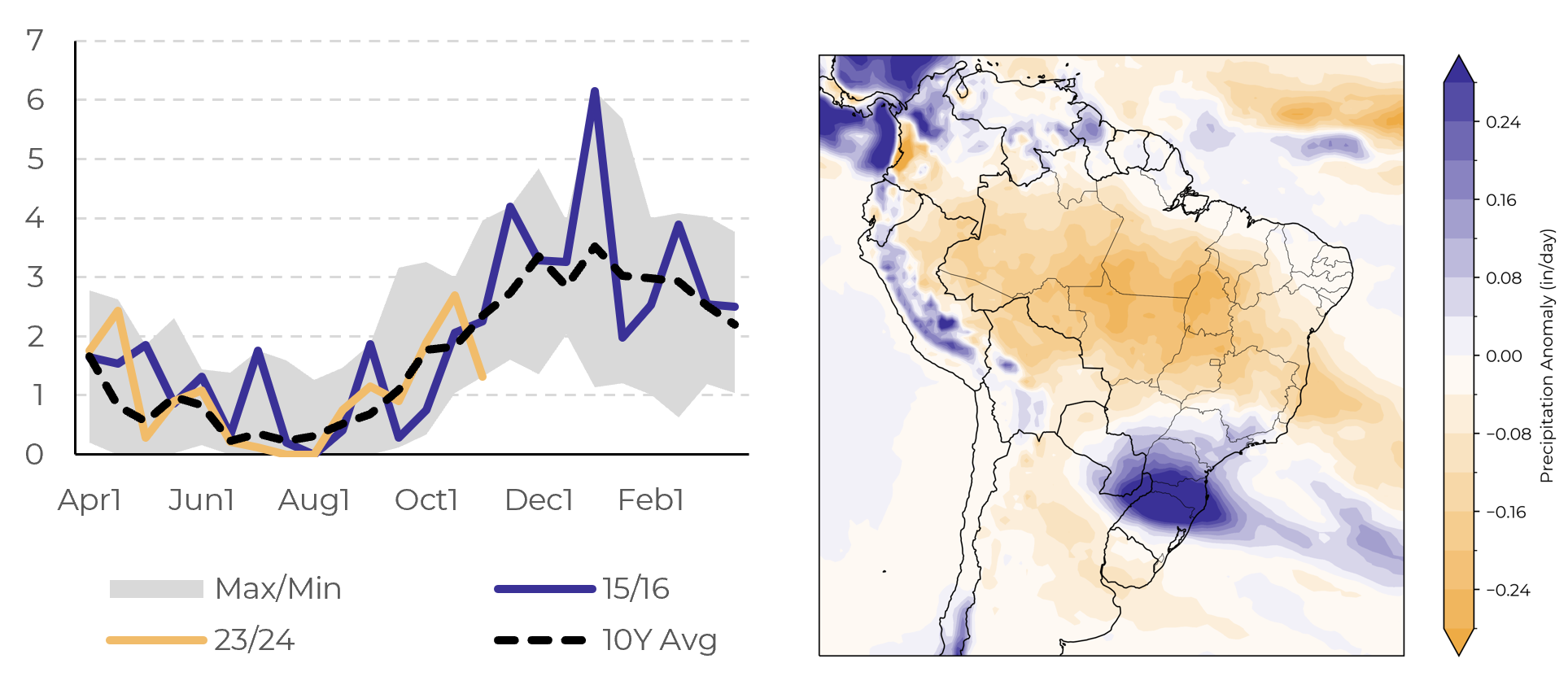

Dry weather, shipping improvements

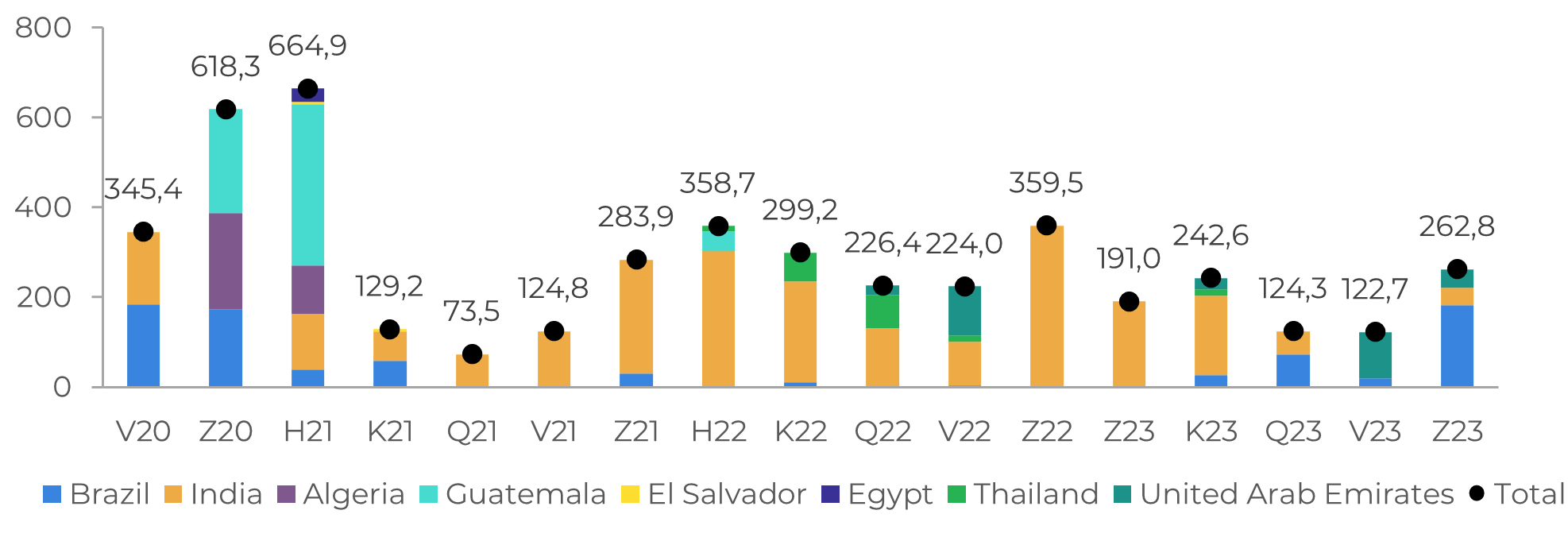

Image 1: White sugar delivery (‘000t)

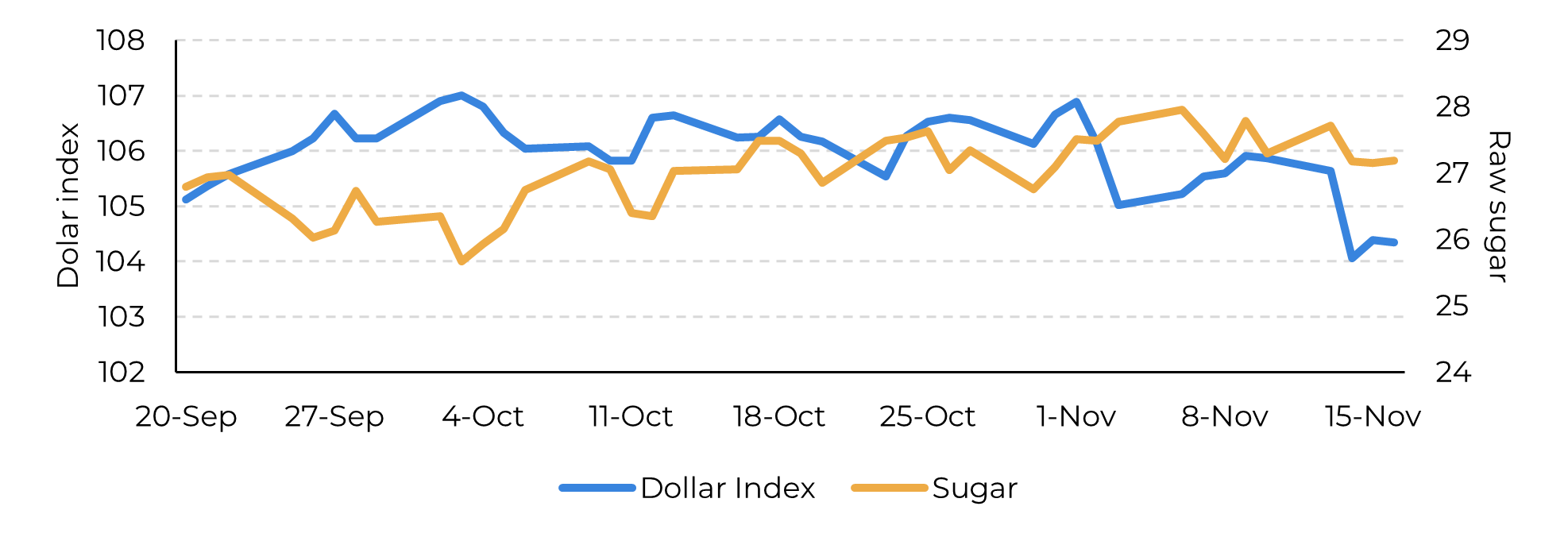

Image 2: Sugar failed to register gains amid macro sentiment shift

Image 3: Lost days estimate per fortnight (No. days)/left and lost days estimate per fortnight (No. days)/right

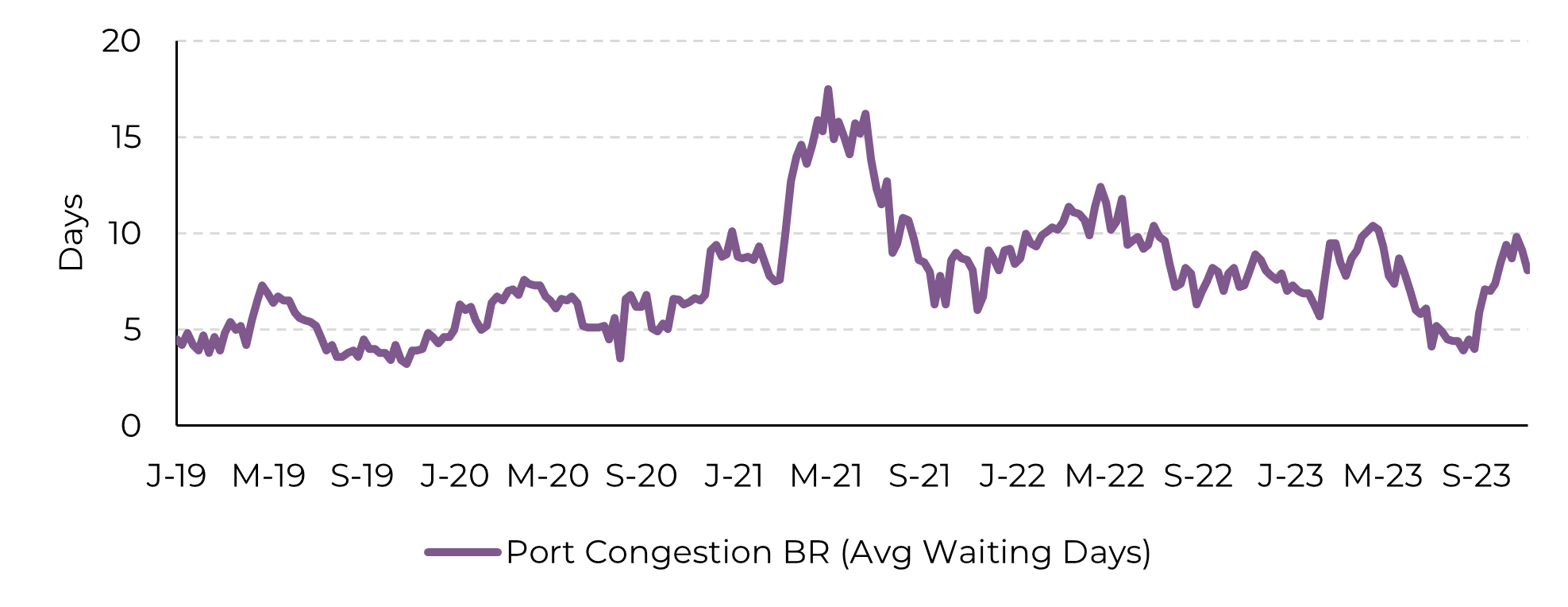

Image 4: Port congestion is starting to correct

In Summary

Weekly Report — Sugar

Disclaimer

To access this report, you need to be a subscriber.