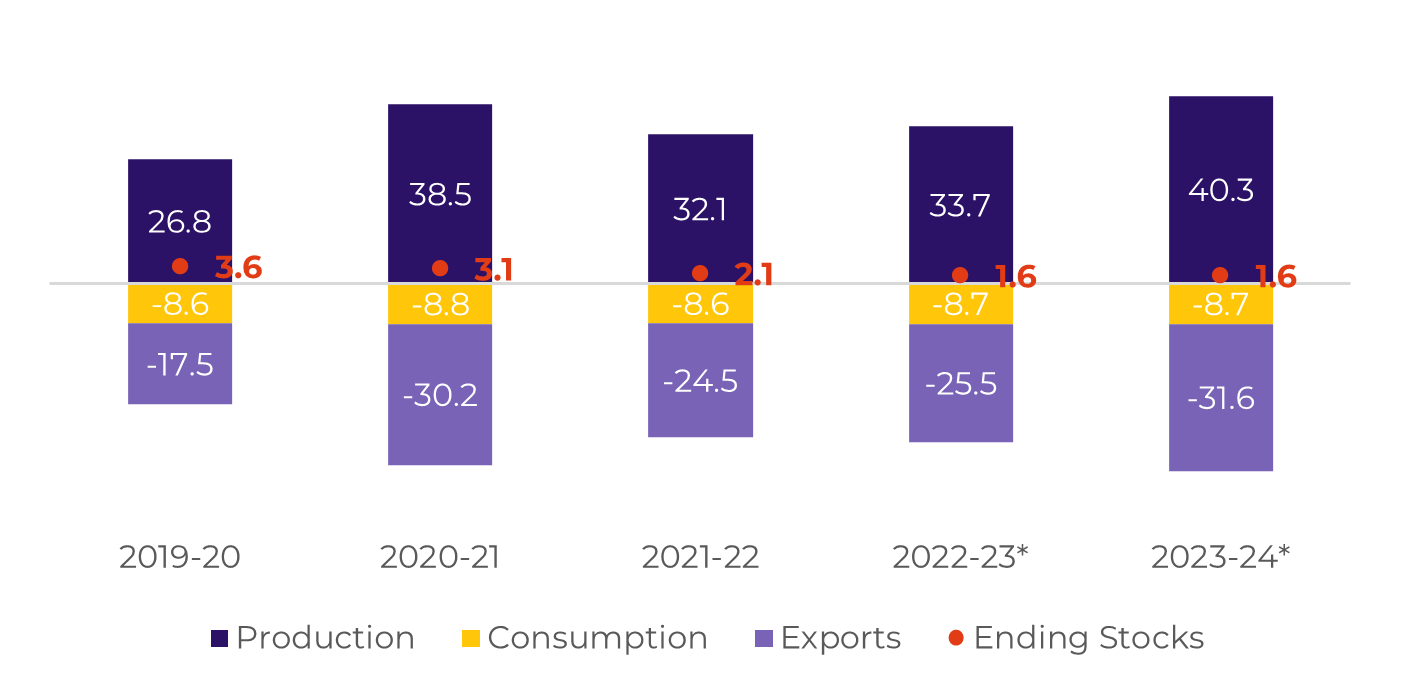

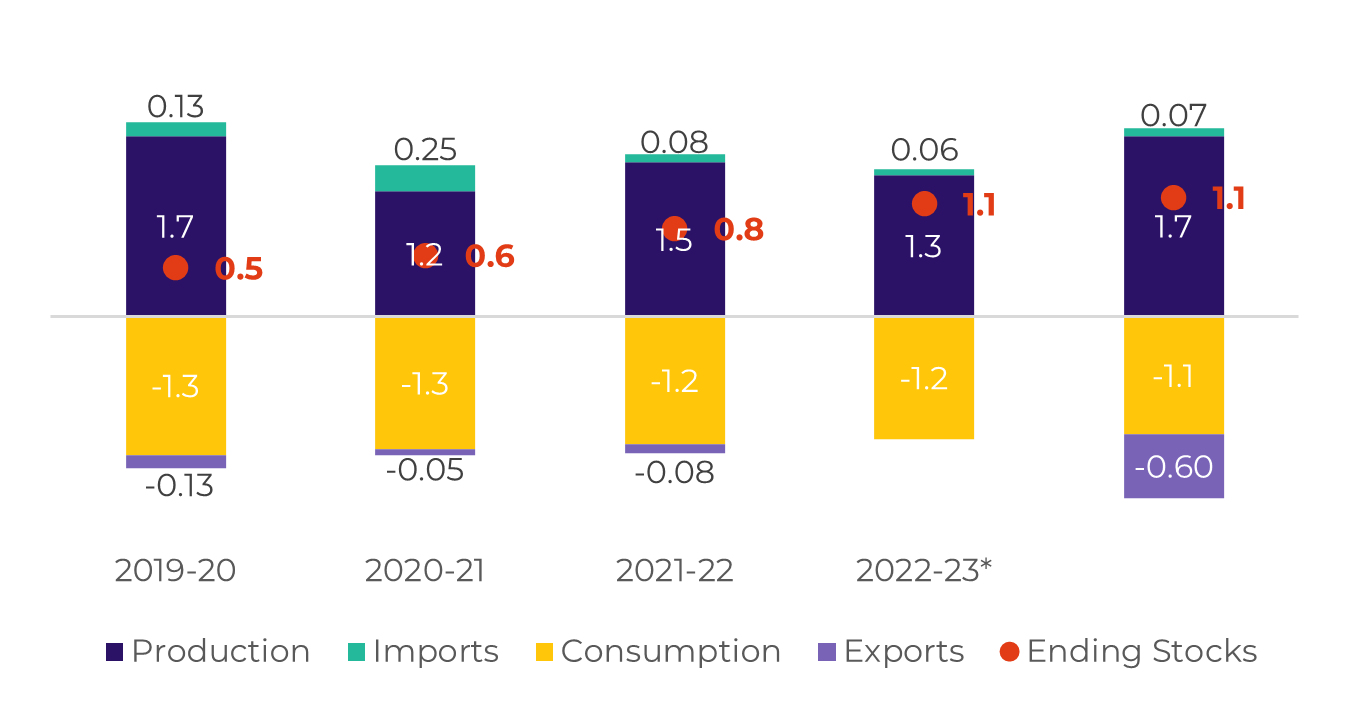

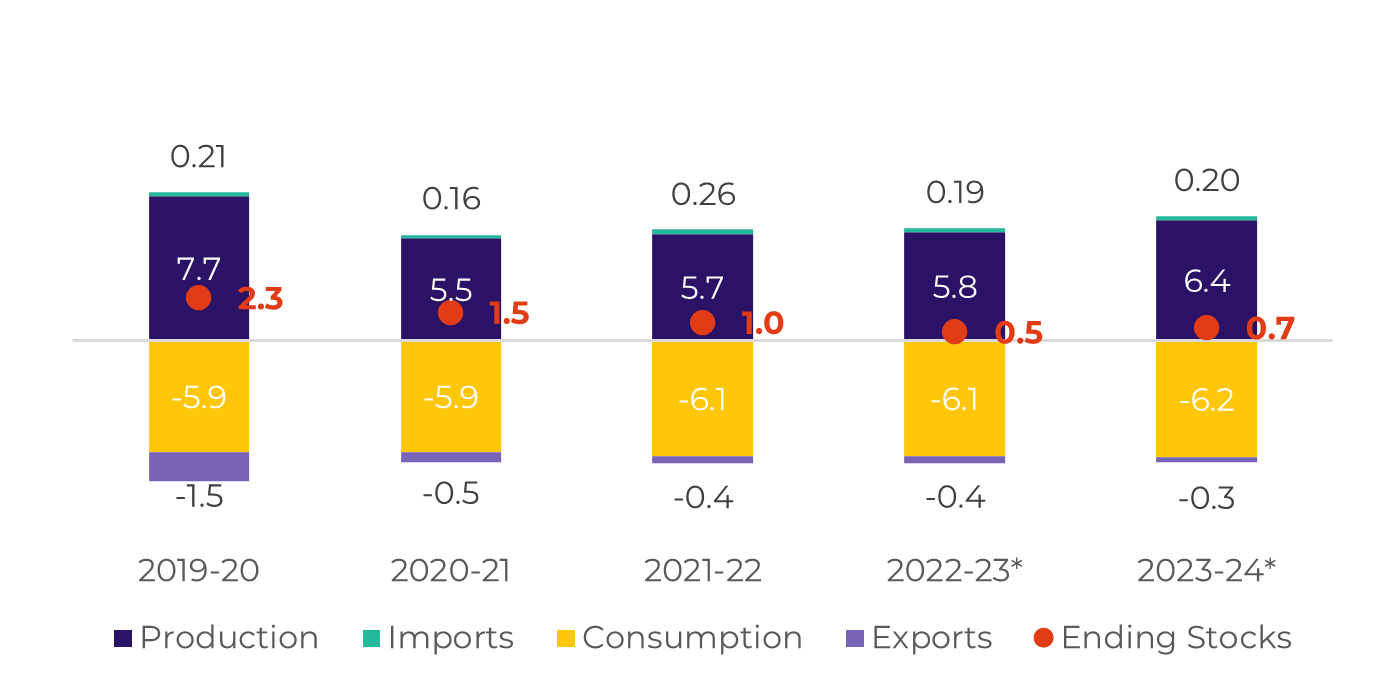

Source: Ikar, Sugar.ru, Greenpool, hEDGEpoint

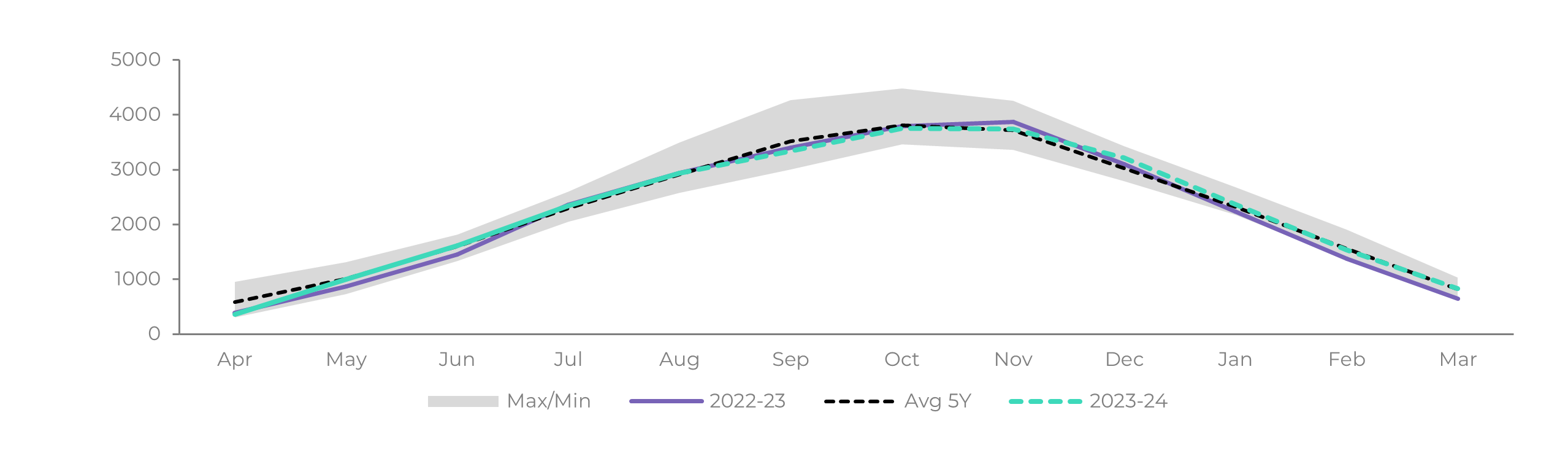

There are risks associated with sugar beet processing, including weather-related challenges and issues with fuels and lubricants that add a negative pressure to the 6.4Mt estimate.

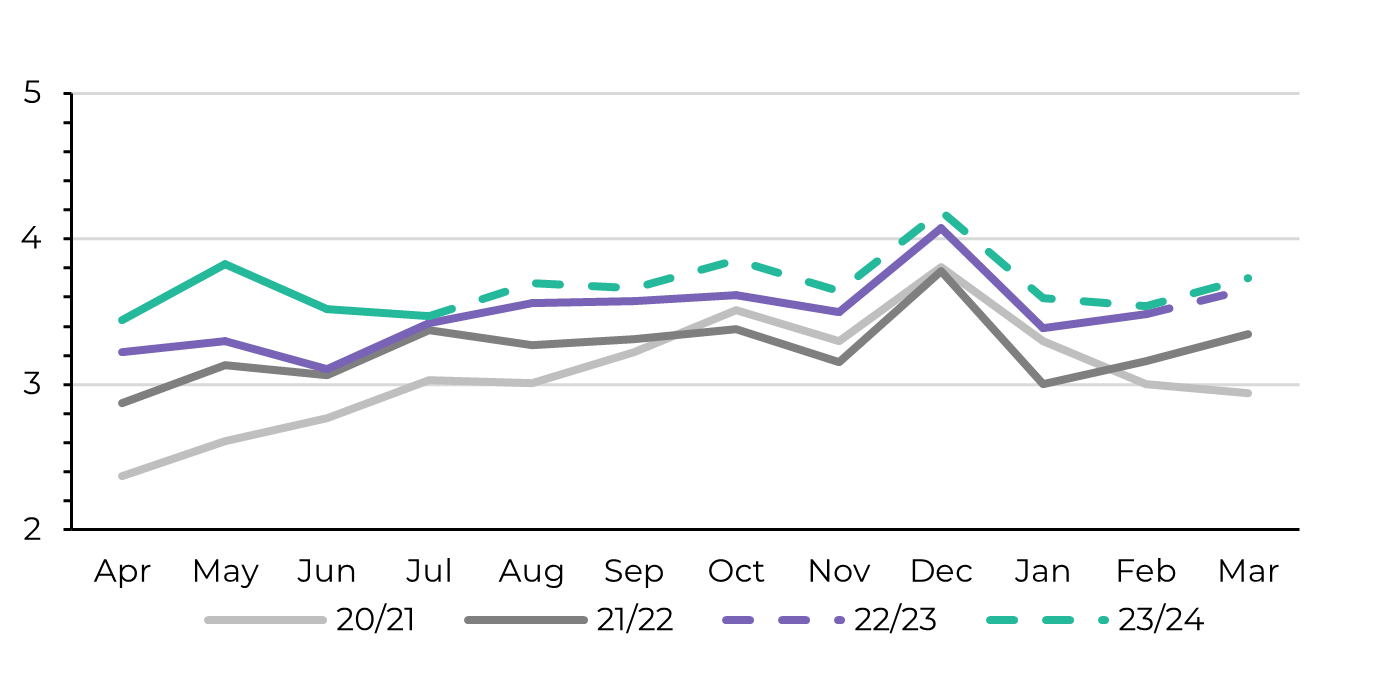

The latest data from Soyuzrossakhar, disclosed by sugar.ru, reveals that the current sugar yield as of September 11th is at 13%, which is notably low. To provide context, on September 12th 2022, it was 14.2%, and in 2021, it stood at 13.5%. Estimating the current sugar beet crop at 45.7 million metric tons (accounting for losses), sugar.ru bets on a range between 6.2 and 6.4Mt.