Risk-off sentiment and ample supply keep sugar under pressure

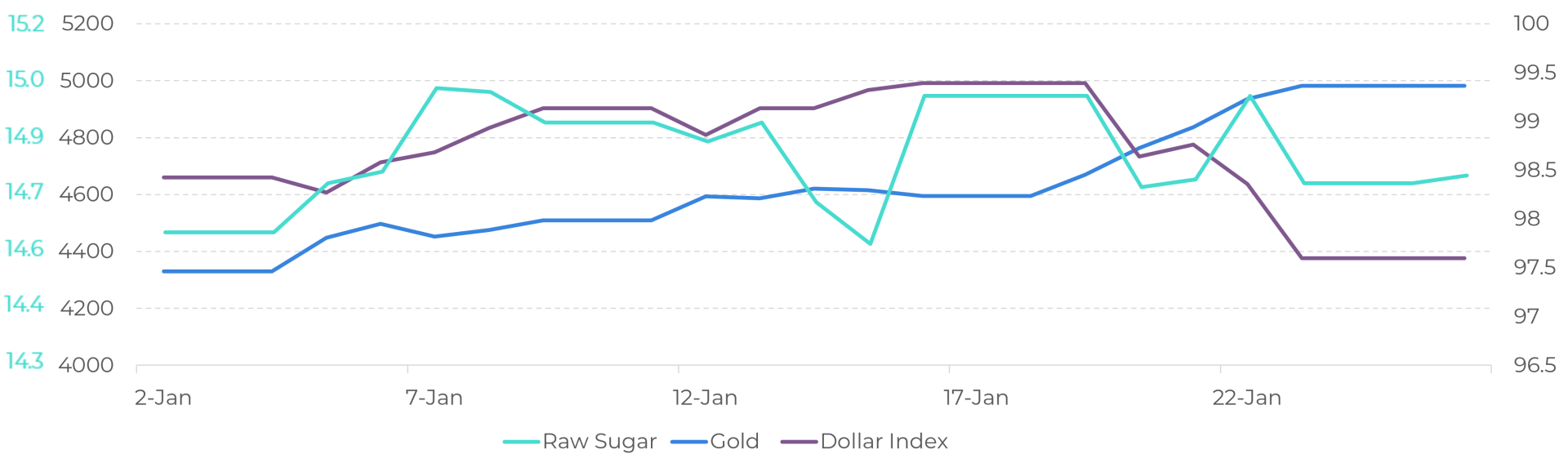

- The shortened week opened with strong bearish pressure on sugar due to higher global risk sentiment amid U.S.–EU geopolitical tensions.

- Sugar fell 1.6% while safe‑haven metals surged; markets stayed geopolitically driven through mid‑week, marked by The World Economic Forum.

- Sentiment improved Thursday (22) after the U.S. eased tariff threats and ruled out forceful Greenland acquisition, helping sugar rebound 1.5%.

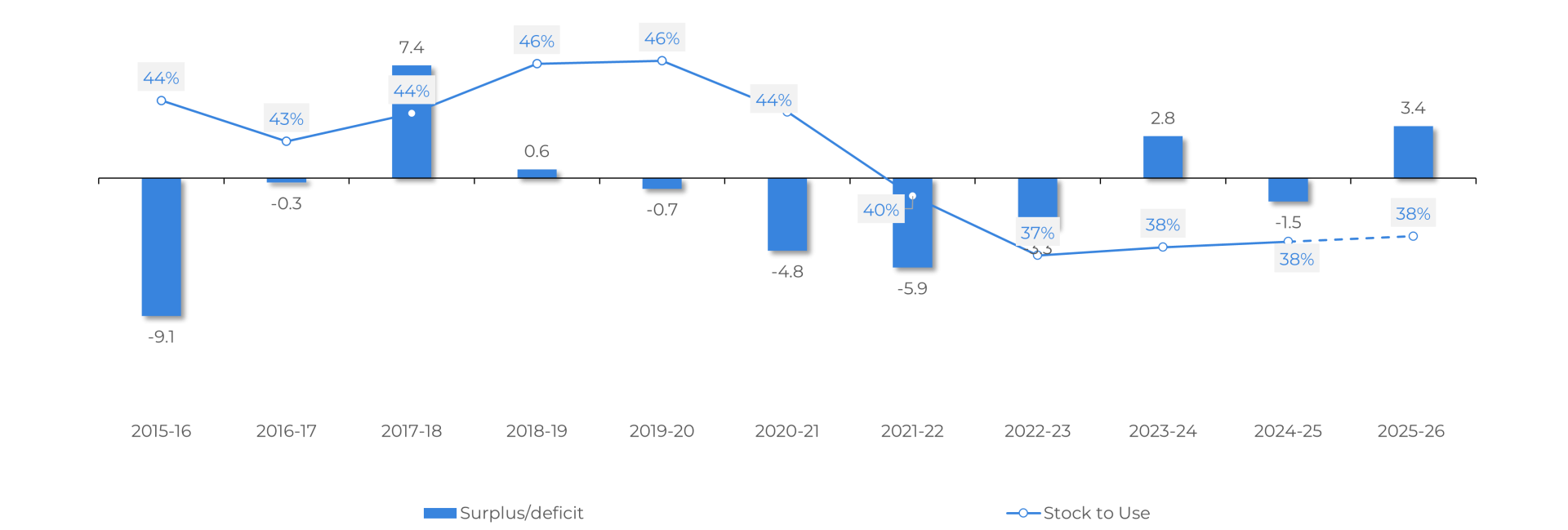

- Fundamentals remain broadly bearish as Brazilian CS output stays strong, with the season likely reaching 610 Mt of cane and 40.5 Mt of sugar.

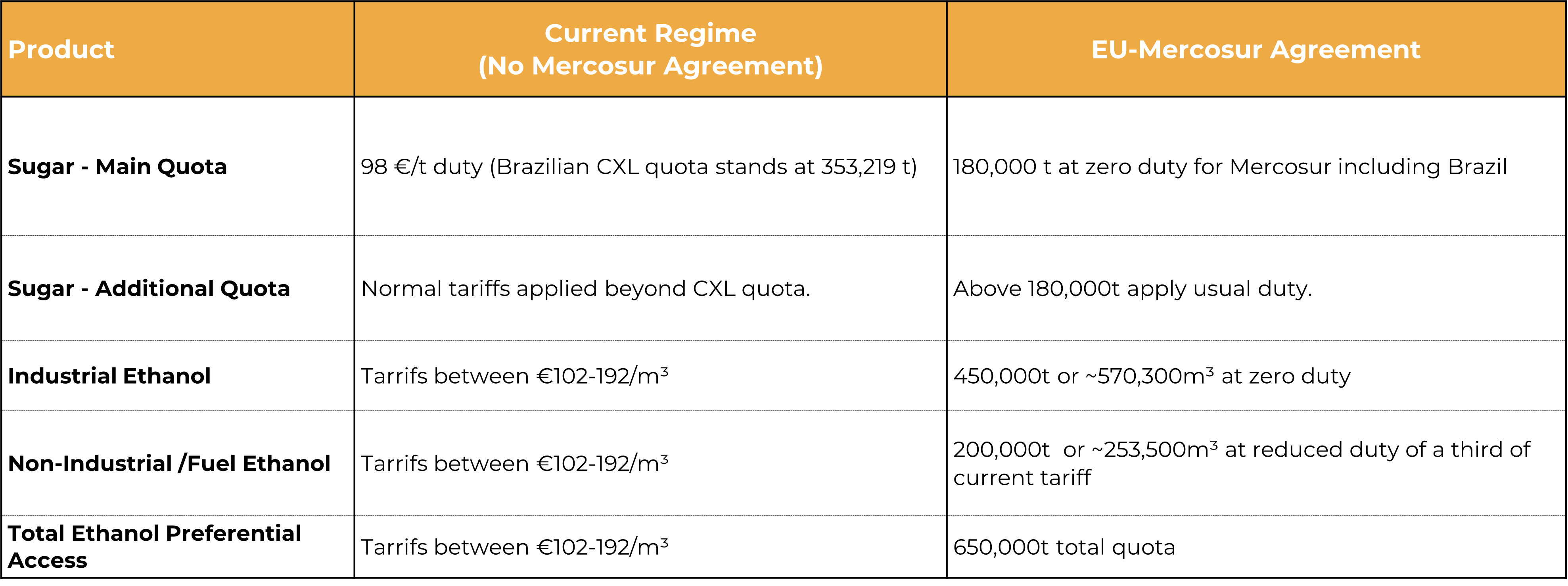

- Global supply recovery, India, Mexico, Thailand, China, U.S., EU, adds to the surplus, while the EU–Mercosur deal may slightly increase competitive pressures and expand ethanol opportunities for Brazil.

Risk-off sentiment and ample supply keep sugar under pressure

Last week was shorter due to the US holiday and the extended weekend, and sugar prices opened on Tuesday under strong bearish momentum driven by heightened risk sentiment. Over the weekend, President Trump discussed potential tariff increases on certain European allies as leverage in negotiations related to the possible US purchase of Greenland.

Raw sugar fell 1.6% during Tuesday (20), while metals, particularly gold, considered a safe haven asset; gained more than 3.7%. Although the sweetener showed slightly more stability the following day, geopolitics remained the primary source of friction in global markets. With rising tensions between the EU and the US, both the dollar and US Treasury bonds weakened, while gold and silver continued to appreciate.

Sugar (c/lb) x Gold (USD/oz) x Dollar Index

Source: LSEG

On Thursday (22), sentiment shifted to risk off after Trump announced the suspension of plans to impose new tariffs on the EU and clarified that the US would not use force to acquire Greenland. This was generally supportive of commodities, except for the energy complex, which had been benefiting from lingering uncertainty. Sugar prices rebounded by 1.5% on Thursday, ultimately closing the week at a lower level of 14.7 c/lb on Friday.

From a fundamental’s perspective, the sweetener market remains broadly unchanged, with Brazilian output still expected to be solid. According to the latest UNICA report, Center-South mills crushed 2.17 Mt of cane in the second half of December, up from 1.71 Mt in the same period of the 2024/25 season. Since the start of the 2025/26 crop, cumulative crushing has reached 600.40 Mt, only 2.28% below last year, suggesting that if this pace holds, the region could finish the season near 608 Mt. Our view is slightly more optimistic, placing final output closer to 610 Mt. With a sugar mix of 50.6%, total sugar production would approach 40.5 Mt, helping explain the prevailing bearish tone in the market.

As highlighted in the previous report, the recovery in several key origins, most notably India, comes on top of an already ample global supply backdrop. Mexico is also expected to perform well, with Conadesuca projecting a 12% rebound in sugar production in 25/26. Thailand should add roughly 500 kt to its yearly output, though still operating below its historical potential, while China is estimated by the China Sugar Association to reach 11.2 Mt. Other regions, including the US and the EU, are set for solid, albeit not exceptional, results. In the US, sugar production is forecast to be 0.6% lower than last year but remains 0.8% above the five year average. For the EU plus the UK, net sugar output is expected to fall 4% compared with 2024/25 yet still stands about 2% above the five year average.

Global Sugar Supply and Demand (Oct - Sep | Mt rv)

Source: Hedgepoint

Summary of trade adjustments given the possible Mercosur Agreement

Source: Agrideriaindustrialllc, Energynews, Hedgepoint

Summary

Last week’s shortened session saw sugar pressured by U.S.–EU geopolitical tensions, which boosted risk aversion and lifted safe haven metals. Markets steadied only after the U.S. softened its tariff stance on Thursday, allowing sugar to recover part of its losses before ending slightly lower at 14.7 c/lb. Fundamentally, the market remains weighed down by strong Brazilian output, likely near 610 Mt of cane and over 40 Mt of sugar, alongside broad production recoveries in India, Mexico, Thailand, China, the U.S., and the EU. The nearing EU–Mercosur deal is expected to marginally shift sugar trade flows while significantly improving Brazil’s access to the EU ethanol market within quotas.

Weekly Report — Sugar

Reviewed by Laleska Moda

laleska.moda@hedgepointglobal.com

Disclaimer

This document has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without intending to create obligations or commitments to third parties. It is not intended to promote or solicit an offer for the sale or purchase of any securities, commodities interests, or investment products.

To access this report, you need to be a subscriber.

Contact us

Check our general terms and important notices.

We have updated our Terms & Conditions to reflect improvements to our platform, data handling practices, and the overall experience we provide to our clients.