Brazilian Center-South 2026/2027 preliminary view

- Sugar prices have remained range‑bound at 14-15¢/lb, reflecting expectations of a surplus in 2025/26 balance and heavy trade flows.

- Brazil is the main driver of the oversupply, with strong Center‑South output in 2025/26 and early signs pointing to another solid 2026/27 crop.

- Under a max‑sugar scenario (50.6% mix), production could reach 42.4 Mt, generating a ~4 Mt surplus in global trade flows.

- Reducing the sugar mix to ~46% would rebalance sugar but require lower hydrous prices to absorb excess ethanol, implying a ~13.5¢/lb sugar floor.

- A more realistic 48% sugar mix reduces, but does not eliminate, the surplus, keeping prices bearish and drifting toward the seasonal floor.

Brazilian Center-South 2026/2027 preliminary view

The sugar market has remained stable within a relatively low trading range for an extended period, between 14 to 15c/lb. Prices have failed to recover, largely reflecting market consensus around a surplus in the supply-demand balance for the 2025/26 (Oct–Sep) season, besides an also over-supplied trade flow.

A significant share of this surplus comes from another strong performance in Brazil, alongside improving results across the Northern Hemisphere. The Brazilian Center South 2025/26 crop year is approaching its end, signaling a strong sugar output. We currently estimate crushing at approximately 610 Mt of cane – moving closer to our first estimate, with a 50.6% sugar mix, resulting in around 40.5 Mt of sugar production.

Adding to the bearish global outlook is the early view of the 2026/27 Brazilian season. While it remains early to draw firm conclusions, early rainfall patterns and favorable Vegetation Health Index (VHI) point to the potential for another year of solid production, reinforcing expectations of continued ample global supply. Our preliminary estimates suggest that, despite incomplete realized data, considering that the critical development window for sugarcane falls between October and February, it is possible to reach up to 630 Mt of cane. At that raw material availability level, price direction will largely depend on the sugar mix. Therefore, in this report, we will work on some scenarios.

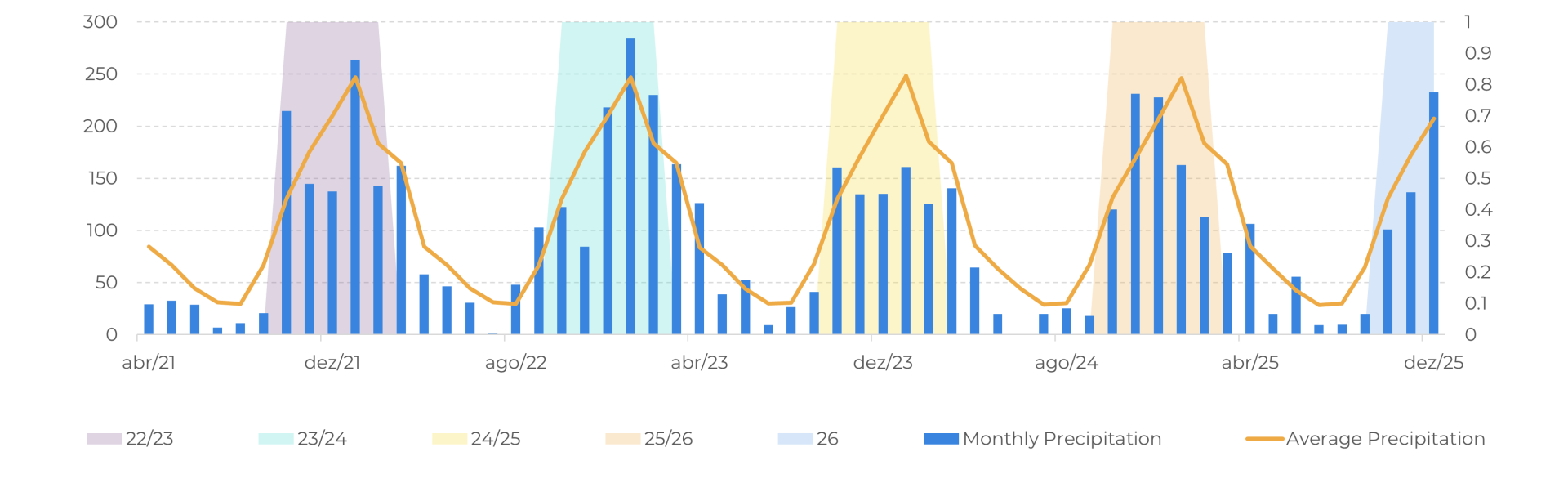

Rainfall in CS x cane development period (mm)

Source: UNICA, Hedgepoint

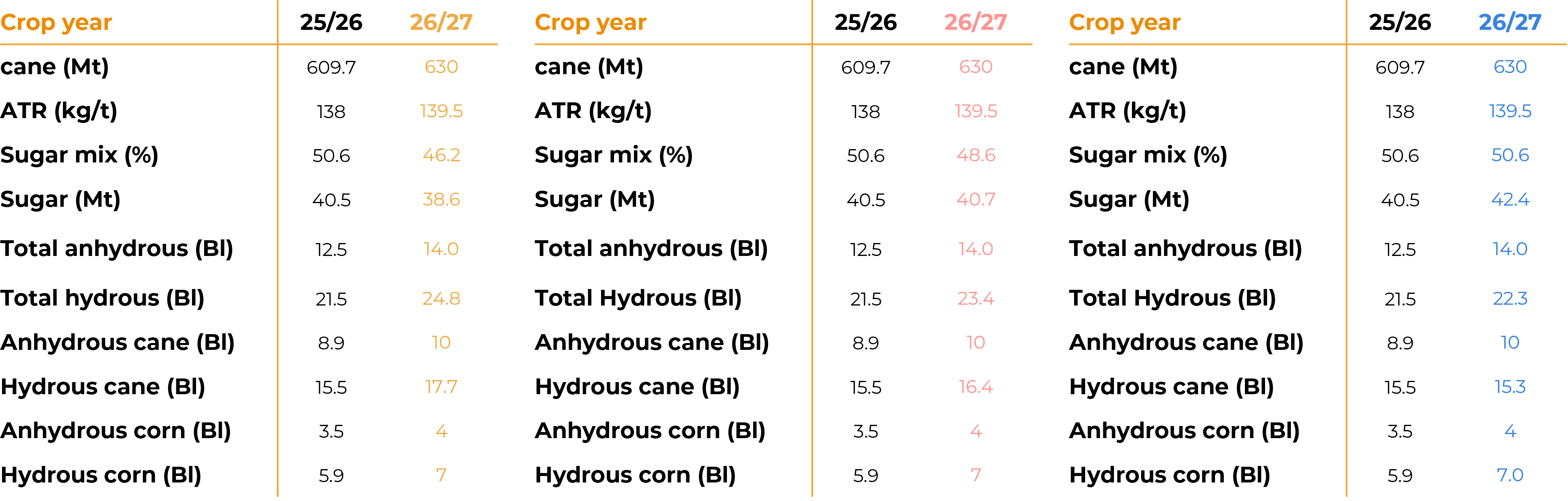

As common assumptions across all scenarios, we consider 630 Mt of cane crush, 139.5 kg/t of TRS, 11 billion liters of corn ethanol production, and Otto‑cycle growth of 2.5% over the season.

For the first scenario, let us assume that mills could continue maximizing sugar output, maintaining the same operating pace observed in the 2025/26 season and achieving a 50.6% sugar mix. Under this exercise, total sugar production would reach approximately 42.4 Mt, with exports from the Center‑South estimated at around 33.5 Mt. In this context, global trade flows would adjust accordingly, resulting in the accumulation of an estimated 4 Mt sugar surplus between Q4‑2025 and Q1‑2027, reinforcing an oversupplied outlook and limiting upside potential for prices. This scenario is unlikely, as it implies a sustained expansion of sugar output despite both an already oversupplied situation and relative price signals that currently favor ethanol over sugar in Brazilian production decisions.

What sugar mix would be required to smooth these trade flows, and what price level would that imply? These are the key questions addressed in our second scenario.

To offset 4 Mt of sugar production, the sugar mix would need to decline to approximately 46%. However, such a shift would inevitably lead to a build‑up of ethanol stocks.

Trade flow - Sugar mix 50.6% (left) and 46.2% (right) in '000t tq

Source: Hedgepoint

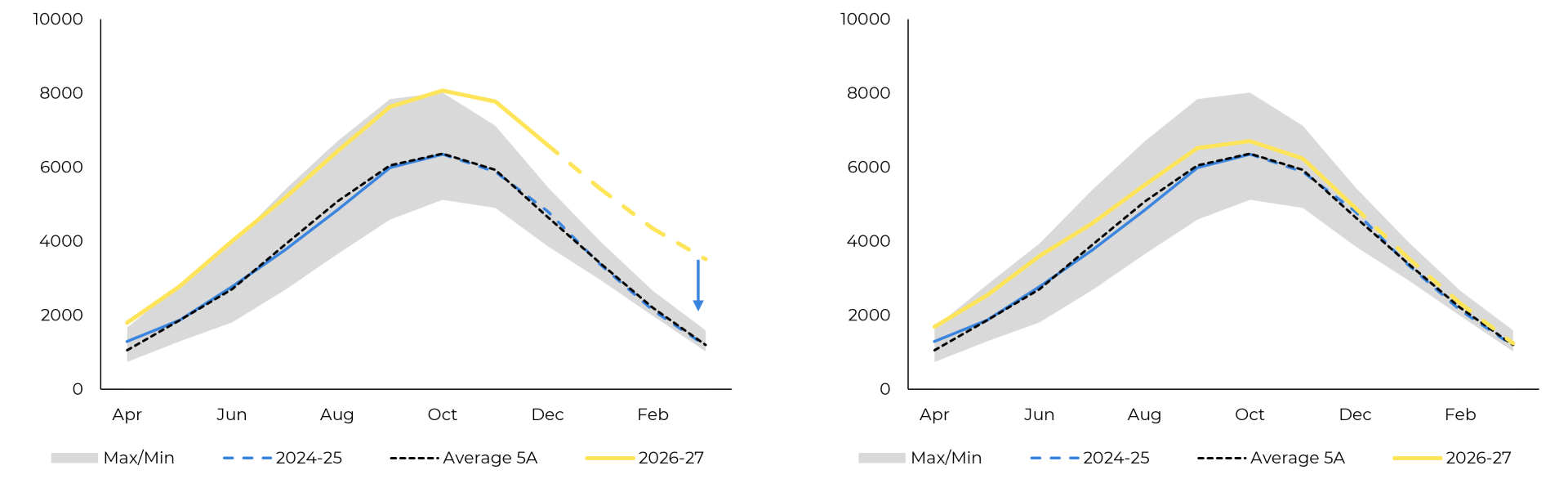

Hydrous Stock un ‘000 m³ - before (left) and after (right)

Source: UNICA, SECEX, ANP, Hedgepoint

Crop estimate considering a sugar mix of 46.2% (left), 48.6% (middle) and 50.6% (right)

Source: UNICA, Hedgepoint

Note: both 46.2% and 48.6% scenarios would need prices to induce higher hydrous consumption to stabilize stocks.

Summary

The sugar market remains structurally oversupplied, with Brazil at the center of both current and forward looking bearish pressure. Even under more conservative assumptions on the sugar ethanol mix, global trade flows are unlikely to fully rebalance, limiting upside potential for prices. While aggressive ethanol demand reallocation could theoretically clear the surplus, operational frictions and pricing constraints make a partial adjustment more likely.

Weekly Report — Sugar

Reviewed by Laleska Moda

laleska.moda@hedgepointglobal.com

Disclaimer

This document has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without intending to create obligations or commitments to third parties. It is not intended to promote or solicit an offer for the sale or purchase of any securities, commodities interests, or investment products.