legal, tax or accounting advice and you are responsible for seeking any such advice separately. Hedgepoint Schweiz AG is organized, incorporated, and existing under the laws of Switzerland, is filiated to ARIF, the Association Romande des Intermédiaires Financiers, which is a FINMA-authorized Self-Regulatory Organization. Hedgepoint Commodities LLC is organized, incorporated, and existing under the laws of the USA, and is authorized and regulated by the Commodity Futures Trading Commission (CFTC) and a member of the National Futures Association (NFA) to act as an Introducing Broker and Commodity Trading Advisor. HedgePoint Global Markets Limited is Regulated by the Dubai Financial Services Authority. The content is directed at Professional Clients and not Retail Clients. Hedgepoint Global Markets PTE. Ltd is organized, incorporated, and existing under the laws of Singapore, exempted from obtaining a financial services license as per the Second Schedule of the Securities and Futures (Licensing and Conduct of Business) Act, by the Monetary Authority of Singapore (MAS). Hedgepoint Global Markets DTVM Ltda. is authorized and regulated in Brazil by the Central Bank of Brazil (BCB) and the Brazilian Securities Commission (CVM). Hedgepoint Serviços Ltda. is organized, incorporated, and existing under the laws of Brazil. Hedgepoint Global Markets S.A. is organized, incorporated, and existing under the laws of Uruguay. In case of questions not resolved by the first instance of customer contact (client.services@Hedgepointglobal.com), please contact internal ombudsman channel (ombudsman@hedgepointglobal.com – global or ouvidoria@hedgepointglobal.com – Brazil only) or call 0800-8788408 (Brazil only). Integrity, ethics, and transparency are values that guide our culture. To further strengthen our practices, Hedgepoint has a whistleblower channel for employees and third-parties by e-mail ethicline@hedgepointglobal.com or forms Ethic Line – Hedgepoint Global Markets. “HedgePoint” and the “HedgePoint” logo are marks for the exclusive use of HedgePoint and/or its affiliates. Use or reproduction is prohibited, unless expressly authorized by HedgePoint. Furthermore, the use of any other marks in this document has been authorized for identification purposes only. It does not, therefore, imply any rights of HedgePoint in these marks or imply endorsement, association or seal by the owners of these marks with HedgePoint or its affiliates.