Live with Experts – Highlights of the Sugar Market

Live with Experts – Highlights of the Sugar Market

Macroeconomic and Price Outlook

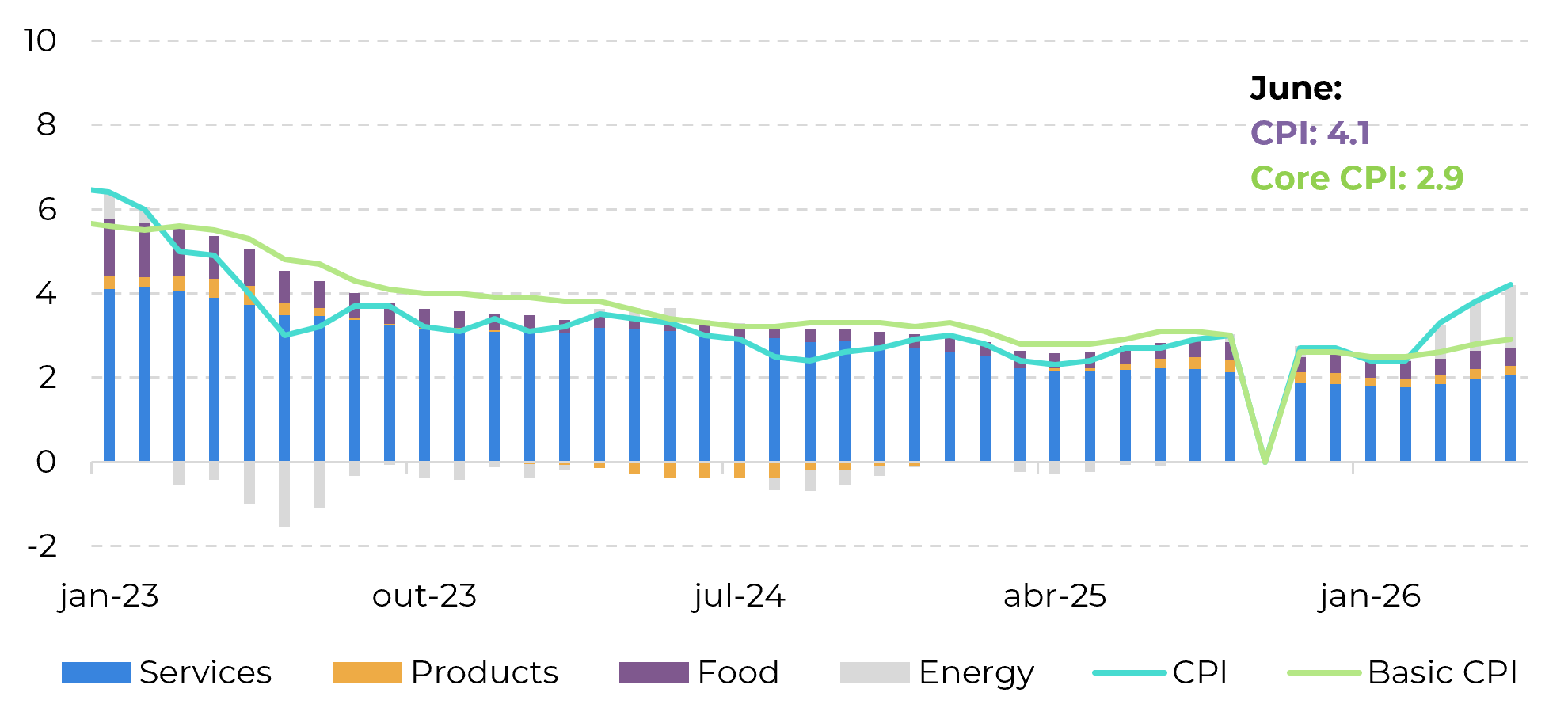

The market continues to monitor the effects of the conflict in the Middle East, persistent global inflation, and the maintenance of high interest rates in major economies. Weaker U.S. employment data temporarily reduced support for the dollar and favored a recovery in commodities over the past week by dampening expectations of U.S. interest rate hikes. Nevertheless, the Fed is likely to continue monitoring inflation to determine its monetary policy, as inflation remains above the 2% target due to the fallout from the conflict with Iran.

U.S. Consumer Price Index (CPI)

Source: Bloomberg

In terms of sugar, the recent price recovery was driven by funds covering short positions amid growing concerns about the 2026/27 Northern Hemisphere crop. Despite this, current supply remains high and limits more significant upward movements. Technically, the raw sugar contract encountered resistance near 15.5 c/lb.

Northern Hemisphere

India

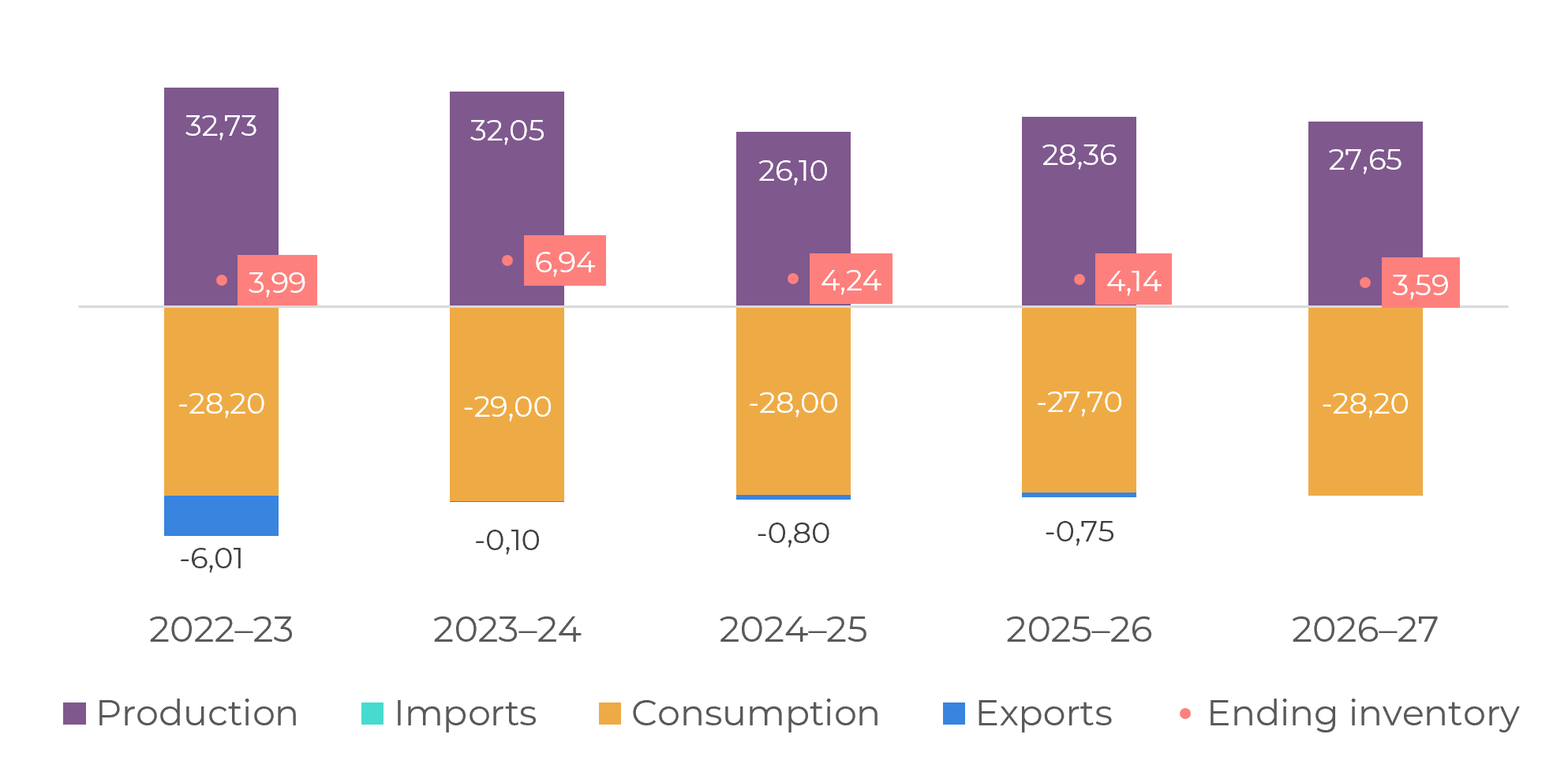

The monsoons have progressed reasonably well after a delayed start. Production is estimated at approximately 27.3 Mt, down from the previous season. The country is not expected to export sugar in 2026/27, and a deterioration in weather conditions due to the El Niño could even lead to a need for imports, which would support prices by directly impacting global supply.

Sugar Balance Sheet – India (Mt, October–September)

Source: ISMA, AISTA, ChiniMandi, NFCSF, Hedgepoint

Thailand

Europe and the United Kingdom

Mexico, Central America, and Eurasia

Brazilian Center-South

In Brazil, the Central-South harvest is performing solidly, with high crushing levels and sugarcane production expected to reach 635 million tons in 26/27 and may even exceed that level. Weather conditions have been favorable so far, with expectations close to the historical average, which should support a robust harvest. The production mix, however, tends to be more alcohol-oriented, reflecting the lower attractiveness of sugar in the face of global oversupply.

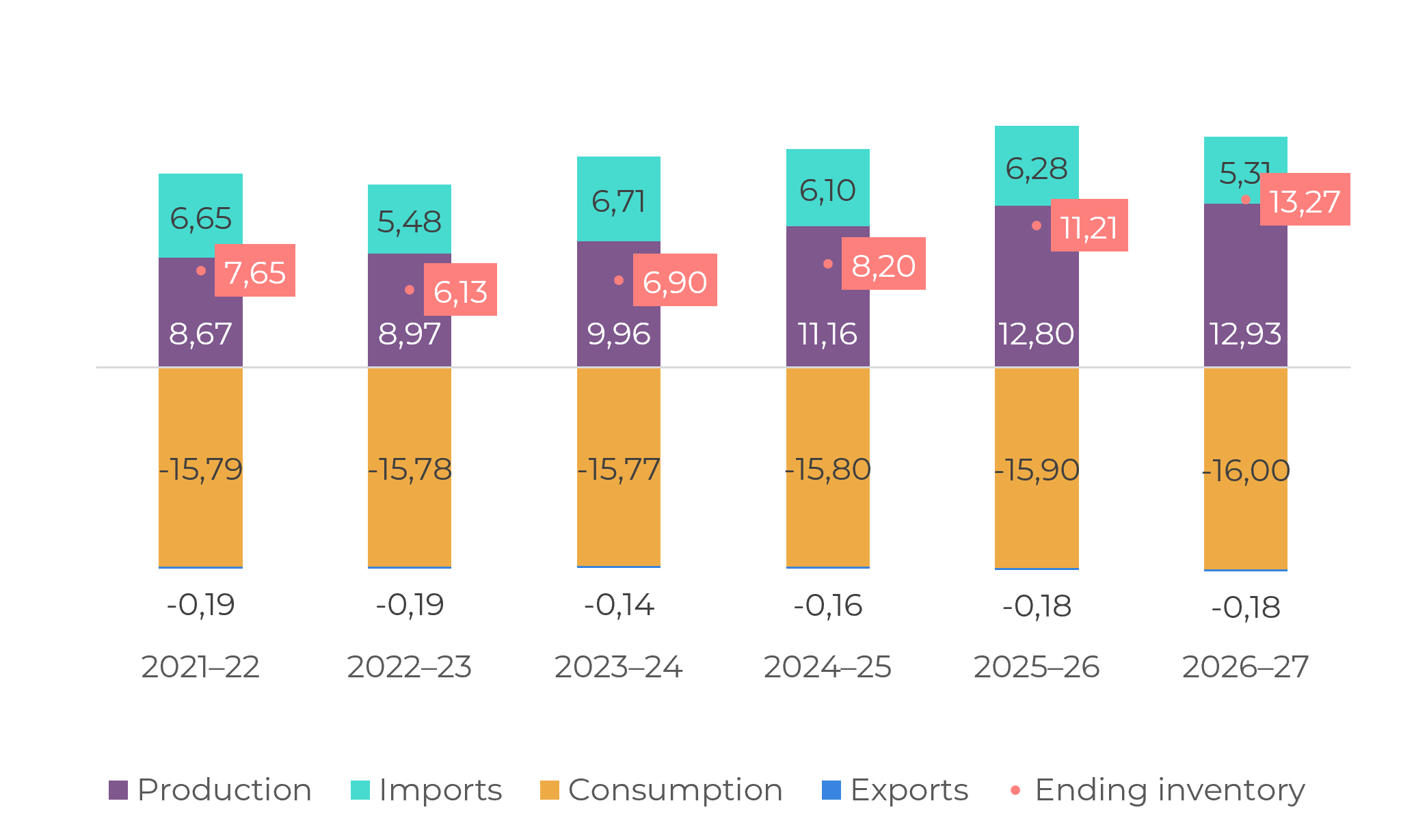

China

Sugar Balance Sheet – China (Mt, October–September)

Source: GSMN, CSA, YNTW, Refinitiv, Greenpool, Hedgepoint. Note: Inventories also include volumes held in bonded warehouses.

Brazil

Even with rains delaying the crushing season, the forecast remains virtually unchanged: 635 Mt of sugarcane, an ATR slightly higher than expected, and a sugar-to-ethanol ratio of approximately 47.3%. There is potential for an increase in the sugar mix if prices continue to favor sugar over ethanol. Not only that, but the prospect of a tightening in trade flows in 2027 suggests that the next harvest in Brazil’s Center-South region may be predominantly sugar-oriented. In terms of El Niño, the climate event does not have a strong correlation with sugarcane-producing regions. However, due to its high intensity, we may see heavier rainfall in southern São Paulo and Mato Grosso do Sul during the next months, which could delay the harvest but benefit sugarcane toward the end of the season. El Niño years generally tend to boost yields in the region.

Crop Summary

Source: UNICA, Hedgepoint

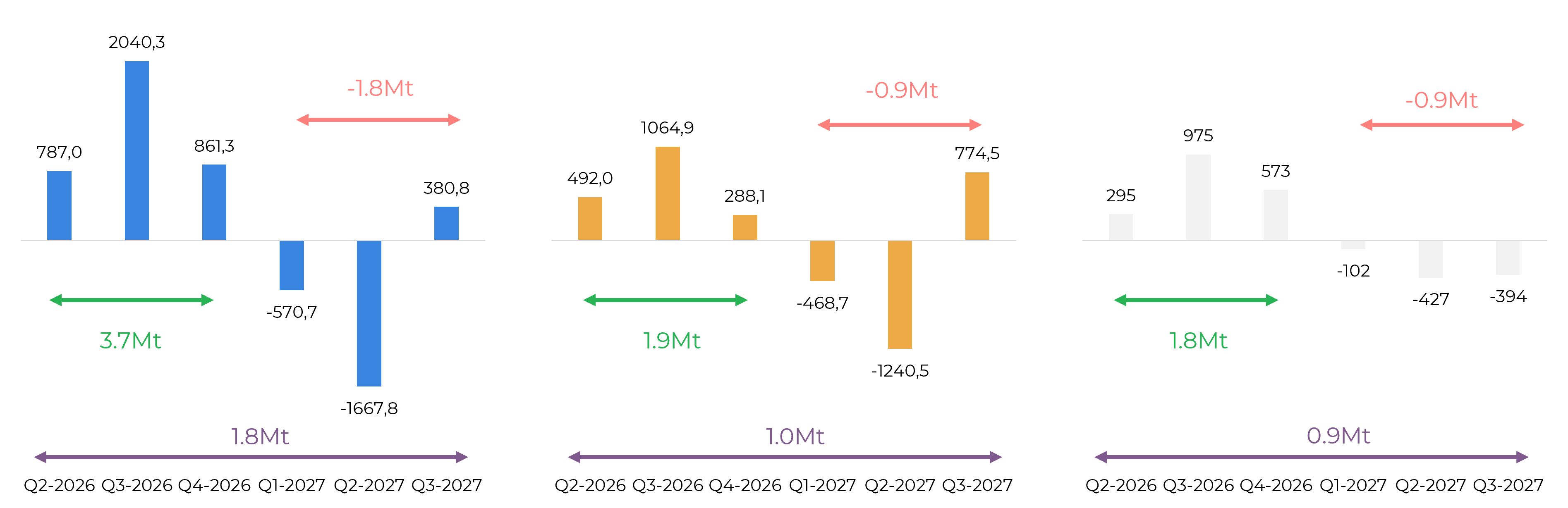

Global Trade Flow

The reduction in exportable supply from the Northern Hemisphere has diminished the expected global market surplus starting in the fourth quarter of 2026. Brazil continues to act as the main supplier balancing the market and is expected to play an even more significant role in 2027/28. Changes in the product mix in the Center-South region may partially mitigate this scenario. Conversely, significant declines that could lead India to import will intensify the global tightness. These trends should be monitored closely.

Total trade flows (left), raw sugar (middle), and white sugar (right) | ‘000t tq

Source: Green Pool, Hedgepoint

Summary

Weekly Report — Sugar

laleska.moda@hedgepointglobal.com

Disclaimer

This document has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without intending to create obligations or commitments to third parties. It is not intended to promote or solicit an offer for the sale or purchase of any securities, commodities interests, or investment products.