Sugar Outlook Remains Bearish

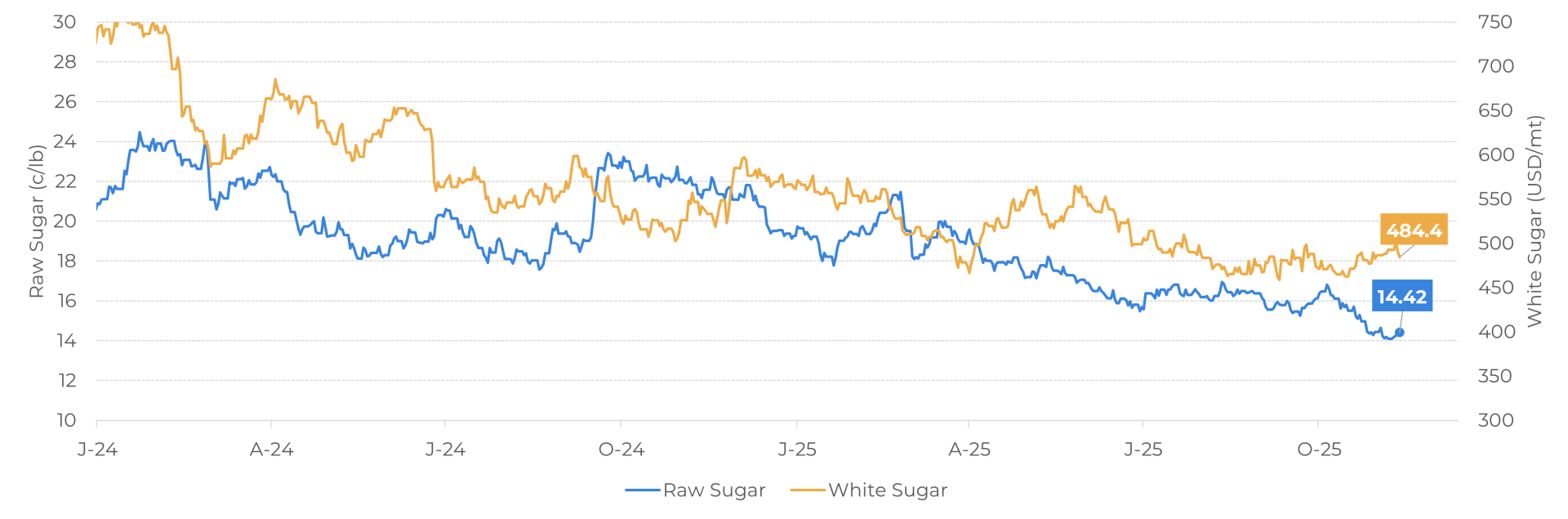

- Raw sugar prices have recently touched a 5-year low, at 14.04 c/lb. Although the contract has returned to the 14-15 c/lb levels this week – partially driven by the macro front – fundamentals remain bearish, with a surplus expected in 25/26.

- Part of the surplus expected is due to a good performance from Brazil’s Center South region in the second half of the crop. So far, cumulative sugar production for the current cycle has already exceeded that of the previous one.

- Beyond Brazil, the Northen Hemisphere is also set to have a good output in 25/26, due to better weather conditions, especially in India.

- Favorable weather in Thailand and good sugarcane development in India are driving optimistic supply expectations for the Northern Hemisphere. These projections are supported by robust production forecasts and ongoing weather monitoring in key growing regions.

- The authorization of sugar exports from India, combined with greater global availability, supports a robust supply scenario. This helps offset Brazil’s off-season and reinforces the consensus of a surplus for the 25/26 season, which tends to limit significant price increases.

Sugar Prices

Sugar prices have been in a bearish trend for the past months,

experiencing a sharp drop between October and November. In recent days, the

Mar26 raw contract reached its lowest level in five years at 14.04 c/lb, while

the Dec25 white contract touched 406 USD/Mt levels past

Monday (10), the lowest since Dec 2020.

Both contracts had a modest recovery since then, mainly focused on the macroeconomic scenario, as the US approached the end to its longest government shutdown. Early this week, the Senate was able to pass a new funding package, approved by the House of Representatives on Wednesday (12), ending the 43-day shutdown. The resuming government activity on Thursday (13) has also given some support to equities and some commodities, such as sugar.

Raw and white sugar prices (1st contract)

Source: LSEG

Brazil and India

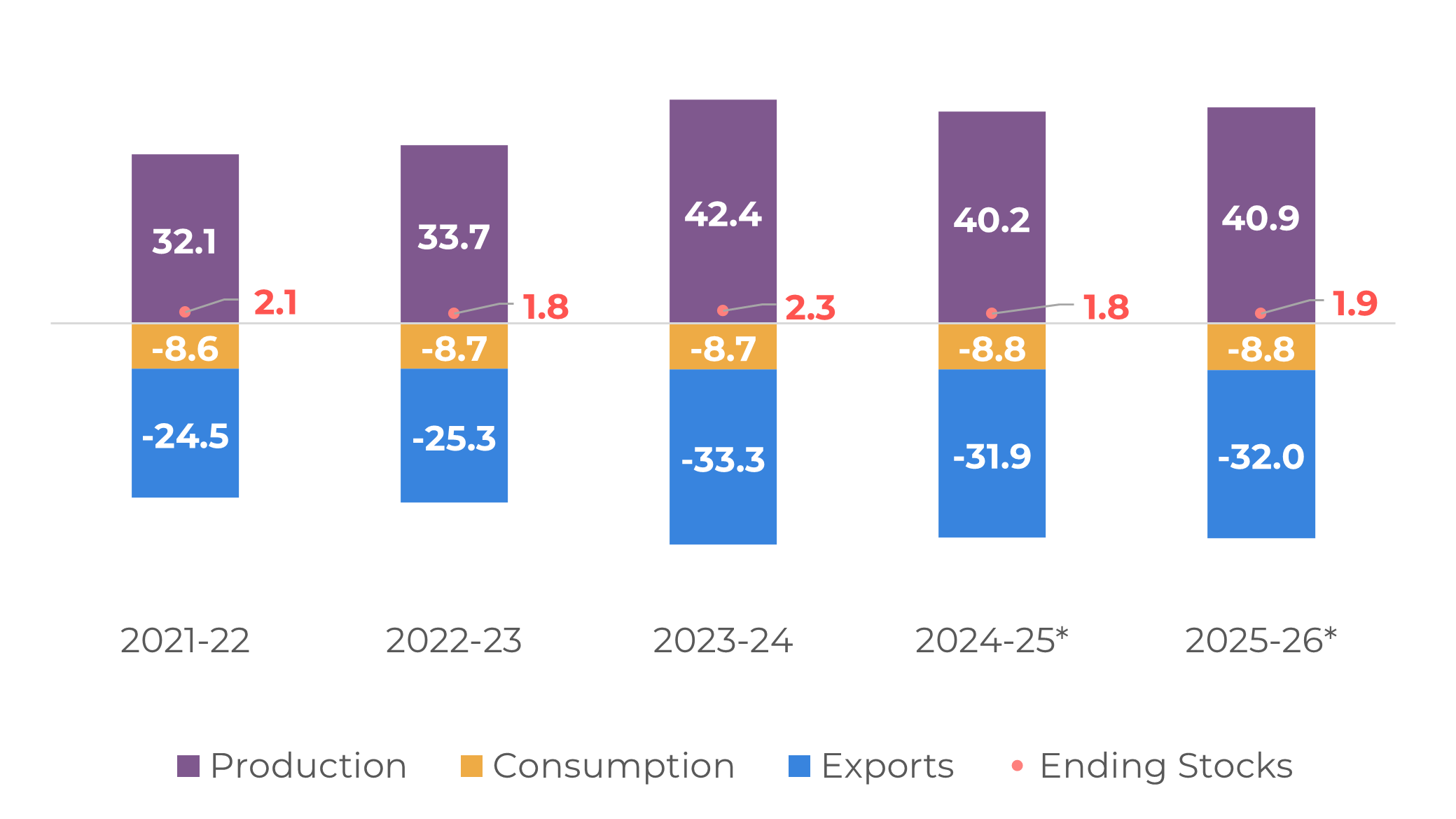

However, the macroeconomic support tends to be short-lived, as sugar supply and demand fundamentals remain bearish, with a surplus expected in 25/26. One of the main drivers for this is the better-than-expected Brazilian harvest after July. Although TRS (total recoverable sugar) remained below average levels, sugar crushing rebounded after July, which prompted us to maintain our expectations of a total crushing around 605 Mt of sugarcane, slightly lower than 24/25. As mix also continued in higher levels – with a record in the first half of August – cumulative sugar production for the 25/26 cycle surpassed 24/25 levels at the end of September and are likely to end the harvest above.

Even with current parity levels favoring ethanol production, the cumulative sugar mix is unlikely to change significantly this cycle, due to the higher levels in previous months and the recent drop in oil prices. There may be some deviation in Goiás, Mato Grosso, and Mato Grosso do Sul states, but this will not affect the overall sugar figures in 25/26, with our supply expectations around 40.9 Mt.

But Brazil will not be the only country contributing to global supply, as the Northern Hemisphere enters its harvest season. In the region, expectations remain positive for the main producers. In Thailand, favorable weather during crop development reinforces our sugar production estimate of around 10 Mt. Nonetheless, weather conditions continue to be closely monitored, particularly the intensity and possible impacts of the La Niña phenomenon, which could affect the pace of harvesting.

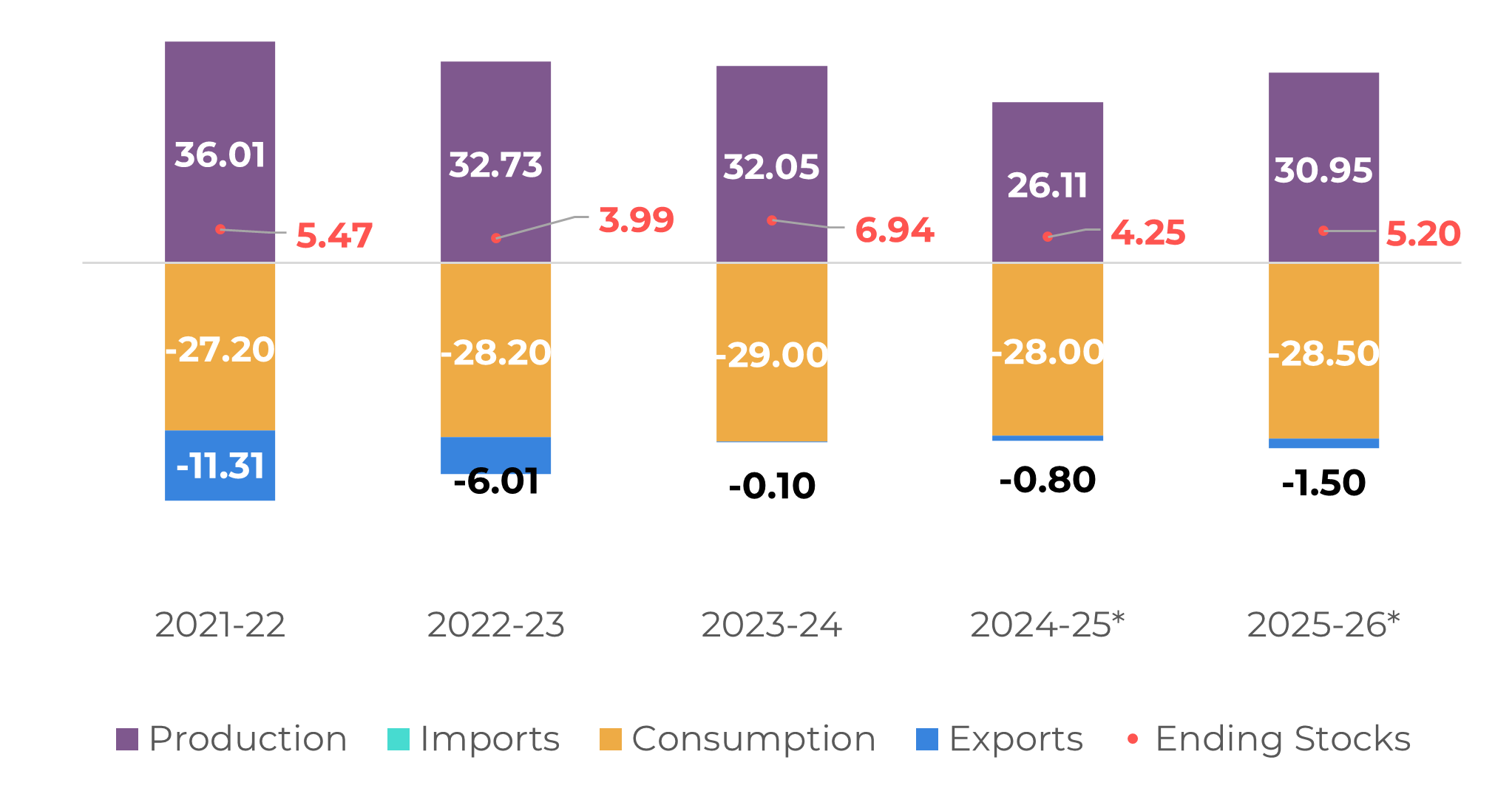

The outlook is also positive for India. According to recent ISMA estimates, the country is expected to produce 30.95 Mt of sugar, considering a diversion of 3.4 Mt for ethanol. While the planted area increased only marginally by 0.4%, the favorable production forecast is largely attributed to strong sugarcane development across key growing regions. Adequate rainfall and healthy reservoir levels have contributed to this expectation, along with other contributing factors such as a higher volume of plant cane in Maharashtra, a slight increase in the area cultivated in Karnataka, and the replacement of varieties in Uttar Pradesh.

As for exports, the Indian government has authorized 1.5 Mt for the 225/26 cycle, in line with our expectations. Any revision to this volume could result from a change in the export regime, influenced by current international sugar prices and parity. However, domestic prices remain a factor to be considered and could influence potential adjustments.

Brazil Supply and Demand (Mt)

Source: Hedgepoint

India Supply and Demand (Mt)

Source: Hedgepoint

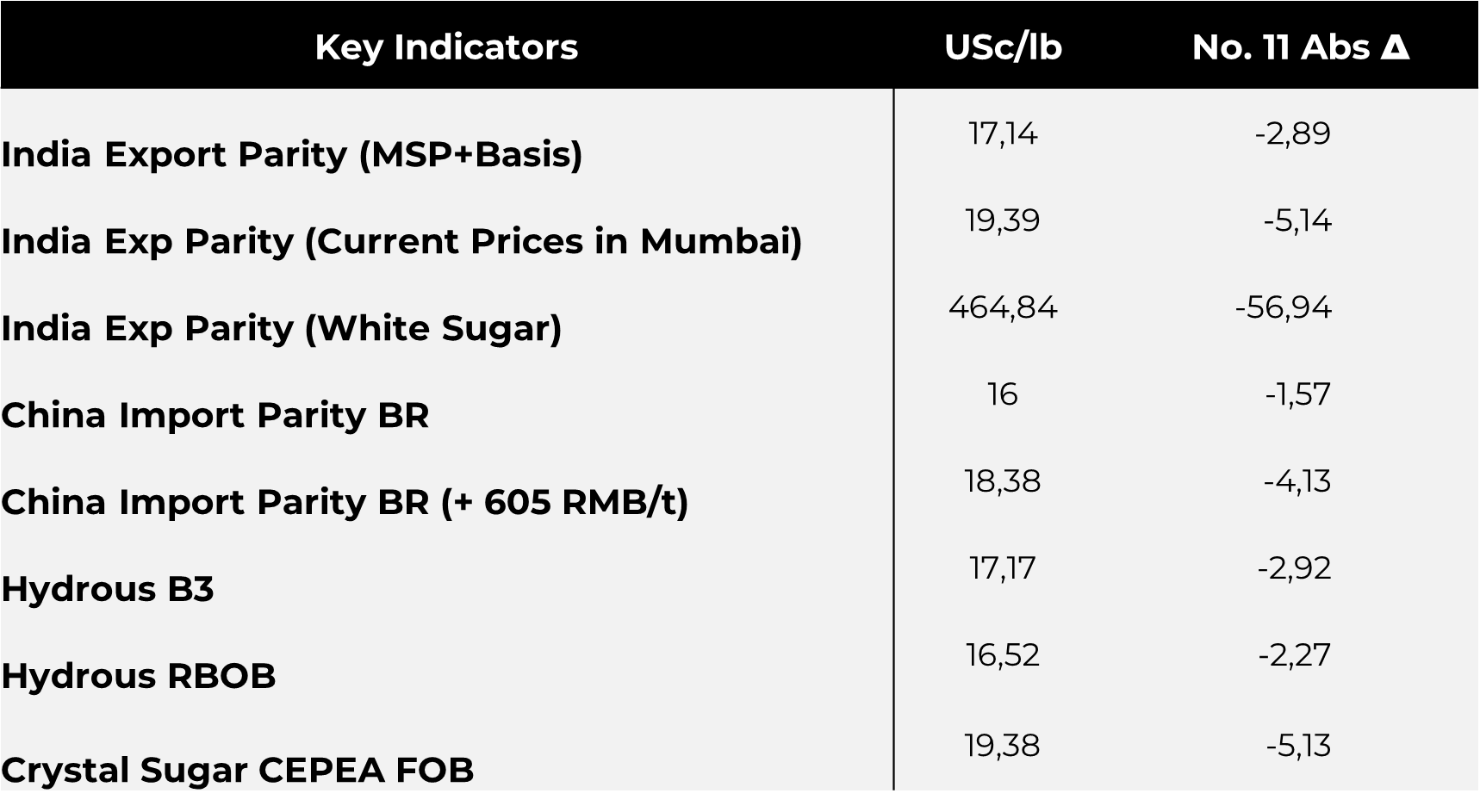

Source: Green Pool, Hedgepoint

Source: LSEG, Bloomberg, Hedgepoint

Summary

Sugar prices have been under pressure in recent months, with notable

declines between October and November. Despite temporary macroeconomic support,

sugar market fundamentals continue to signal a bearish outlook, primarily due

to expectations of a surplus in the 25/26 cycle.

Brazil's harvest has exceeded expectations since July, with sugarcane

crushing rebounding and cumulative sugar production surpassing the previous

cycle. Even though ethanol production is currently more favorable due to parity

levels, the sugar mix is unlikely to shift significantly, with likely a higher

sugar production in 25/26.

Weekly Report — Sugar

laleska.moda@hedgepointglobal.com

Reviewed by Thais Italiani

thais.italiani@hedgepointglobal.com

Disclaimer

This document has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without intending to create obligations or commitments to third parties. It is not intended to promote or solicit an offer for the sale or purchase of any securities, commodities interests, or investment products.