Higher Indian production meets a bearish global sugar environment

- Global sugar prices stayed bearish in 2025, falling 22% to 15 c/lb, mainly due to strong supply from Brazil and other Northern Hemisphere producers; India’s bullish influence was limited.

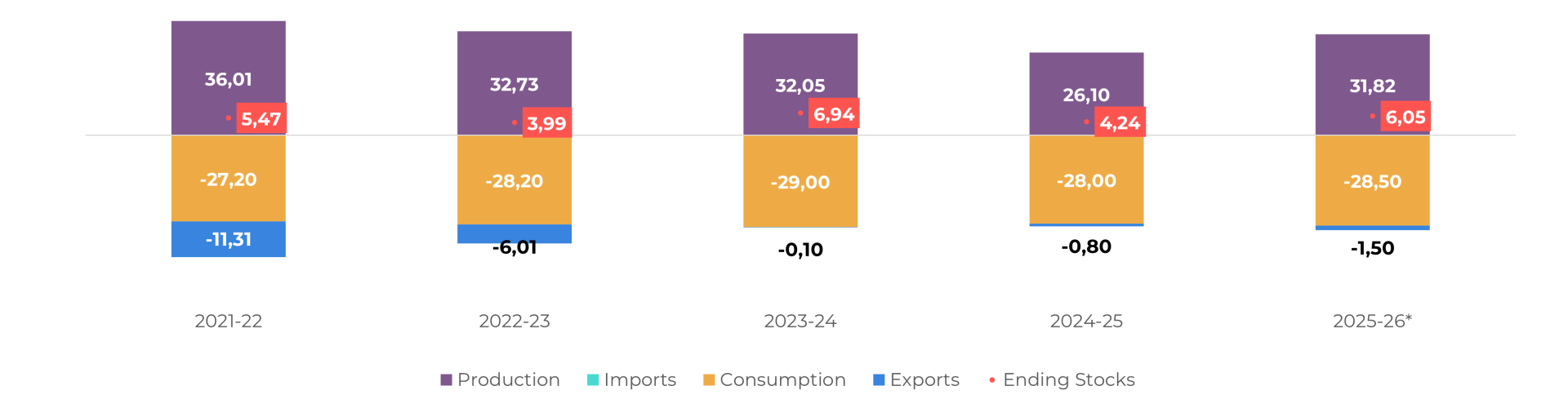

- India’s 2024/25 output underperformed, with net sugar production at 26.1 Mt and 800 kt exported; a remaining 200 kt is likely to roll into 2025/26.

- For 2025/26, India’s production is outperforming expectations, with output up 20% year-on-year, lifting our net production estimate to 31.8 Mt.

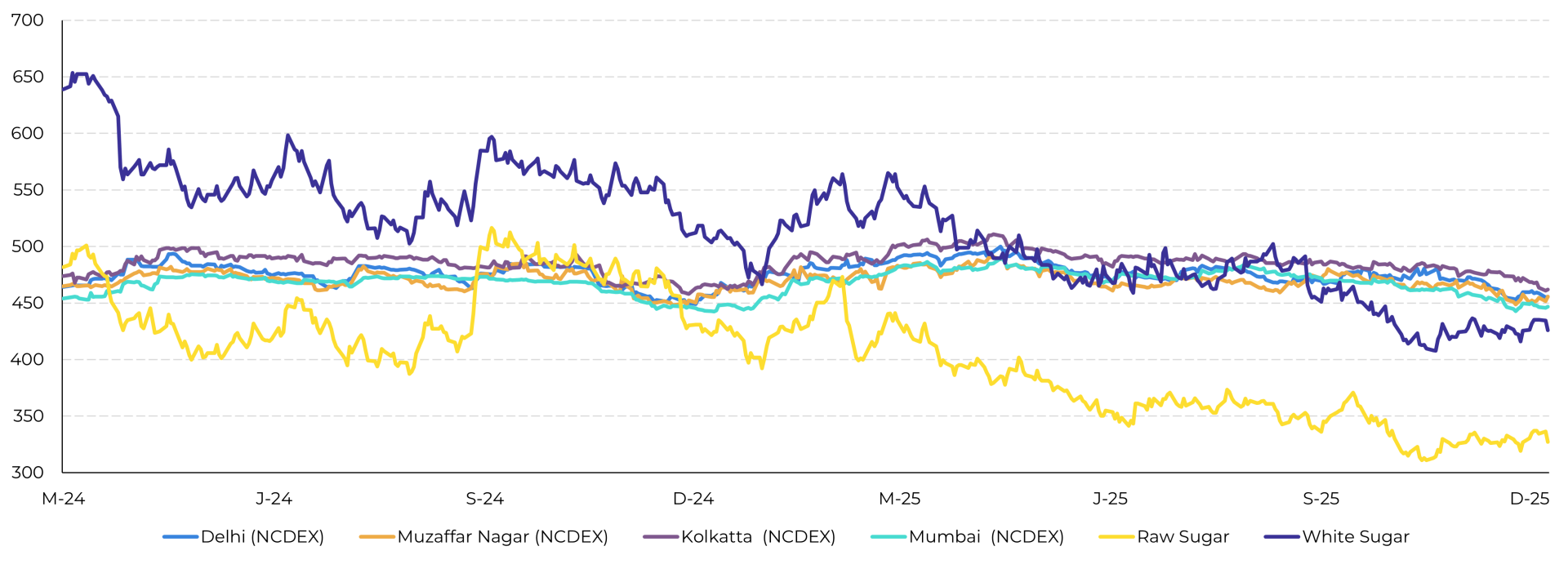

- Export prospects remain constrained as domestic vs. international price dynamics close arbitrage; export parity sits near 18.5 c/lb (raws) and USD 445/t (whites), while potential Minimum Selling Price (MSP) hikes may further limit export viability.

- Brazil’s robust intercrop and stable cane forecasts (610 Mt) dampen any bullish impact from India, reinforcing the bearish global context.

Higher Indian production meets a bearish global sugar environment

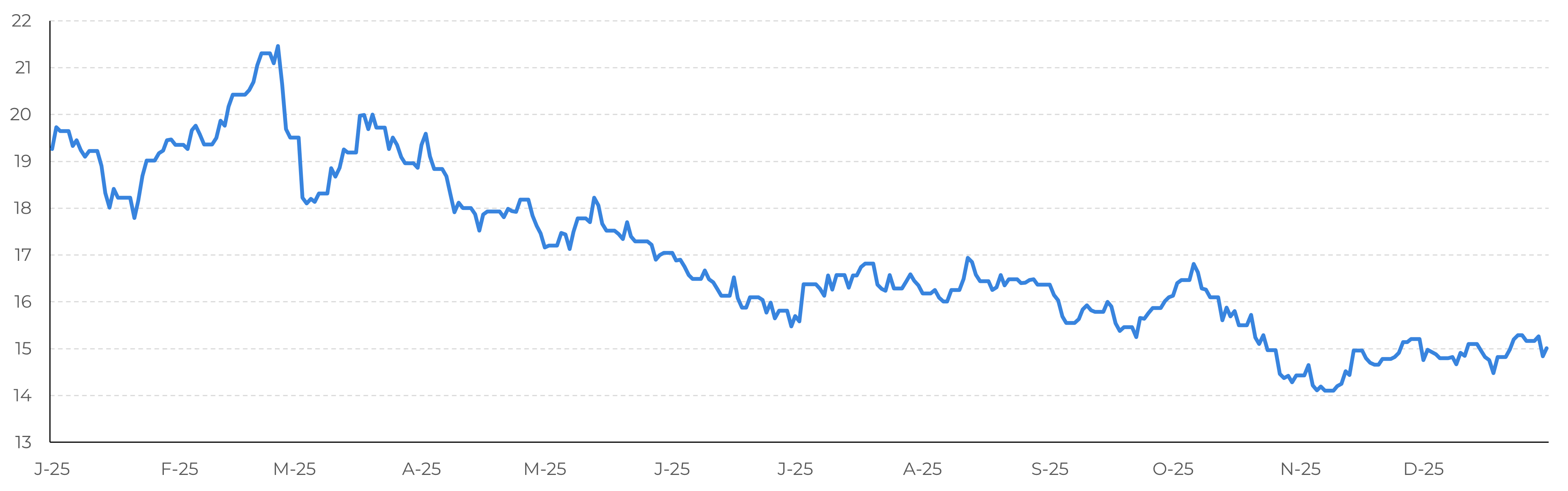

Sugar prices remained on a bearish trajectory throughout 2025, driven primarily by increased availability in Brazil and several Northern Hemisphere producers, such as the European Union. With cane estimates consistently revised upward, Brazil’s strong output exerted downward pressure on prices, which ended the year at 15 c/lb; representing a 22% annual decline. Although there are still key uncertainties for Brazil in 2026, this report focuses on India’s role in the market. The latter provided some bullish support during 2025, but its overall impact on global prices was limited.

Raw sugar prices through 2025 (c/lb)

Source: LSEG

Namely, in the 2024/25 season, India’s sugar production came in below expectations at roughly 29.6 Mt gross. After diverting 3.4 Mt to ethanol, net sugar output reached 26.1 Mt. On the export front, the country shipped 800 kt, with the remaining 200 kt quota likely to be carried into 2025/26.

For the 2025/26 season, early results align with our forecasts; pointing to a significantly more positive outlook that reinforces the global bearish trend. Production has been advancing at an excellent pace: from October 2025 to January 15, 2026, India produced nearly 16 Mt, a 20% increase over the same period last year. Cane crush also rose notably, totaling 176.4 Mt compared with 148.4 Mt in the previous season.

Average sugar recovery improved to 9%, up from 8.8% in 2024/25. As a result, we have raised our net production estimate slightly to 31.8 Mt, while ethanol diversion expectations have been trimmed to 3.7 Mt.

Average sugar recovery improved to 9%, up from 8.8% in 2024/25. As a result, we have raised our net production estimate slightly to 31.8 Mt, while ethanol diversion expectations have been trimmed to 3.7 Mt.

India Supply and Demand (Oct - Sep | Mt)

Source: Hedgepoint

India’s domestic prices vs international (USD/t)

Source: Bloomberg, Hedgepoint

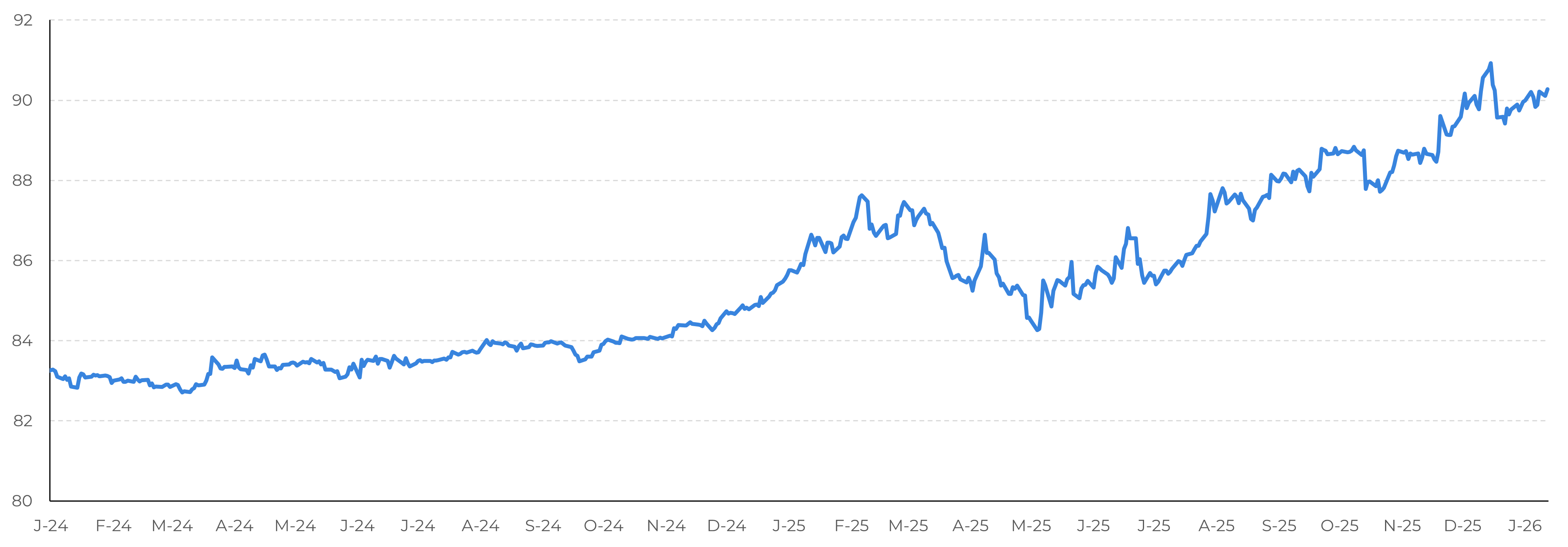

INR depreciation against the dolar

Source: LSEG

Summary

Sugar prices stayed under pressure in 2025 due to abundant supply from Brazil and other major producers, while India, despite weaker 2024/25 output, offered only limited bullish support. In 2025/26, India’s production has accelerated sharply, reinforcing the global bearish trend, though high domestic prices and a likely increase in the MSP restrict export viability. Meanwhile, Brazil’s stronger than expected intercrop and steady cane outlook have further capped any short-term upside.

Weekly Report — Sugar

Reviewed by Thais Italiani

thais.italiani@hedgepointglobal.com

Disclaimer

This document has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without intending to create obligations or commitments to third parties. It is not intended to promote or solicit an offer for the sale or purchase of any securities, commodities interests, or investment products.

To access this report, you need to be a subscriber.

Contact us

Check our general terms and important notices.

We have updated our Terms & Conditions to reflect improvements to our platform, data handling practices, and the overall experience we provide to our clients.