Weather improvements and price corrections

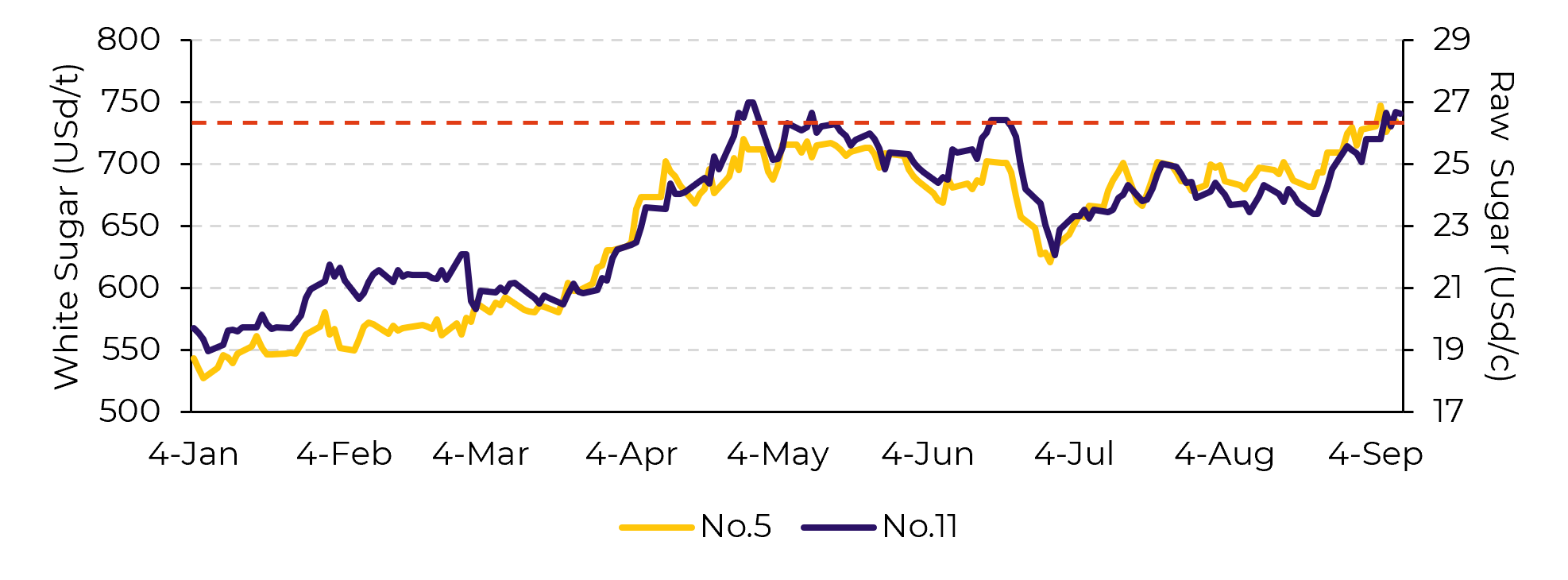

Image 1: Prices are supported by availability restraints

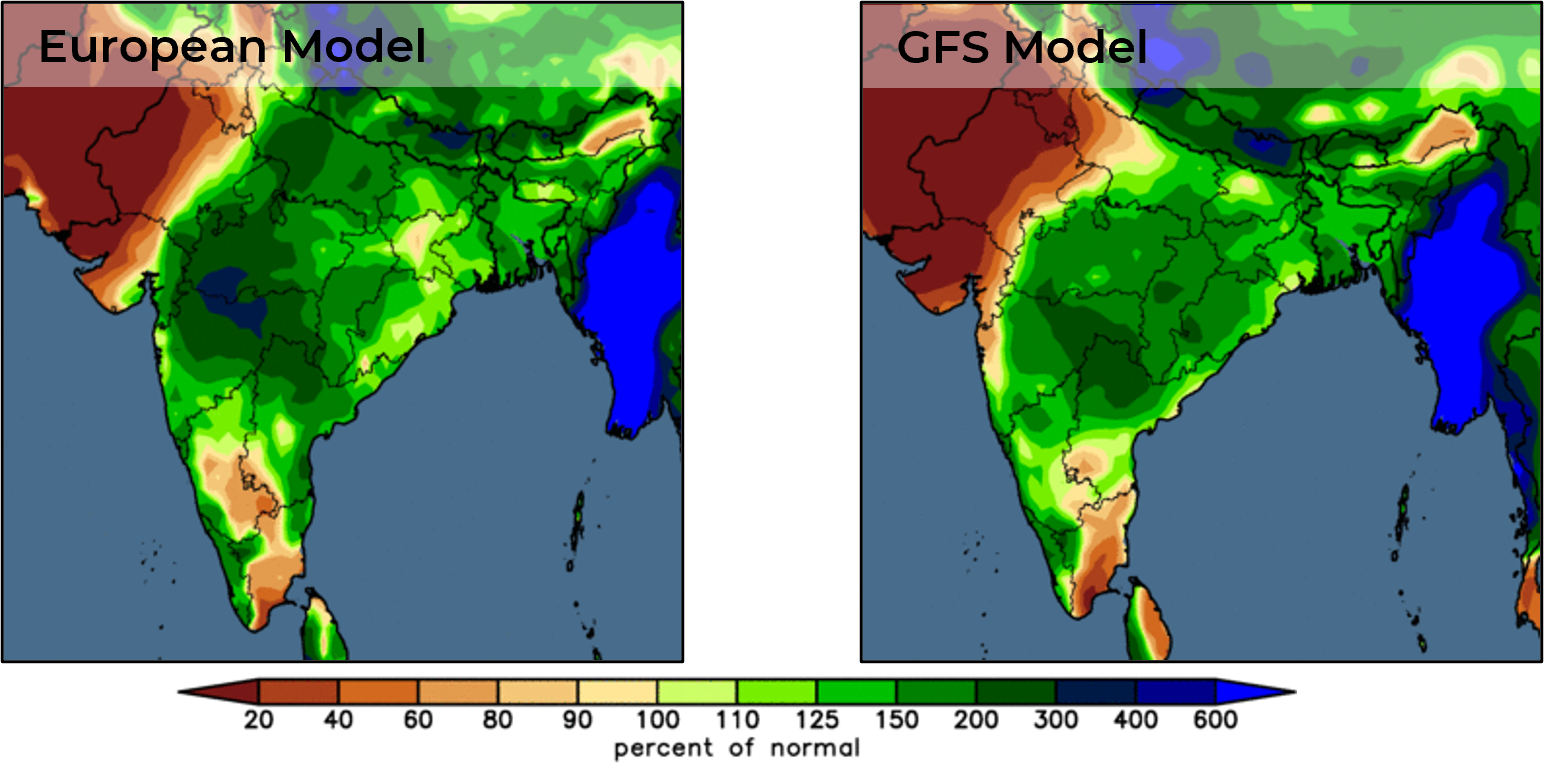

Image 2: Precipitation anomaly forecast India for 14-days starting September 8 (%)

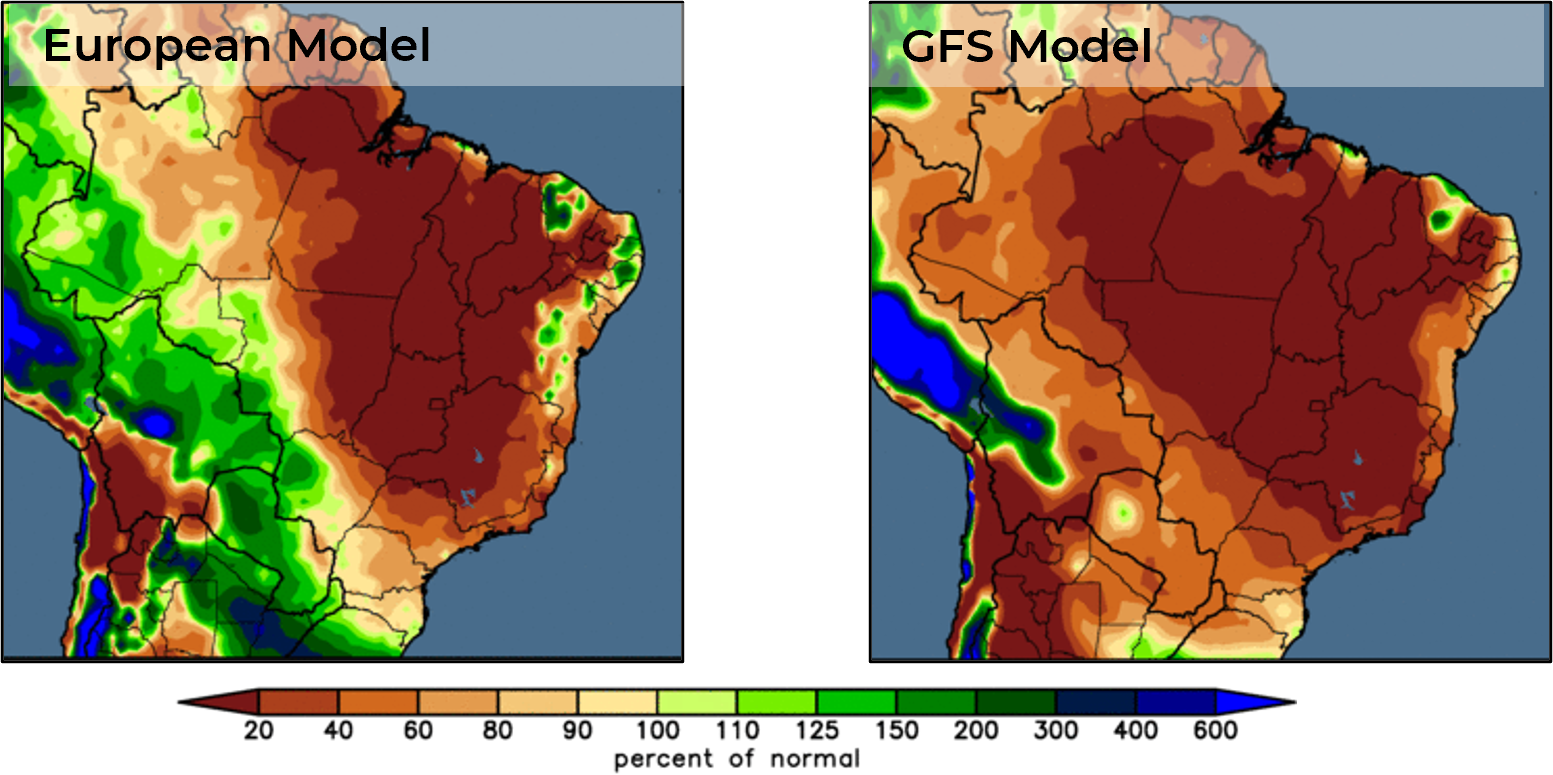

Image 3: Precipitation anomaly forecast Brazil for 14-days starting September 8 (%)

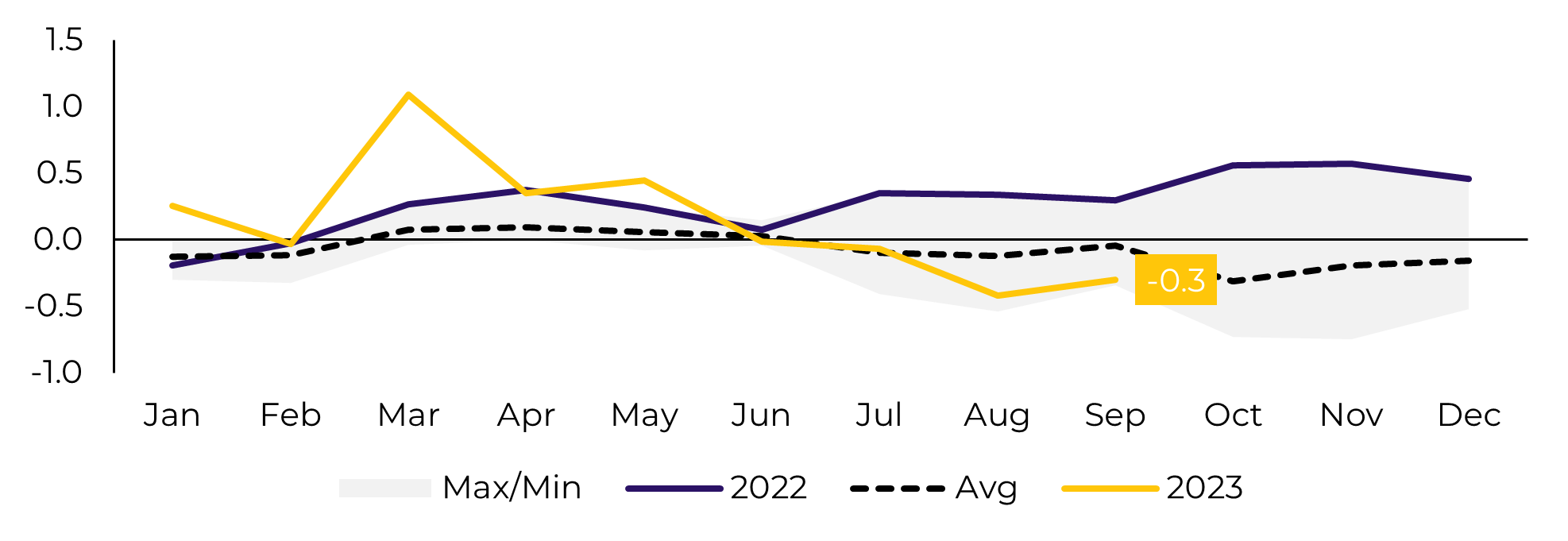

Image 4: Raw sugar cash premium at Santos (USc/lb)

In Summary

Weekly Report — Sugar

Disclaimer

To access this report, you need to be a subscriber.