Sweet rebound, sour risks

"Sugar prices rebounded on technical and demand signals, easing concerns over ethanol diversion in Brazil and possibly reducing Chinese buying interest. Despite this, fundamentals remain rather bearish, and macro risks, like new U.S. tariffs and BRL devaluation, could pressure the market. Northern Hemispheres good prospects, particularly India’s developments adds further pressure to long-term contracts."

Sweet rebound, sour risks

- Sugar prices rebounded, supported by demand signals and technical indicators.

- Fundamentals remain bearish, with stock-to-use ratios starting to rebuild, limiting the short-term possible upside beyond 17–18 c/lb.

- The U.S. tariff announcements boosted the dollar, driven by heightened inflation expectations. Combined with strong labor market data, this has shaken monetary easing expectations. However, uncertainty still pressure inflation value, which remains bellow previous years’.

- Ethanol diversion fears in Brazil eased as prices rose above 16 c/lb, especially in São Paulo; marginal shifts may occur in Goiás and Mato Grosso.

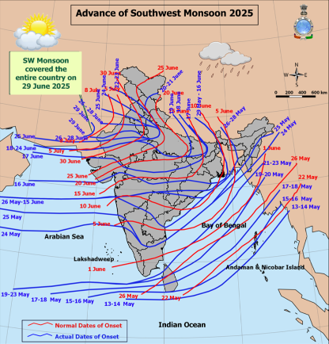

- Chinese buying could slow down amid higher prices, while India’s strong monsoon and planting suggest production recovery and possible export pressure next season.

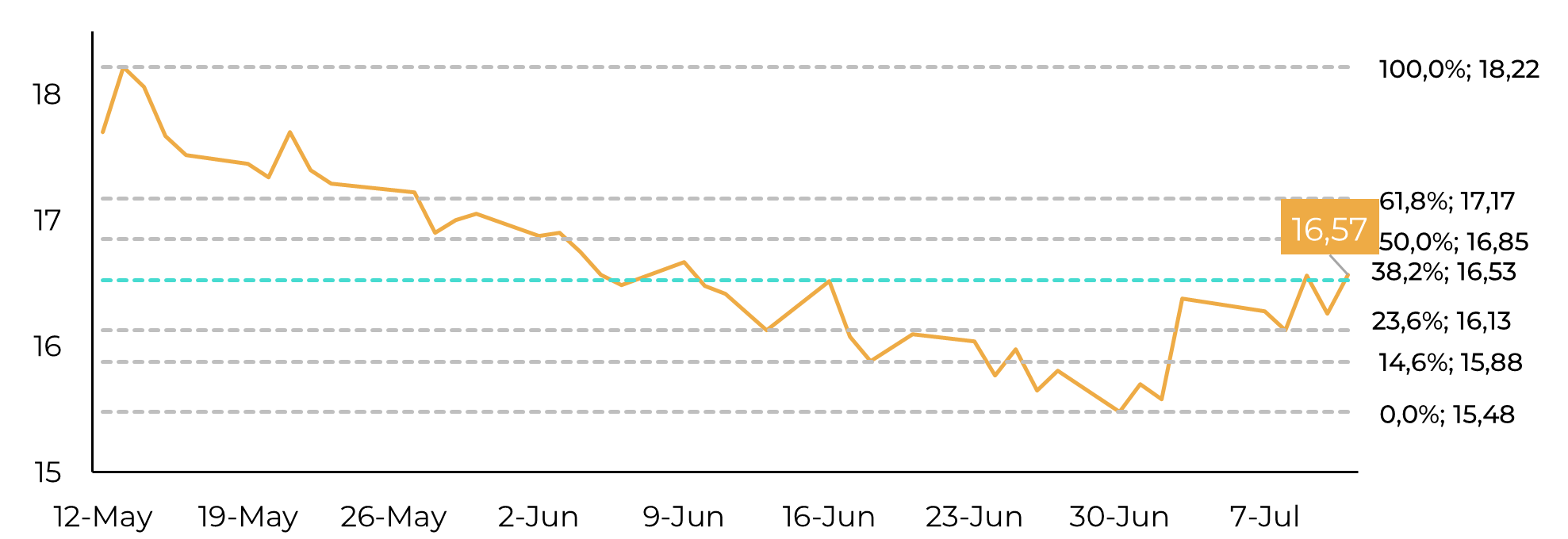

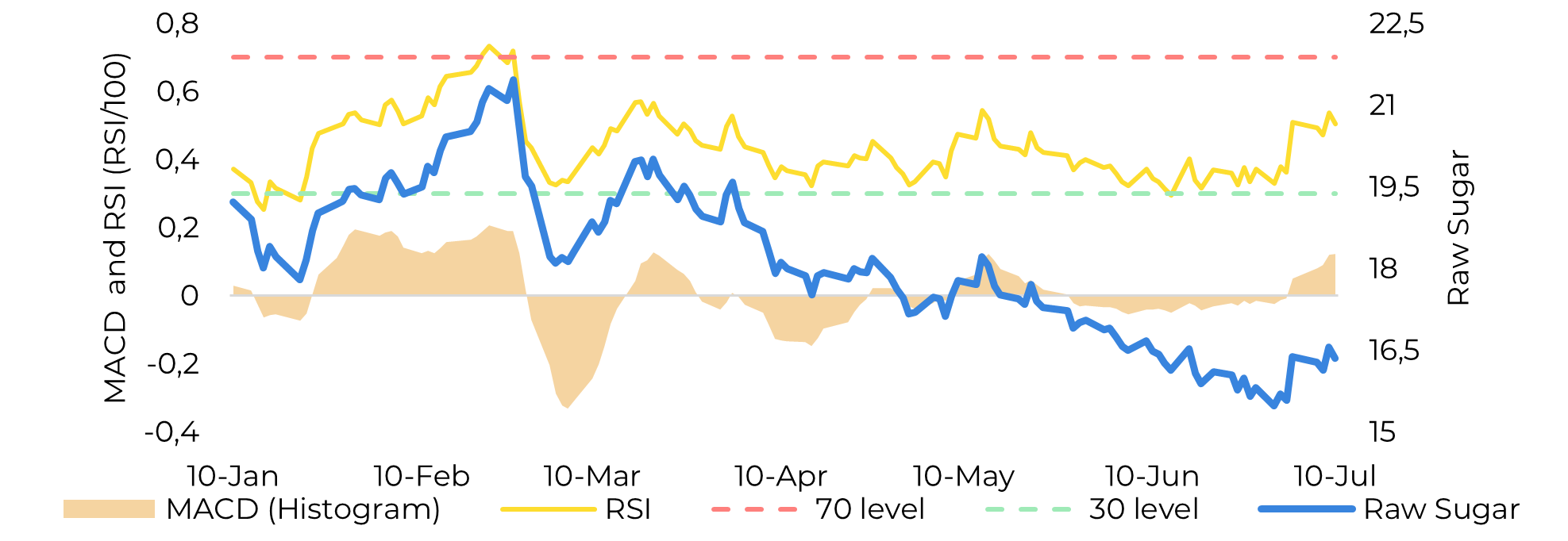

Sugar prices staged a recovery during the week, supported by demand-related news (Pakistan and Philippines), the latest Unica report, and broader fundamentals suggesting the dip to 15.5 c/lb may have been an overreaction. Technical indicators such as RSI and MACD have shifted, pointing to a more bullish trend. Notably, raw sugar prices climbed back above the 38.2% Fibonacci retracement level for the first time since June, potentially signaling renewed buying interest. However, fundamentals remain weaker than in the past three to four seasons, with stock-to-use ratios beginning to rebuild. While we agree that prices should be trading at higher levels (at least 17-18c/lb), there are clear limits, making a return to 2023–2024 highs unlikely.

Image 1: Fibonacci Retracement Levels (c/lb)

Source: LSEG, Hedgepoint

Image 2: MACD and RSI levels

Source: LSEG, Hedgepoint

Image 3: New Tariffs to take place on August 1st

Source: LSEG, Hedgepoint

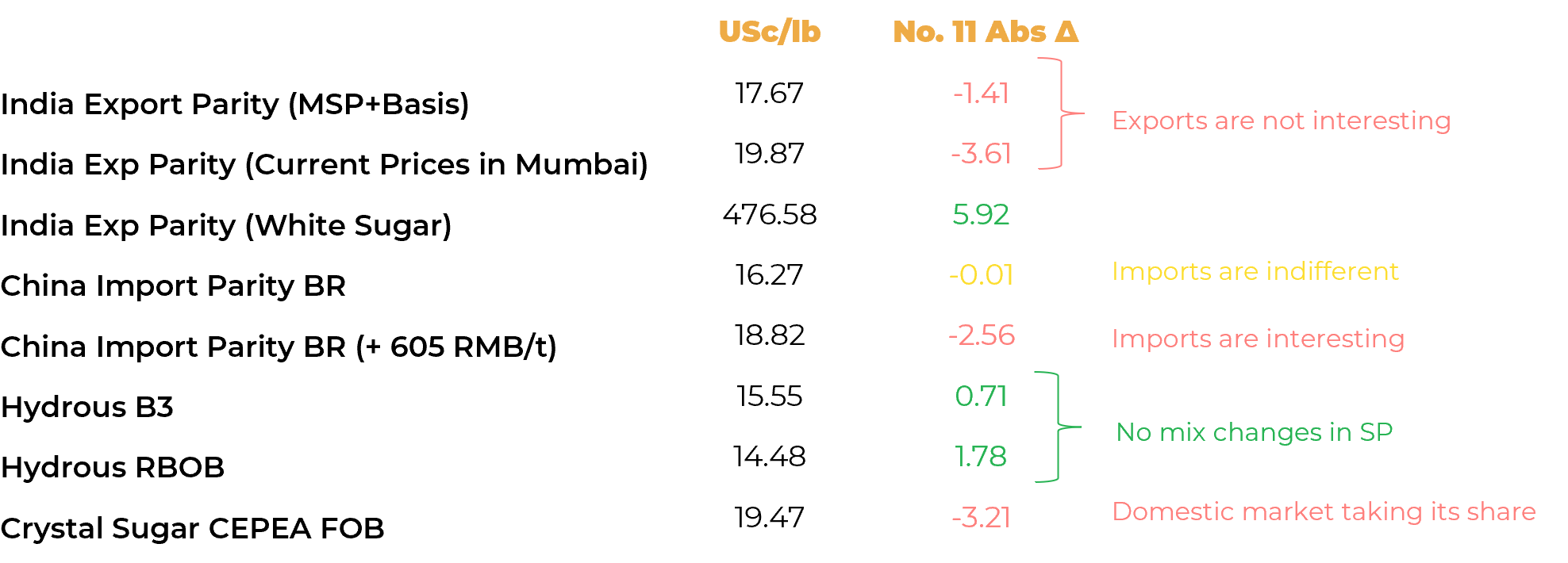

Image 4: Key Indicators (compared to Thursday close 16.26 c/lb)

Source: Bloomberg, LSEG, Hedgepoint

Image 5: Advance of Southwest Monsoon (2025)

Source: Indian Meteorological Department

In Summary

Weekly Report — Sugar

livea.coda@hedgepointglobal.com

laleska.moda@hedgepointglobal.com

Disclaimer

This document has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without intending to create obligations or commitments to third parties. It is not intended to promote or solicit an offer for the sale or purchase of any securities, commodities interests, or investment products. Hedgepoint and its associates expressly disclaim any liability for the use of the information contained herein that directly or indirectly results in any kind of damages. Information is obtained from sources which we believe to be reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. The trading of commodities interests, such as futures, options, and swaps, involves substantial risk of loss and may not be suitable for all investors. You should carefully consider wither such trading is suitable for you in light of your financial condition. Past performance is not necessarily indicative of future results. Customers should rely on their own independent judgment and/or consult advisors before entering into any transactions. Hedgepoint does not provide legal, tax or accounting advice and you are responsible for seeking any such advice separately. Hedgepoint Schweiz AG is organized, incorporated, and existing under the laws of Switzerland, is filiated to ARIF, the Association Romande des Intermédiaires Financiers, which is a FINMA-authorized Self-Regulatory Organization. Hedgepoint Commodities LLC is organized, incorporated, and existing under the laws of the USA, and is authorized and regulated by the Commodity Futures Trading Commission (CFTC) and a member of the National Futures Association (NFA) to act as an Introducing Broker and Commodity Trading Advisor. HedgePoint Global Markets Limited is Regulated by the Dubai Financial Services Authority. The content is directed at Professional Clients and not Retail Clients. Hedgepoint Global Markets PTE. Ltd is organized, incorporated, and existing under the laws of Singapore, exempted from obtaining a financial services license as per the Second Schedule of the Securities and Futures (Licensing and Conduct of Business) Act, by the Monetary Authority of Singapore (MAS). Hedgepoint Global Markets DTVM Ltda. is authorized and regulated in Brazil by the Central Bank of Brazil (BCB) and the Brazilian Securities Commission (CVM). Hedgepoint Serviços Ltda. is organized, incorporated, and existing under the laws of Brazil. Hedgepoint Global Markets S.A. is organized, incorporated, and existing under the laws of Uruguay. In case of questions not resolved by the first instance of customer contact (client.services@Hedgepointglobal.com), please contact internal ombudsman channel (ombudsman@hedgepointglobal.com – global or ouvidoria@hedgepointglobal.com – Brazil only) or call 0800-8788408 (Brazil only). Integrity, ethics, and transparency are values that guide our culture. To further strengthen our practices, Hedgepoint has a whistleblower channel for employees and third-parties by e-mail ethicline@hedgepointglobal.com or forms Ethic Line – Hedgepoint Global Markets. “HedgePoint” and the “HedgePoint” logo are marks for the exclusive use of HedgePoint and/or its affiliates. Use or reproduction is prohibited, unless expressly authorized by HedgePoint. Furthermore, the use of any other marks in this document has been authorized for identification purposes only. It does not, therefore, imply any rights of HedgePoint in these marks or imply endorsement, association or seal by the owners of these marks with HedgePoint or its affiliates.

To access this report, you need to be a subscriber.

Contact us

Check our general terms and important notices.

We have updated our Terms & Conditions to reflect improvements to our platform, data handling practices, and the overall experience we provide to our clients.