Live With Experts - Sugar Market Key Points

Executive Summary

Sugar prices experienced sharp volatility throughout March and early April, largely driven by geopolitical escalation and its effects on the energy complex and logistics rather than any material change in underlying sugar fundamentals. The intensification of tensions between the United States and Iran generated a renewed risk premium across financial markets, lifting oil and LNG prices and triggering short covering activity in the sweetener.

Raw sugar briefly traded above 16.0 c/lb, while white sugar premiums widened temporarily, reflecting logistical sensitivities related to refinery locations. However, as energy prices corrected and geopolitical risk eased, sugar prices lost momentum, reinforcing the view that recent rallies were technical and macro driven rather than structurally supported.

Geopolitics and Macroeconomics Overview

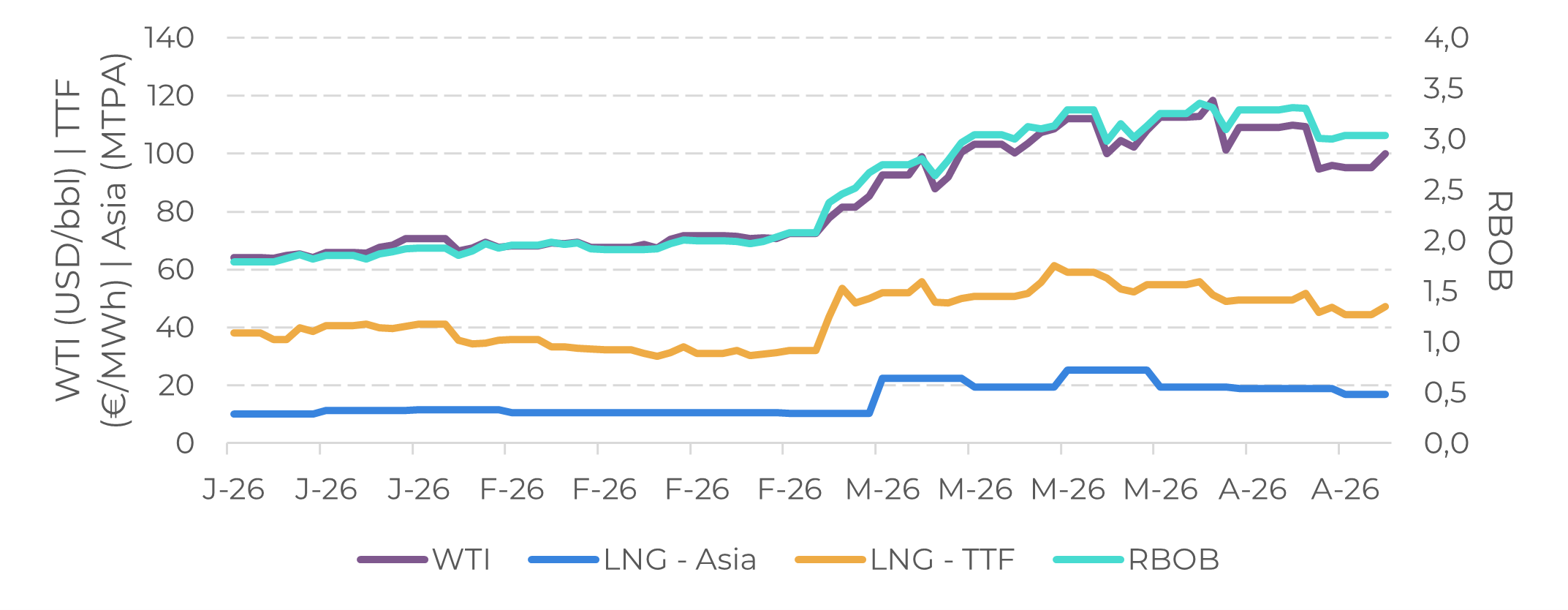

Geopolitical developments were especially relevant through their transmission into the energy complex between March and early May. Attacks on energy infrastructure in the Middle East intensified concerns over long term energy supply, pushing prices higher and increasing inflationary risks for energy dependent economies. For the sugar market, this translated into short lived support through expectations of a full cost pass-through from Petrobras, which is a net importer of gasoline. Sugar prices rose fast as they triggered short covering, as many expected ethanol to benefit from gasoline’s higher prices, inducing a higher demand and a lower mix in the biggest sugar producer. Nonetheless, with no passthrough, as oil and LNG prices corrected, this support diminished.

Figure 1 – Key Energy Contracts

Source: Bloomberg, LSEG

From a macroeconomic perspective, risk aversion rose sharply alongside the escalation of geopolitical tensions. The VIX index climbed materially during the period, while safe haven assets such as gold appreciated against the US dollar. Central banks reacted cautiously: the Federal Reserve opted to keep rates unchanged amid uncertainty over inflation persistence, while Brazil’s COPOM delivered a 25 bp cut, citing signs of domestic economic cooling despite inflation remaining above target. Although the interest rate differential continues to offer some support to the BRL, elevated global uncertainty limits currency stability and increases exposure to capital flow volatility.

Figure 2 – VIX Index: +12.9 Jan-2 vs Apr-6

Source: CFTC, Hedgepoint

Fundamentals

Center-South and price dynamics

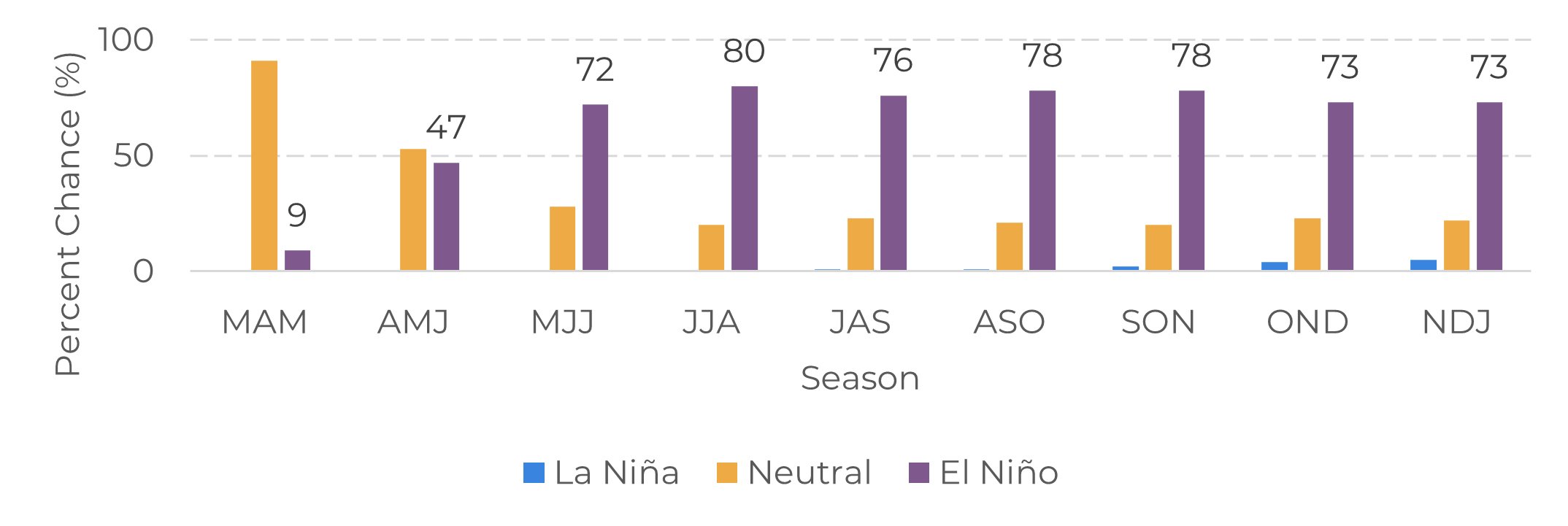

Brazil remains the dominant force shaping global sugar dynamics. The 2025/26 Center South crop is expected to exceed 40 million tons of sugar, supported by cane crushing close to 608 million tons and a high sugar mix – 50.4%. Export availability may surpass 31 million tons, reinforcing Brazil’s role as the world’s largest supplier. Weather conditions throughout 2026/27 planting and development cycle were largely favorable, with cumulative precipitation and vegetation health indicators remaining close to or above historical averages.

Main Risks

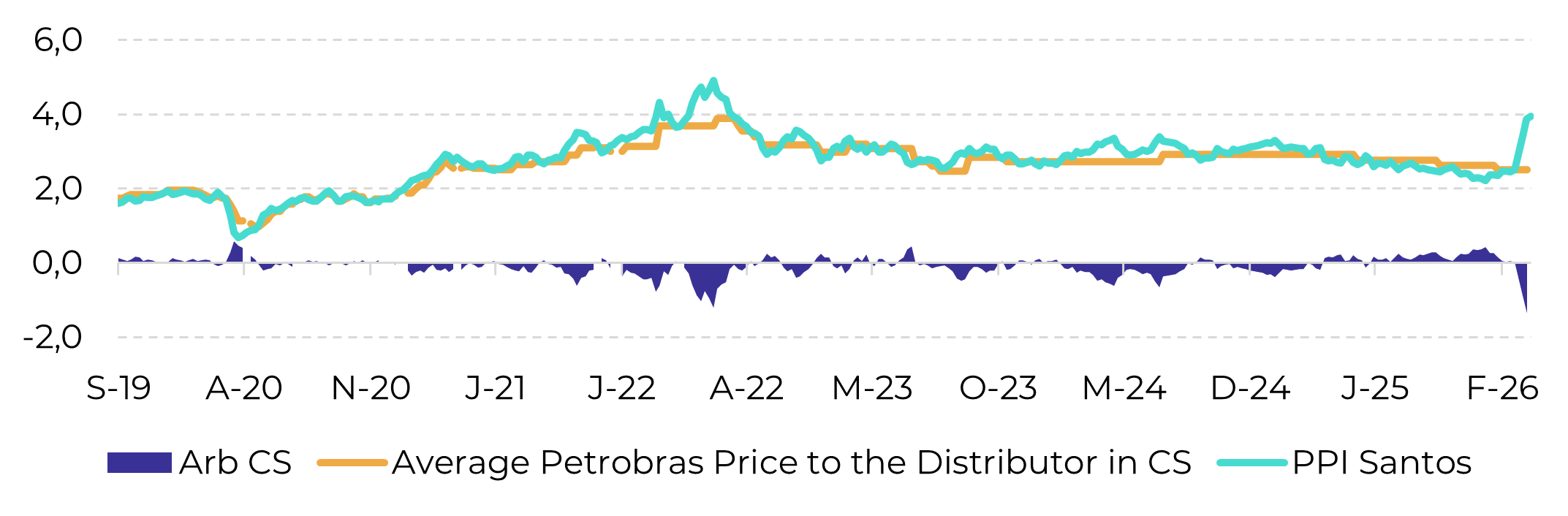

Figure 3 – Petrobras’ average import arbitrage in the Center-South region (BRL/liter)

Source: ANP, Bloomberg, Hedgepoint

Figure 4 – ENSO Probability

Source: International Research Institute for Climate and Society (IRI)

Summary

In conclusion, while geopolitical shocks and energy volatility may continue to generate short term price dislocations, the global sugar market remains structurally bearish. Brazil’s production strength, combined with partial recoveries elsewhere, keeps supply ample and caps sustained price appreciation. Monitoring weather evolution, ethanol parity, and geopolitical developments remain essential, but for now, fundamentals dominate the medium term outlook.

Weekly Report — Sugar

Reviewed by Laleska Moda

laleska.moda@hedgepointglobal.com

Disclaimer

This document has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without intending to create obligations or commitments to third parties. It is not intended to promote or solicit an offer for the sale or purchase of any securities, commodities interests, or investment products.

To access this report, you need to be a subscriber.

Contact us

Check our general terms and important notices.

We have updated our Terms & Conditions to reflect improvements to our platform, data handling practices, and the overall experience we provide to our clients.