A tour around the Northern Hemisphere’s preliminary estimates

"Despite the movement in the market this week, it is also important to keep in mind the recent changes in expectations regarding the Northern Hemisphere. Tracking how these figures evolve could prove insightful, especially considering the Q4/25 and Q1/26. Our analysis will cover Europe, India, the US, China, and Thailand."

A tour around the Northern Hemisphere’s preliminary estimates

- Sugar prices fell at the beginning of the week due to weak demand and Indian crop expectations. However, the raw contracts recovered 2% on July 24 amid physical market rumors.

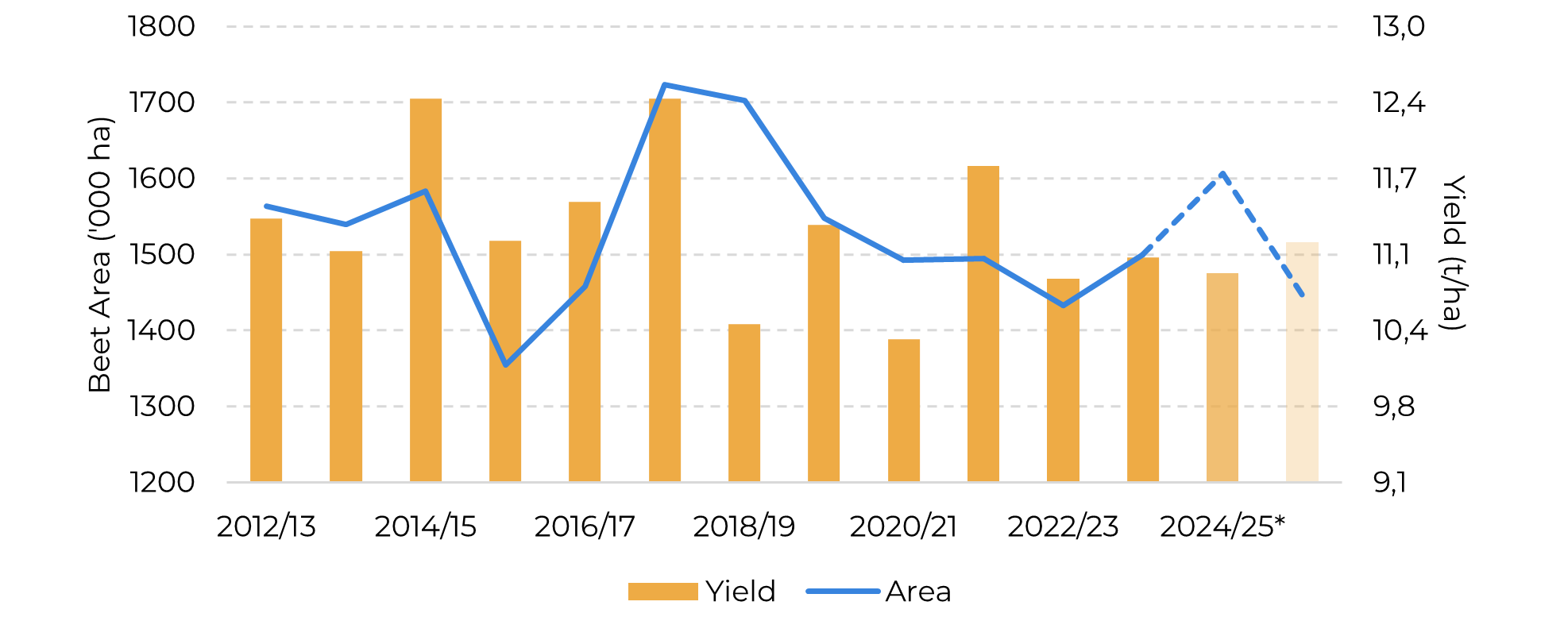

- Europe expects a 10% drop in beet area, with production falling by 1.4Mt in 2025/26, increasing import needs despite good crop development.

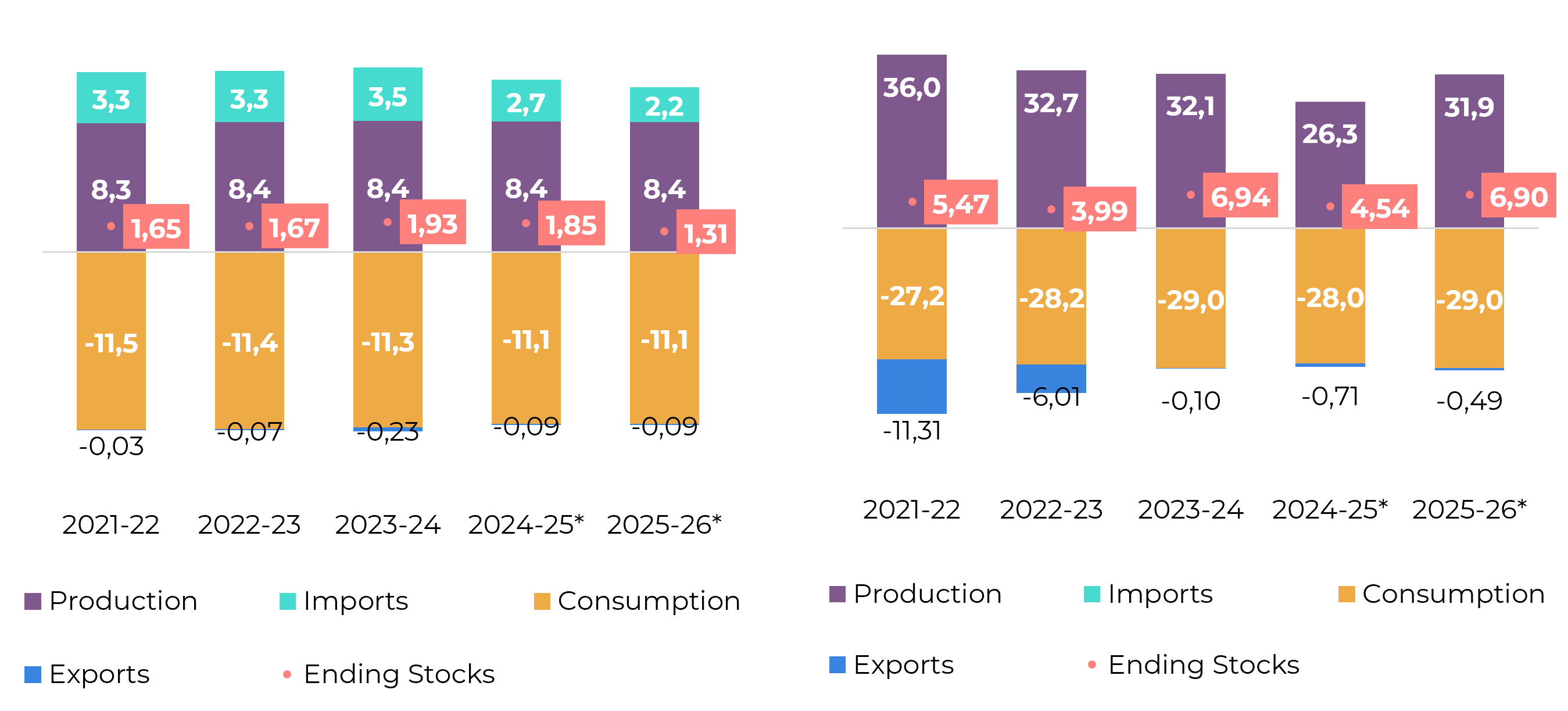

- U.S. sugar output may slightly decline, driven by lower beet yields, while Louisiana cane area continues to expand for the sixth year.

- India’s production is set to recover to ~32Mt, supported by strong monsoon and crop conditions; exports remain uncertain.

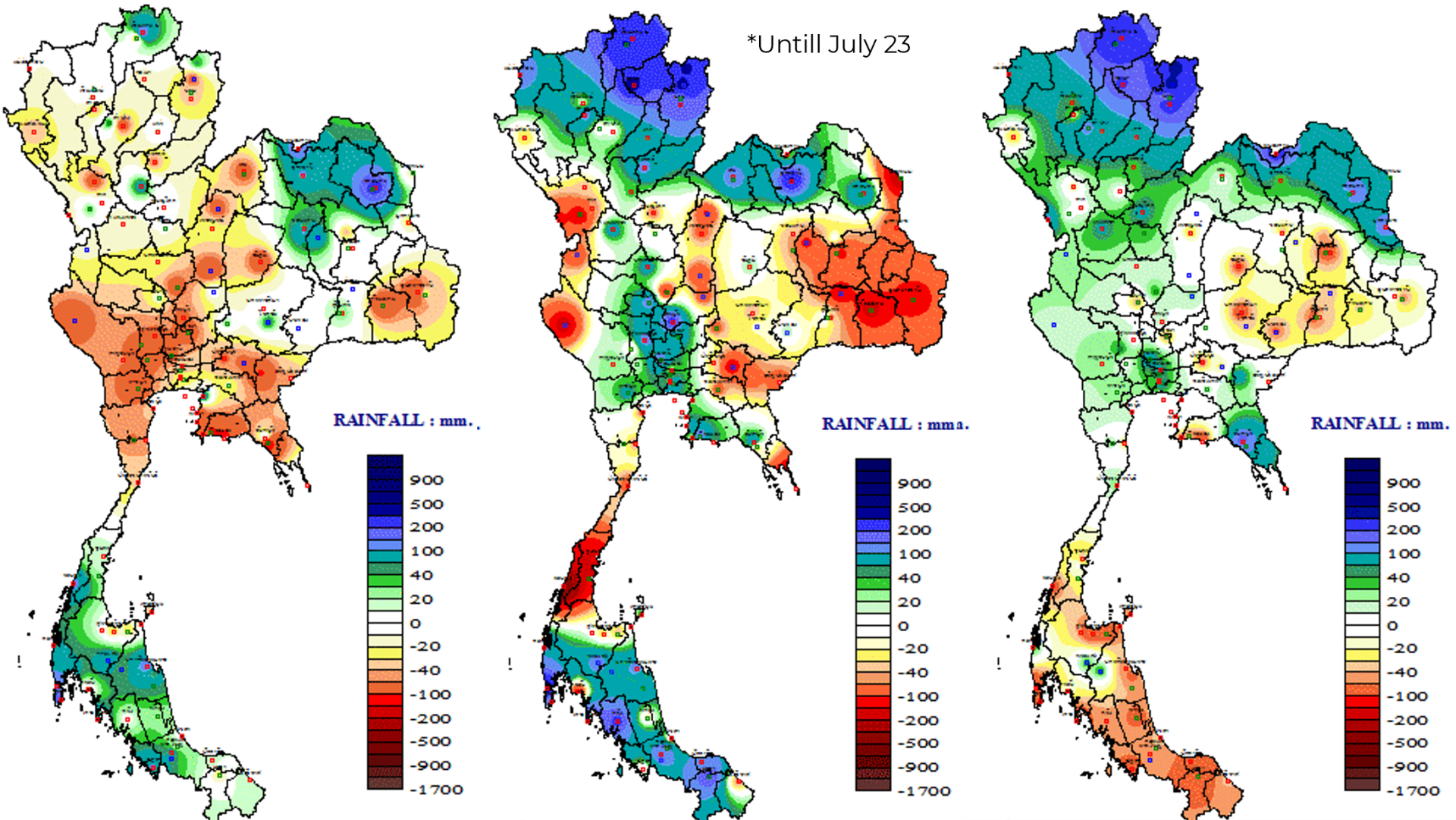

- Thailand’s output rebounds to 10.1Mt, with potential to reach 11.5Mt in 2025/26 and boost exports above 8Mt.

- China maintains strong production (~11.2Mt) and uses stock levels to time imports strategically, taking advantage of recent price dips.

SSugar prices failed to sustain the gains seen in the previous week and started Monday, July 21, on a bearish trend. The lack of significant movement in demand, coupled with expectations of a robust harvest in India in next season, put pressure on raw sugar prices, with the September contract closing Wednesday at 16.24 c/lb. However, part of these losses were reversed on Thursday (24), driven by rumors of increased demand in the physical market. As a result, the sweetener rose 2%, closing the day at 16.57 c/lb.

Despite the movement in the market this week, it is also important to keep in mind the recent changes in expectations regarding the Northern Hemisphere. Tracking how these figures evolve could prove insightful, especially considering the Q4/25 and Q1/26. Our analysis will cover Europe, India, the US, China, and Thailand.

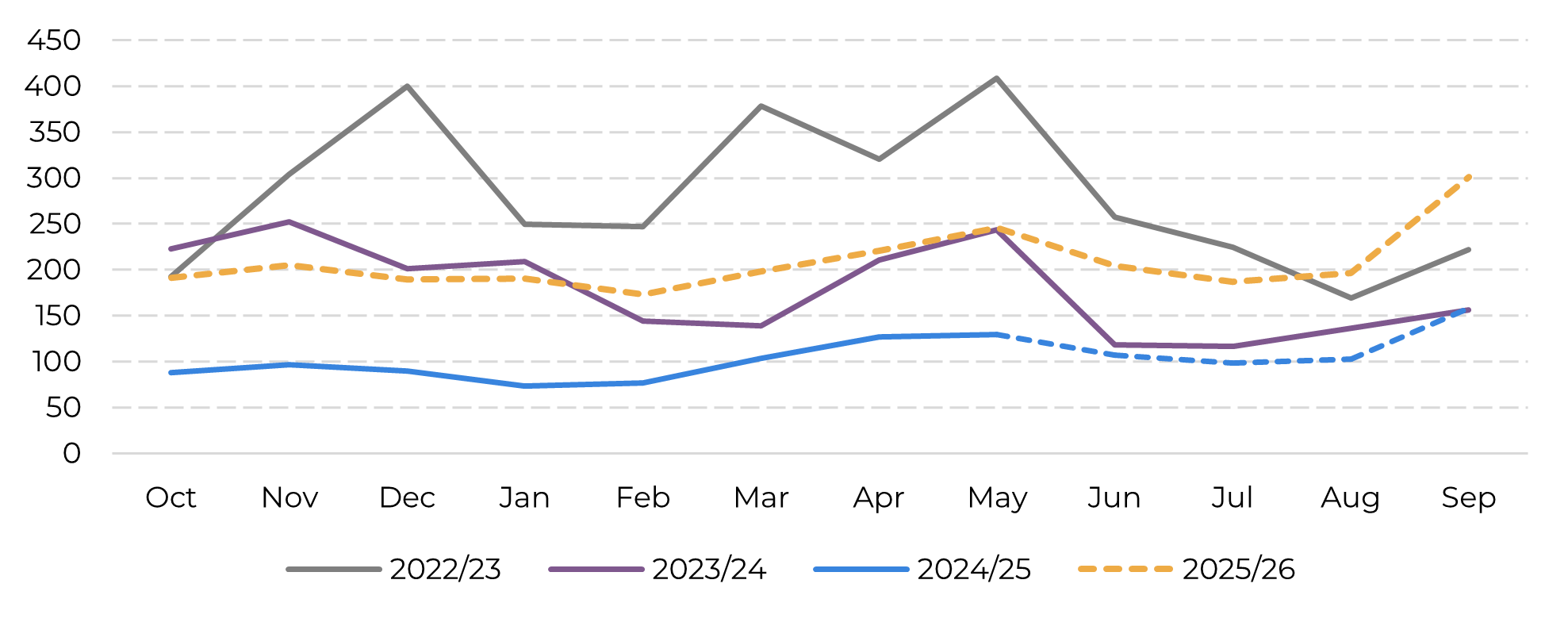

EU+UK Estimated Imports (Total Sugar – ‘000t)

Source: EC, Hedgepoint

EU 27+UK Area x Yield

Source: : EC, Green Pool, Hedgepoint

Despite some weather concerns during the spring, beet development has reportedly progressed well, with expectations of yield improvement. Nevertheless, overall production is still forecasted to decline year-over-year. Our outlook for the EU+UK points to an early drop of 1.4 million tons by 25/26, which will likely increase the region’s import needs.

US (left) and India (right) Sugar Balances – Oct Sep

Source: USDA, ISMA, AISTA, ChiniMandi, NFCSF, Hedgepoint

Thailand Precipitation Anomaly in mm (June – left; July* – center and August expectation - right)

Source: Thai Meteorological Department

Although there are some concerns about weather conditions in Thailand, particularly in the central region, production is expected to continue improving. From the 8.8Mt produced in 23/24, the current season has already added over 1Mt, reaching 10.1Mt. Looking ahead to 25/26, the recovery trend is likely to persist, especially given the favorable weather in the northern and eastern regions. We project that Thailand could reach close to 11.5Mt in production and increase its exports to over 8Mt.

In Summary

Weekly Report — Sugar

livea.coda@hedgepointglobal.com

laleska.moda@hedgepointglobal.com

Disclaimer

This document has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without intending to create obligations or commitments to third parties. It is not intended to promote or solicit an offer for the sale or purchase of any securities, commodities interests, or investment products. Hedgepoint and its associates expressly disclaim any liability for the use of the information contained herein that directly or indirectly results in any kind of damages. Information is obtained from sources which we believe to be reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. The trading of commodities interests, such as futures, options, and swaps, involves substantial risk of loss and may not be suitable for all investors. You should carefully consider wither such trading is suitable for you in light of your financial condition. Past performance is not necessarily indicative of future results. Customers should rely on their own independent judgment and/or consult advisors before entering into any transactions. Hedgepoint does not provide legal, tax or accounting advice and you are responsible for seeking any such advice separately. Hedgepoint Schweiz AG is organized, incorporated, and existing under the laws of Switzerland, is filiated to ARIF, the Association Romande des Intermédiaires Financiers, which is a FINMA-authorized Self-Regulatory Organization. Hedgepoint Commodities LLC is organized, incorporated, and existing under the laws of the USA, and is authorized and regulated by the Commodity Futures Trading Commission (CFTC) and a member of the National Futures Association (NFA) to act as an Introducing Broker and Commodity Trading Advisor. HedgePoint Global Markets Limited is Regulated by the Dubai Financial Services Authority. The content is directed at Professional Clients and not Retail Clients. Hedgepoint Global Markets PTE. Ltd is organized, incorporated, and existing under the laws of Singapore, exempted from obtaining a financial services license as per the Second Schedule of the Securities and Futures (Licensing and Conduct of Business) Act, by the Monetary Authority of Singapore (MAS). Hedgepoint Global Markets DTVM Ltda. is authorized and regulated in Brazil by the Central Bank of Brazil (BCB) and the Brazilian Securities Commission (CVM). Hedgepoint Serviços Ltda. is organized, incorporated, and existing under the laws of Brazil. Hedgepoint Global Markets S.A. is organized, incorporated, and existing under the laws of Uruguay. In case of questions not resolved by the first instance of customer contact (client.services@Hedgepointglobal.com), please contact internal ombudsman channel (ombudsman@hedgepointglobal.com – global or ouvidoria@hedgepointglobal.com – Brazil only) or call 0800-8788408 (Brazil only). Integrity, ethics, and transparency are values that guide our culture. To further strengthen our practices, Hedgepoint has a whistleblower channel for employees and third-parties by e-mail ethicline@hedgepointglobal.com or forms Ethic Line – Hedgepoint Global Markets. “HedgePoint” and the “HedgePoint” logo are marks for the exclusive use of HedgePoint and/or its affiliates. Use or reproduction is prohibited, unless expressly authorized by HedgePoint. Furthermore, the use of any other marks in this document has been authorized for identification purposes only. It does not, therefore, imply any rights of HedgePoint in these marks or imply endorsement, association or seal by the owners of these marks with HedgePoint or its affiliates.