The Surplus Saga: Is there a silver lining?

- Global trade flows are in surplus due to, mostly, strong Brazilian supply.

- The Center-South drives the global balance, with mix flexibility toward ethanol partially absorbing excess sugar.

- Sugar pricing is increasingly linked to ethanol parity, requiring lower prices to stimulate fuel demand and rebalance the market.

- Measures such as E32 or fuel price pass-through could raise the price floor by boosting ethanol demand without further mix adjustments.

- Ample availability keeps near-term prices range-bound, while bullish expectations are deferred to future contracts, reflected in the forward curve.

The Surplus Saga: Is there a silver lining?

The global sugar market is currently navigating a phase characterized by structurally resilient demand, though slower than in the past, and a short-term supply-driven imbalance. Consumption continues to expand, primarily supported by population growth and rising incomes in emerging markets, as discussed in our previous report (link). However, excess supply, particularly from Brazil, has shifted trade flows into surplus, exerting sustained downward pressure on short-term prices.

Within this context, Brazil’s ethanol domestic market has become the key adjustment mechanism to absorb most part of the sugar surplus and restore a degree of equilibrium. For this rebalancing to materialize, additional fuel demand must be stimulated through price adjustments. In this environment, macroeconomic volatility, geopolitical tensions, and energy market dynamics, by reinforcing cost-side pressures, are acting as possible sources of short-term price-support.

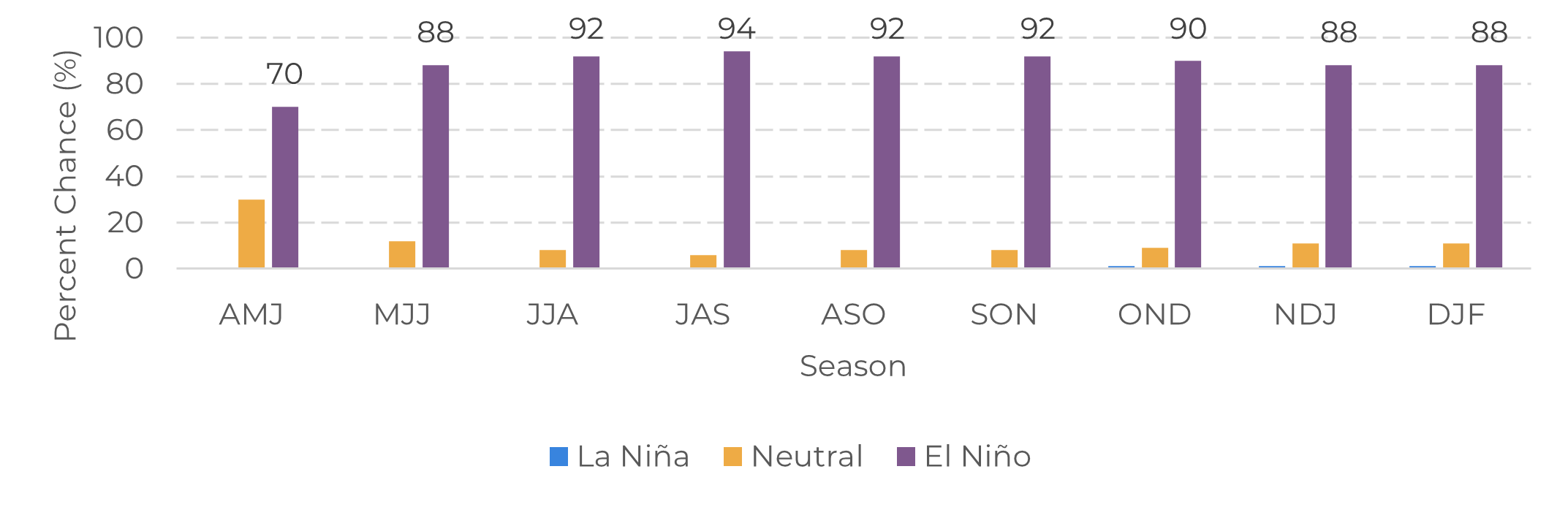

To fully understand the current scenario, it is essential to analyze the supply side of the equation. While regional divergences continue to shape the global balance, the overall supply outlook remains comfortable. In the Northern Hemisphere, India continues to represent the main downside risk, while Thailand and the Americas partially offset this weakness throughout the 2025/26 season. The outlook for 2026/27, however, is more uncertain. The potential development of an El Niño pattern could jeopardize key production recoveries, particularly in those regions.

Chances of an El Niño (%)

Source: IRI, Hedgepoint

Even so, supply disruptions would have to be severe to outweigh Brazil’s capacity to rebalance the market through adjustments in its production mix. As the central driver of the global surplus, Brazil is expected to deliver another strong c[LR2.1]ycle in the 2026/27 season, with Center-South cane production approaching approximately 635 Mt. Notably, while most producing regions would be adversely affected by an El Niño event, the Center-South 2027/28 season could benefit from such conditions, especially if they persist into the region’s summer period.

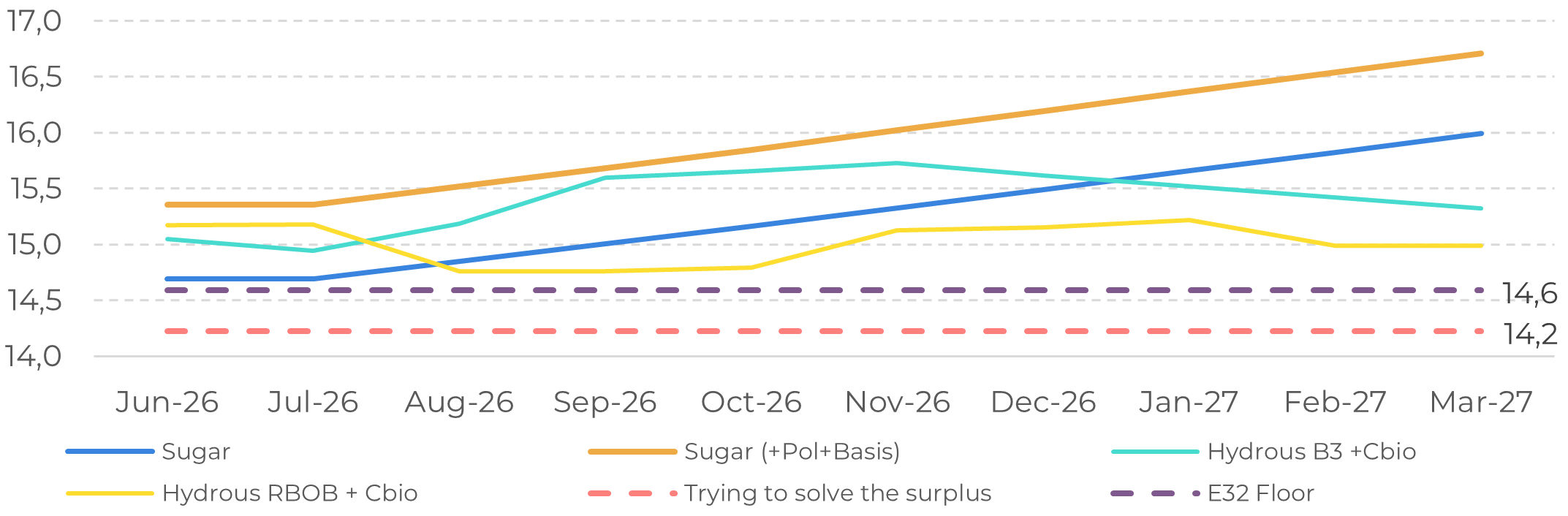

Price parity and floor considering hydrous (c/lb)

Source: Bloomberg, Hedgepoint

Another policy channel that could support a higher price floor would be a full cost pass-through by Petrobras. This would translate into higher gasoline prices and, through energy price equivalence, allow for higher biofuel prices at the pump without compromising demand creation. Consequently, the sugar price floor would also increase, potentially reaching 18c/lb.

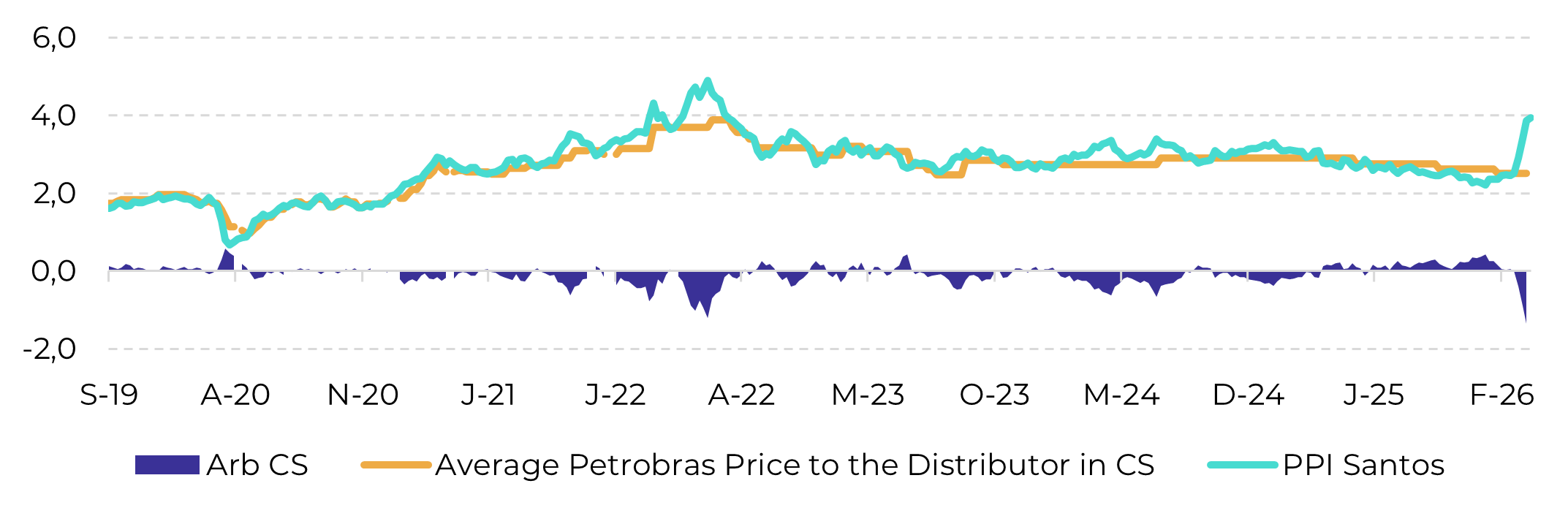

Petrobras’ average import arbitrage in the Center-South region (Reais/liter)

Source: ANP, Bloomberg, Hedgepoint

Nevertheless, given the current election-year environment and the absence of definitive policy decisions, the market has reverted to a more bearish stance. After testing the 15.4 c/lb level, prices have retreated, suggesting a short-term trading range broadly between 14.5 and 15.5 c/lb.

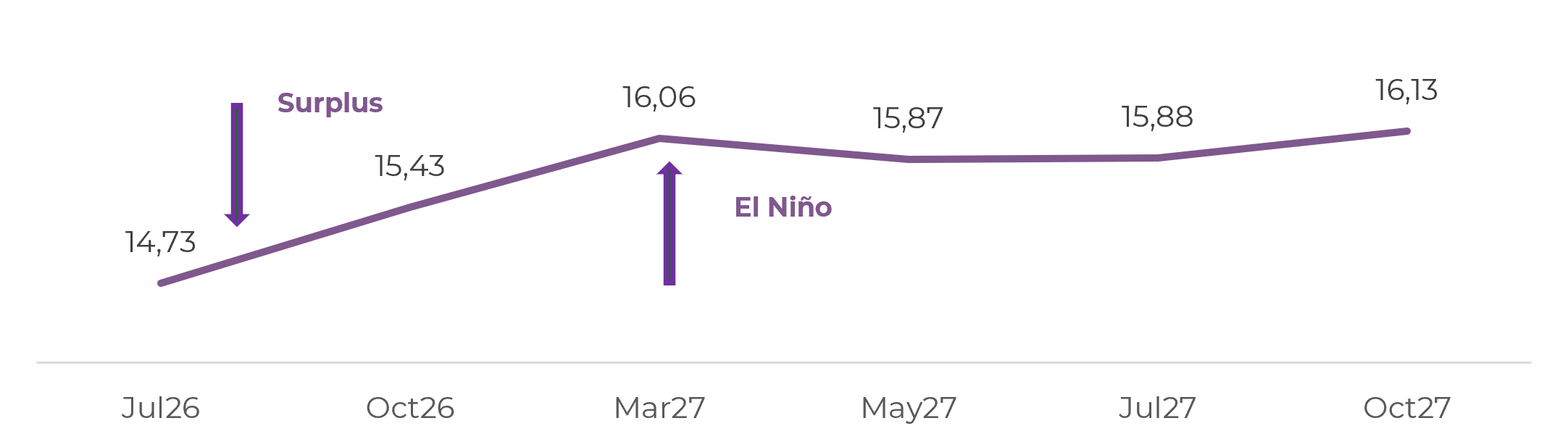

Raw sugar future prices (c/lb)

Source: LSEG, Hedgepoint

Summary

The global sugar market remains at a surplus, largely driven by Brazil’s outsized production. While regional supply risks—particularly those linked to El Niño—may introduce temporary disruptions, they are unlikely to materially alter the overall balance unless significantly severe. This impact, however, is being priced in the future curve, with its current slope and spread structure.

Brazil’s ethanol market continues to serve as the primary adjustment mechanism in the short term, with price-driven demand creation acting as the key channel for rebalancing. However, this process is gradual and dependent on both market dynamics and policy developments, such as potential changes to blending mandates or fuel pricing frameworks.

Weekly Report — Sugar

Reviewed by Thaís Italiani

thais.italiani@hedgepointglobal.com

Disclaimer

This document has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without intending to create obligations or commitments to third parties. It is not intended to promote or solicit an offer for the sale or purchase of any securities, commodities interests, or investment products.

To access this report, you need to be a subscriber.

Contact us

Check our general terms and important notices.

We have updated our Terms & Conditions to reflect improvements to our platform, data handling practices, and the overall experience we provide to our clients.