Live with Experts – Highlights of the Sugar Market

Live with Experts – Highlights of the Sugar Market

Macroeconomic and Price Outlook

The current global sugar market environment continues to be strongly influenced by macroeconomic and geopolitical factors, which have been contributing to increased volatility and shifts in price dynamics and trade flows. The escalation of tensions in the Middle East has led to a significant rise in the global risk premium, reinforcing the search for safe-haven assets and directly impacting the energy market. This trend has broad implications for the commodities chain, as oil and natural gas are essential inputs for both production and logistics. Disruptions to strategic transport routes, combined with rising energy costs, resulted in higher freight rates and the reconfiguration of supply chains, putting pressure on costs throughout the entire sugar chain.

Additionally, the Middle East plays a significant role in fertilizer production, particularly nitrogen-based fertilizers, which are widely used in sugarcane cultivation. Rising costs for these inputs could negatively impact agricultural yields, especially in Northern Hemisphere regions that depend on them.

Furthermore, inflationary pressure stemming from rising energy costs has limited the room for maneuver of major central banks, leading to the maintenance of high interest rates for longer periods. In the United States, persistent inflation has resulted in the continuation of restrictive monetary policy, contributing to the stability of the dollar and the interest rate differential relative to emerging economies such as Brazil.

In the Brazilian domestic market, the pass-through of international energy prices to fuel prices has been partial. Despite the global rise in oil prices, there was no full pass-through to domestic gasoline prices, due to political decisions and pricing strategies. However, adjustments to distributor and gas station margins have led to higher prices for the end consumer, partially boosting the competitiveness of hydrous ethanol. This perception of risk spurred a wave of short-covering by funds in the sugar market, although such support proved limited given the prevalence of bearish fundamentals.

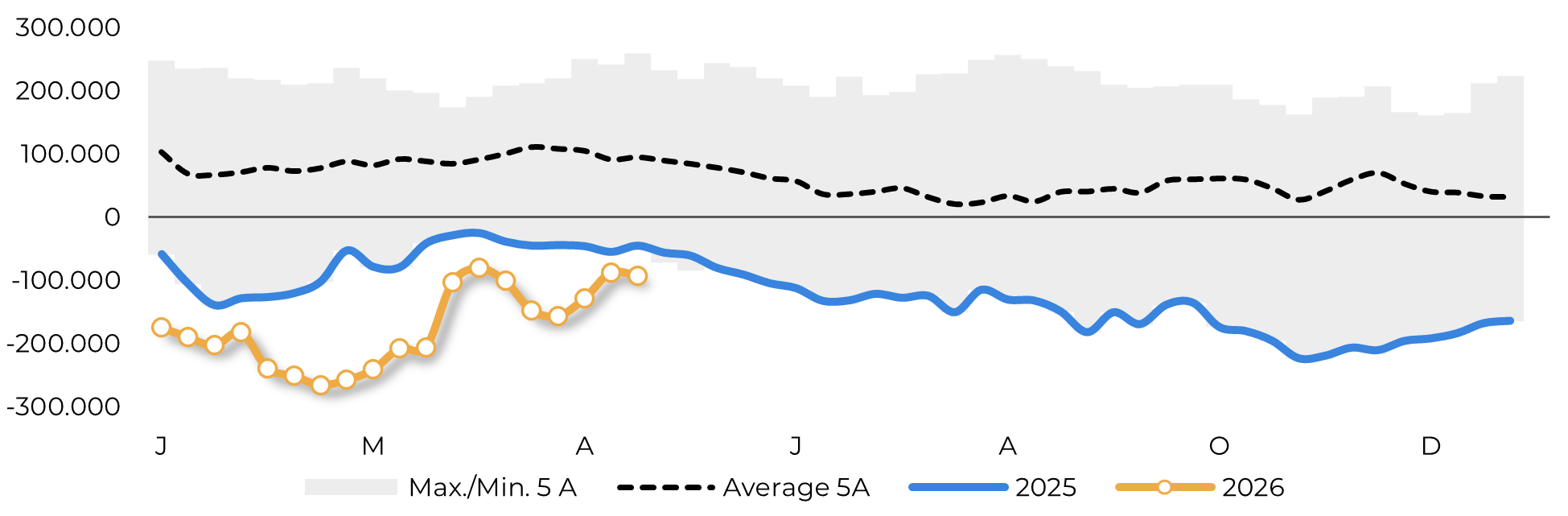

From a fundamentals’ perspective, the global market remains characterized by oversupply. Even amid macroeconomic noise, global availability remains high, supported mainly by robust production performance in Brazil’s Center-South region and a partial recovery in the Northern Hemisphere. In this context, funds maintain net short positions above the historical average, reflecting expectations of a continuing global surplus.

Speculative net position (contracts)

Source: CFTC, Hedgepoint

Northern Hemisphere

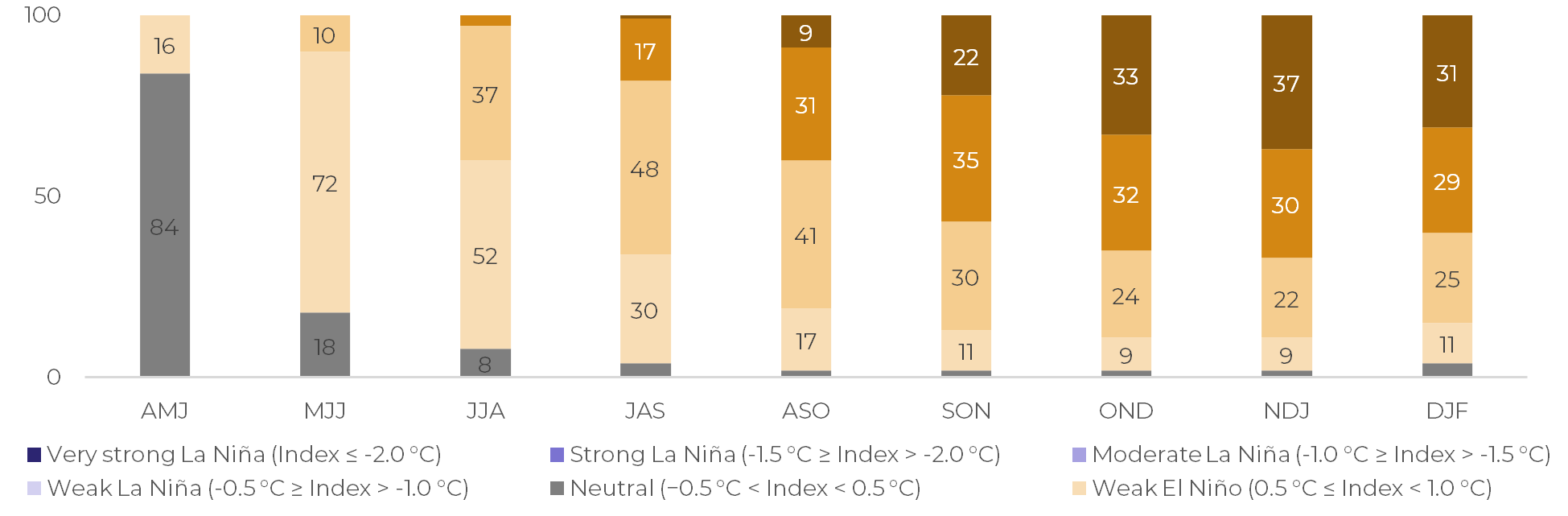

In the Northern Hemisphere, India remains the main risk factor for supply. Production in 25/26 fell short of initially expected potential, resulting in export restrictions and lower inventory levels. For the next cycle, expectations point to a limited recovery, with the possibility of the country’s absence from the export market. This scenario is heavily influenced by weather patterns, particularly the development of El Niño, which could negatively impact the monsoon season and limit yields.

Thailand, in turn, performed better than expected in the current cycle, partially offsetting India’s lower availability. However, for next year, a decline in production is projected due to more adverse weather conditions, typical of El Niño events, which tend to bring higher temperatures and reduced rainfall in the region.

China is also contributing to the increase in global supply in the short term, with record production (over 12 Mt in 2025/26) and a significant increase in imports (40% compared to the previous harvest), part of which is directed toward building strategic stocks. However, this accumulation may slow the pace of future imports, depending on the evolution of domestic production.

In Central America and Mexico, recent results have been positive, with increases in yields and production. Nevertheless, these regions remain vulnerable to adverse weather conditions in the coming cycle, which could limit future supply.

Brazilian Center-South

In Brazil, the Central-South harvest is performing solidly, with high crushing levels and sugarcane production expected to reach 635 million tons in 26/27 and may even exceed that level. Weather conditions have been favorable so far, with expectations close to the historical average, which should support a robust harvest. The production mix, however, tends to be more alcohol-oriented, reflecting the lower attractiveness of sugar in the face of global oversupply.

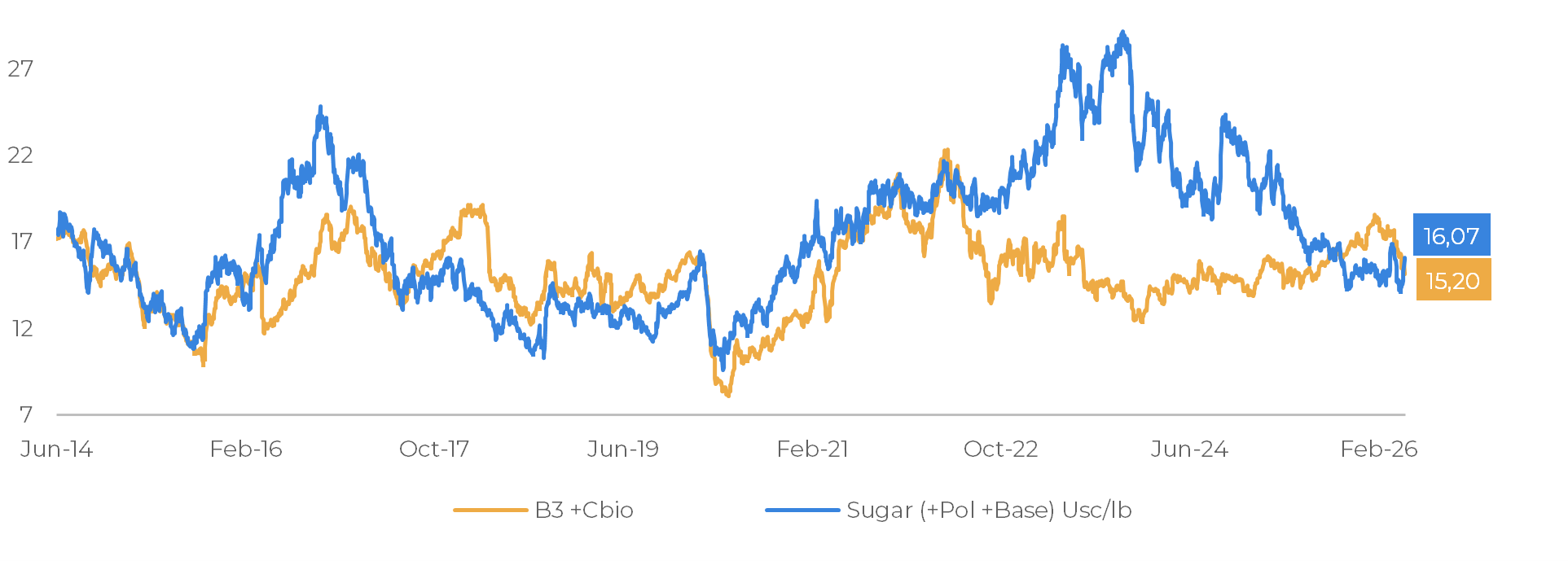

Historical parity: sugar vs. hydrous ethanol

Source: LSEG, Hedgepoint

The dynamics between sugar and ethanol become central in this context. The drop in international sugar prices has brought its competitiveness closer to that of ethanol, encouraging a reconfiguration of the production mix. The strategy for absorbing the sugar surplus therefore involves increasing ethanol production and consumption in the domestic market. This implies lower prices for the biofuel, with the aim of stimulating demand and balancing the market.

However, this adjustment occurs imperfectly. The existence of advanced price fixings and price dynamics limits the speed and intensity of the shift in the mix, leading to an intermediate level that does not completely eliminate the global surplus, currently estimated at 47.5%. Even with this realignment, the market still has a surplus estimated at around three million tons.

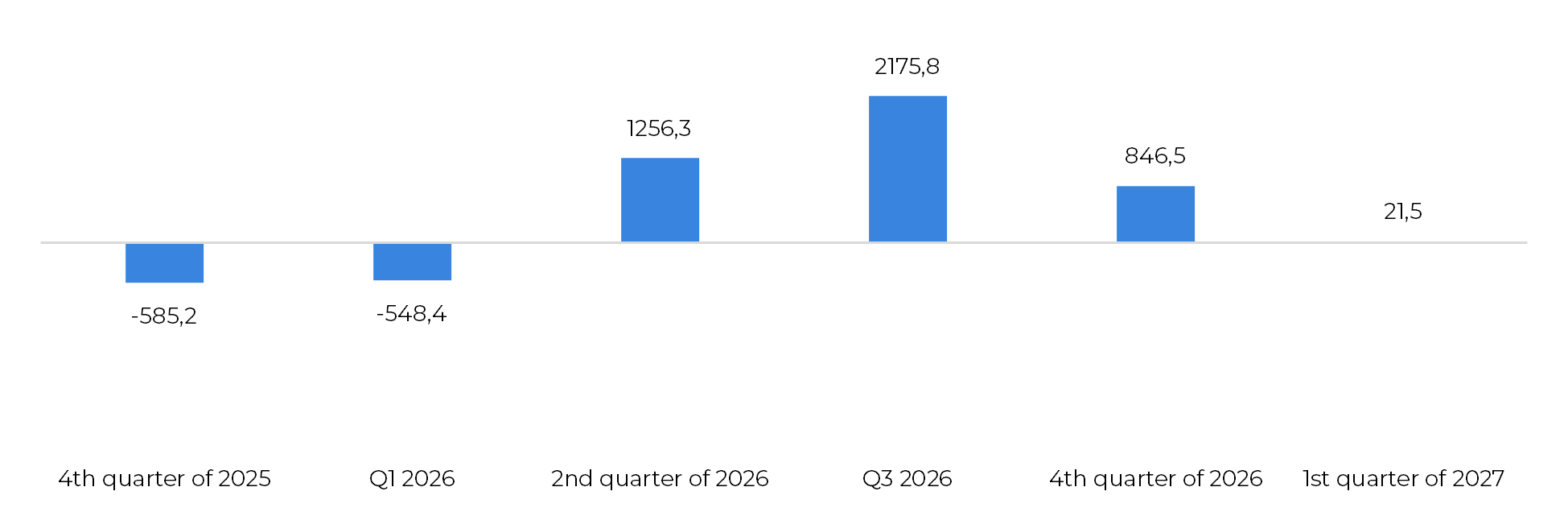

Total trade flows (‘000t tq)

Source: Green Pool, Hedgepoint

Risks

Among the main risks are exchange rate volatility — especially in the context of Brazil’s upcoming elections — and pricing decisions by the state-owned oil company. A full pass-through of international fuel prices would significantly raise the cost of gasoline, boosting ethanol’s competitiveness and, consequently, supporting its prices and those of the sweetener. It is estimated that the sugar floor price would rise from 14 c/lb to approximately 18 c/lb in the event of a full pass-through without subsidies.

ENSO Intensity Probabilities (May 2026)

Source: NOAA, Hedgepoint

On the other hand, Brazil retains the capacity to offset these losses, either through increased production or adjustments to the mix, limiting any significant rise in sweetener prices. This flexibility reinforces the country’s role as the primary stabilizing force in the global market. However, this dependence also increases price sensitivity to potential local climate shocks.

Summary

In summary, the global sugar market is experiencing a sustained surplus, putting downward pressure on prices in the short term. However, climate risks and macroeconomic factors could introduce volatility and pave the way for upward price movements in the medium term. Brazil remains the key variable, both due to its high production levels and its flexibility in shifting production between sugar and ethanol, thereby consolidating its central role in global price formation.

Weekly Report — Sugar

laleska.moda@hedgepointglobal.com

Disclaimer

This document has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without intending to create obligations or commitments to third parties. It is not intended to promote or solicit an offer for the sale or purchase of any securities, commodities interests, or investment products.