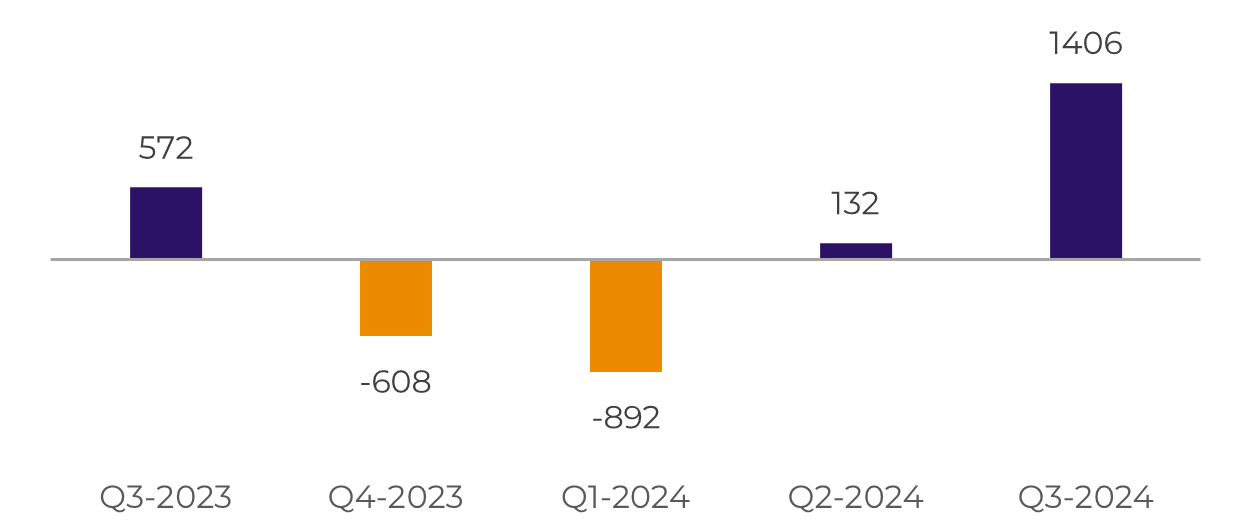

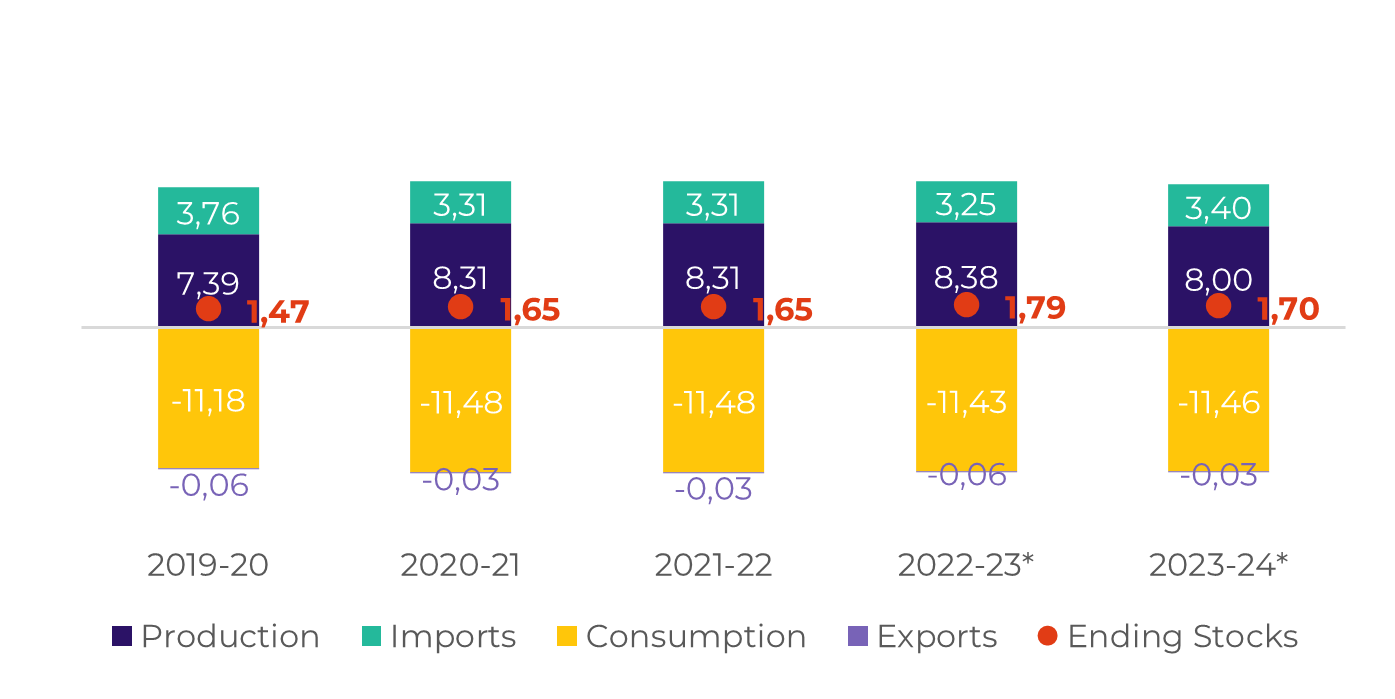

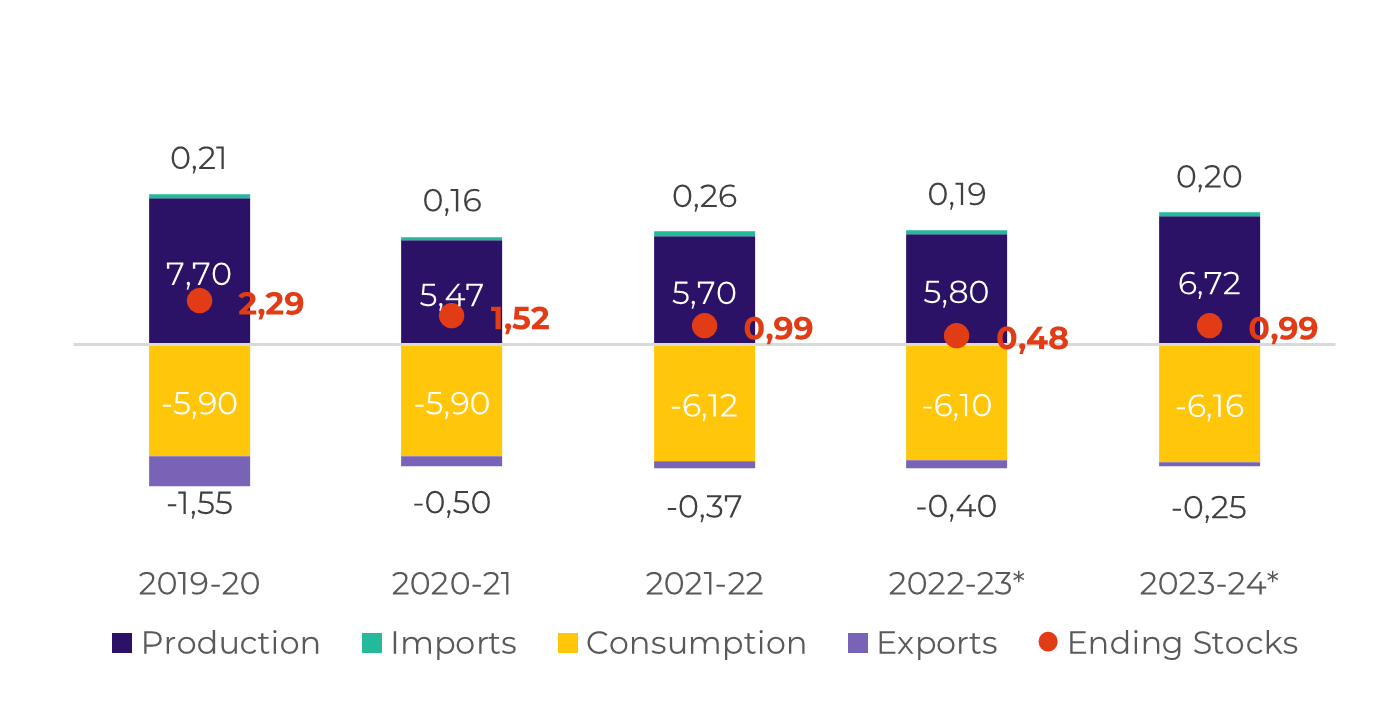

Source: Unica, MAPA, SECEX, hEDGEpoint

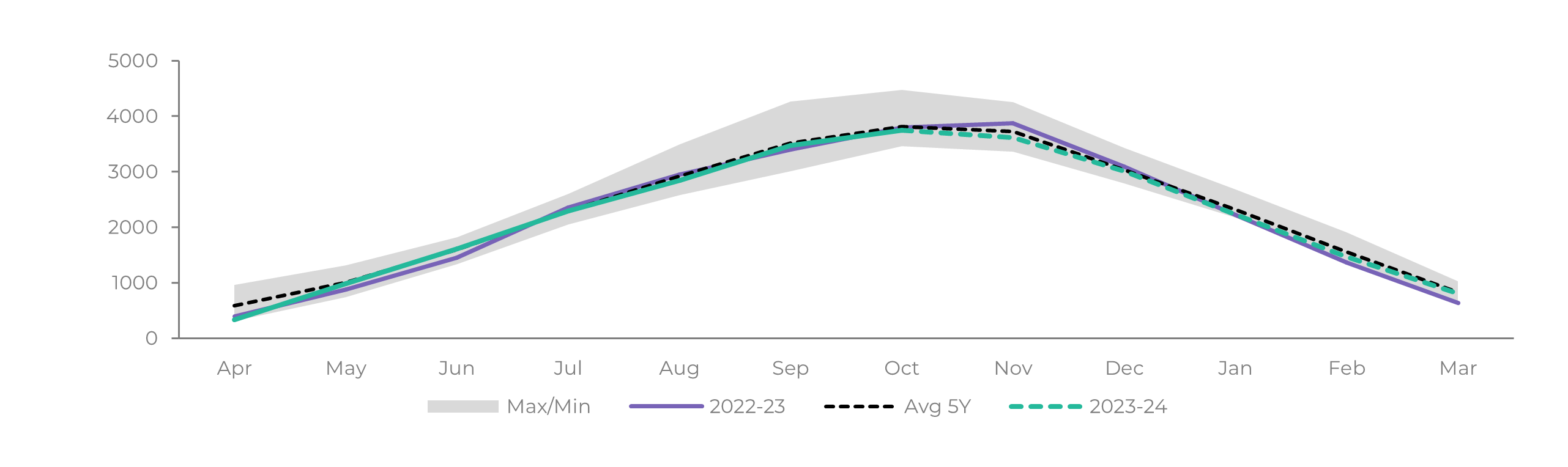

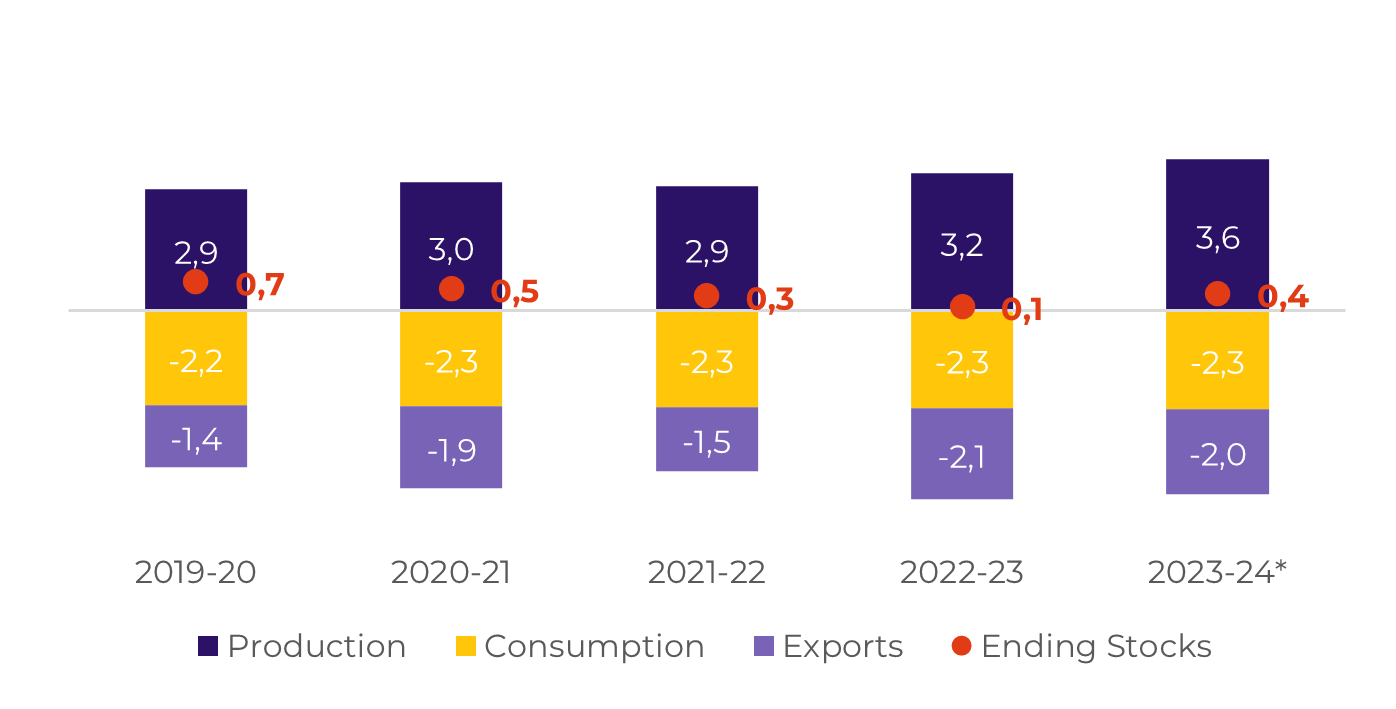

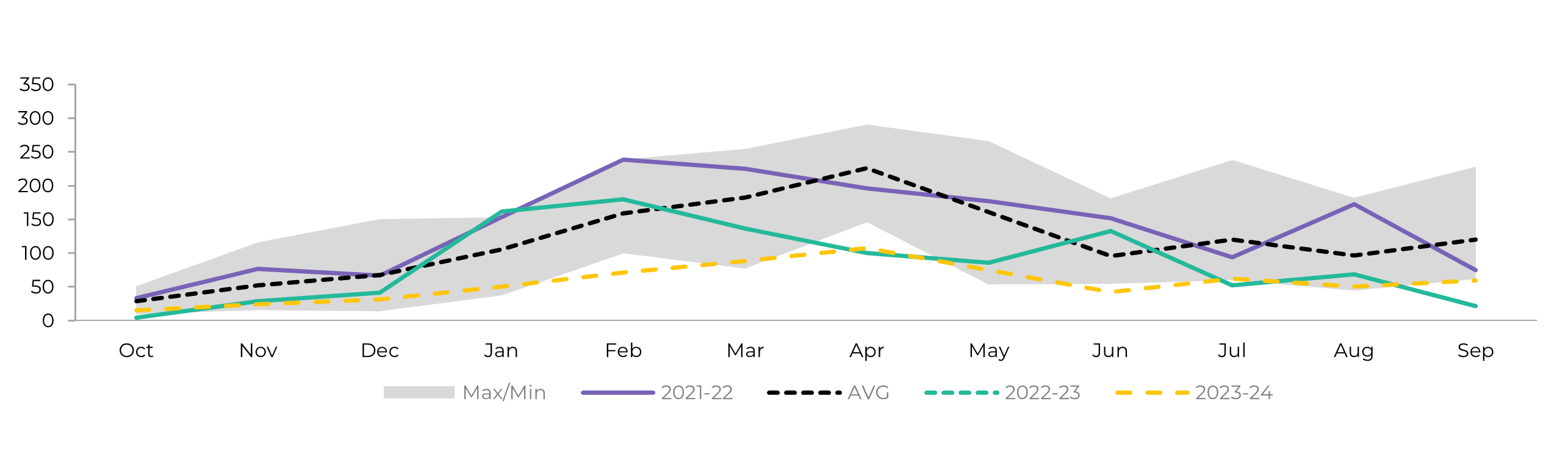

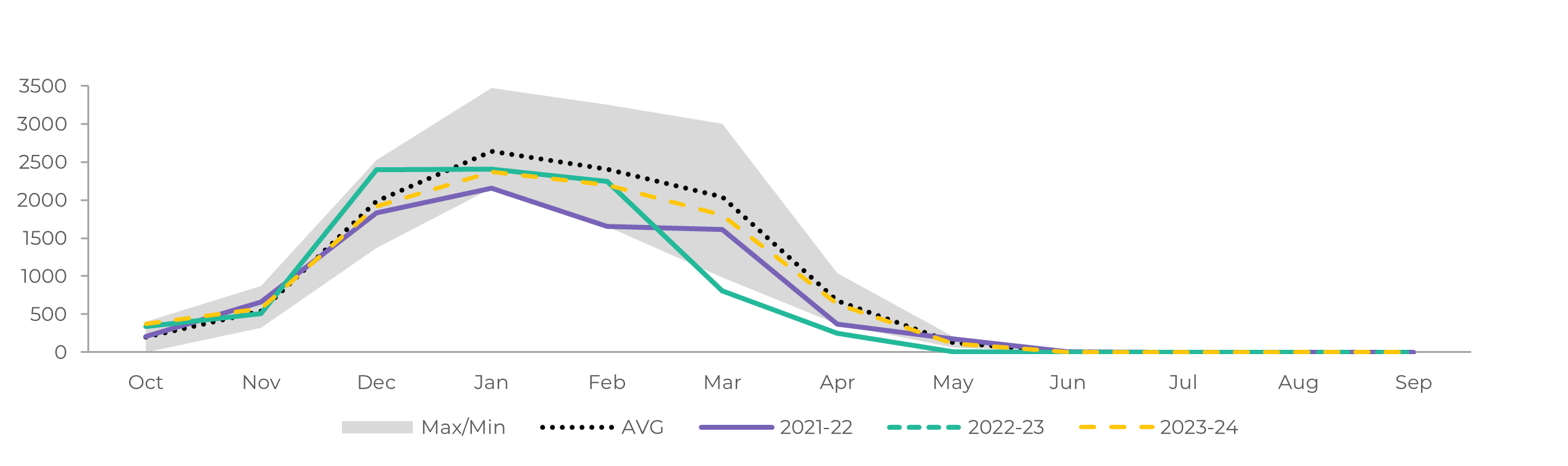

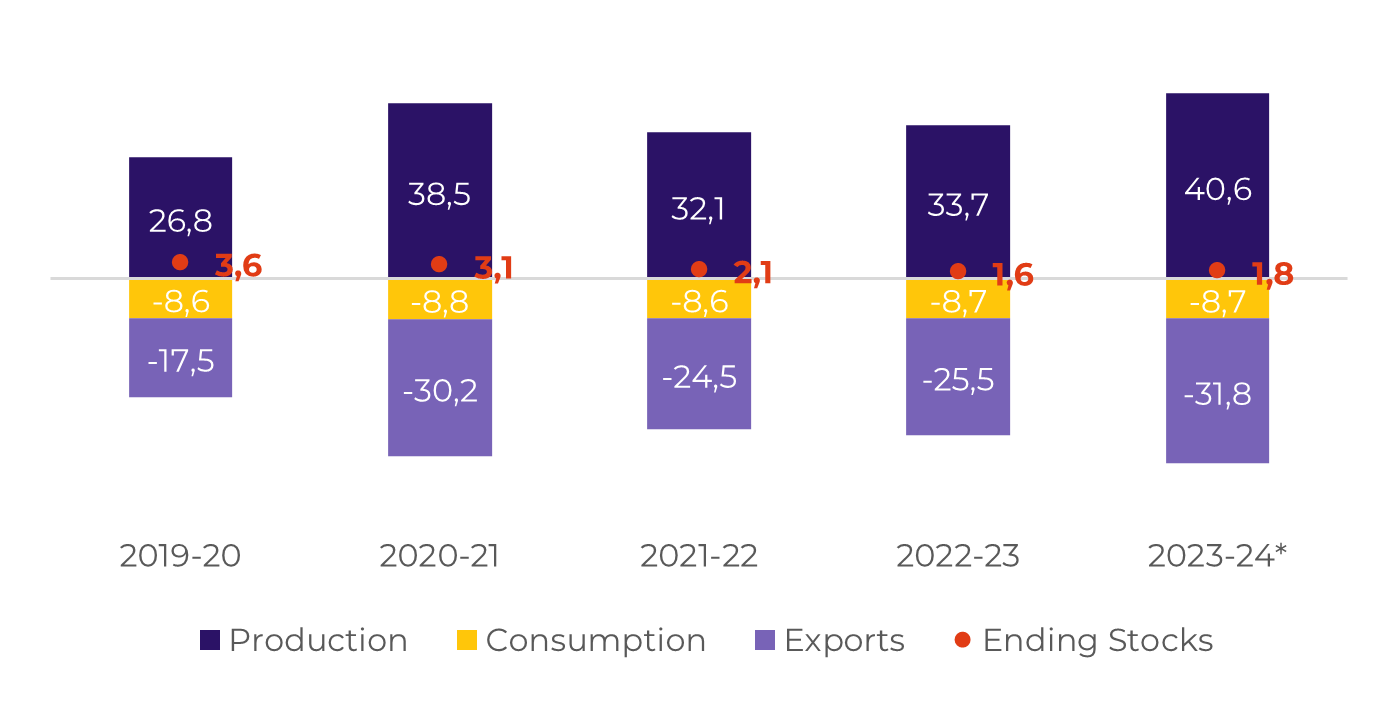

Cane yields and area expansion during 23/24 are the main reasons behind the region’s excellent results.

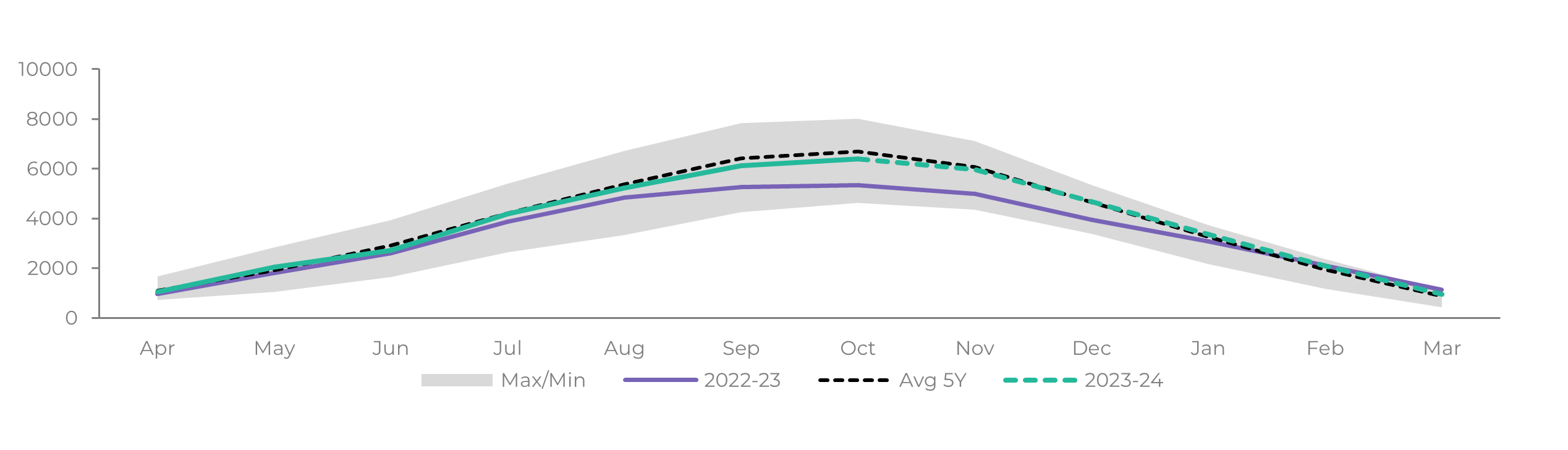

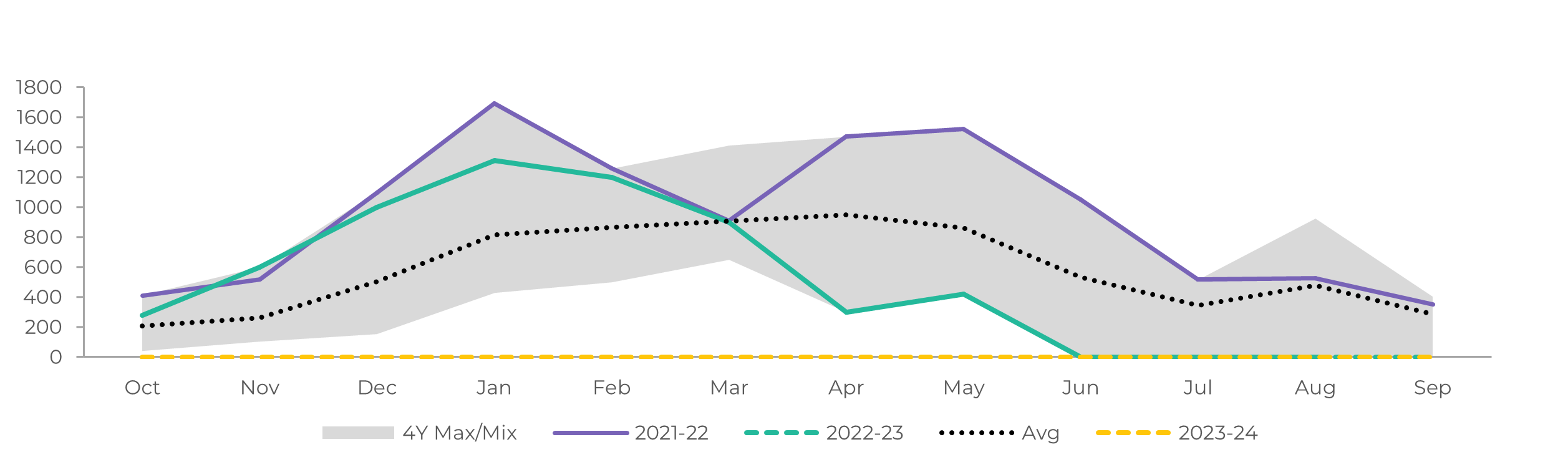

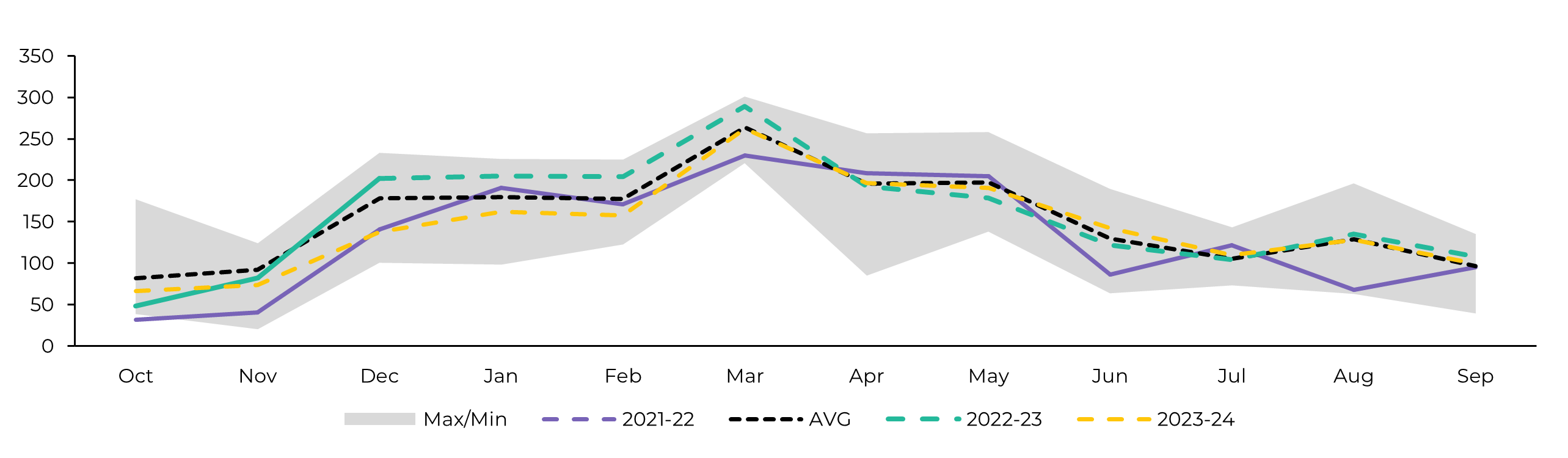

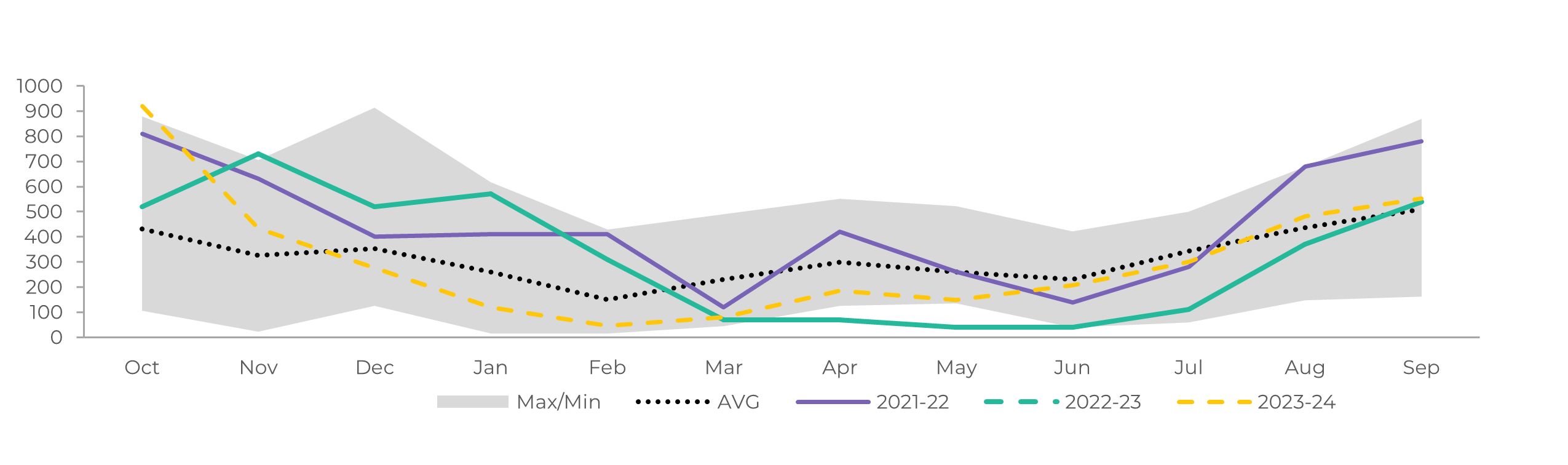

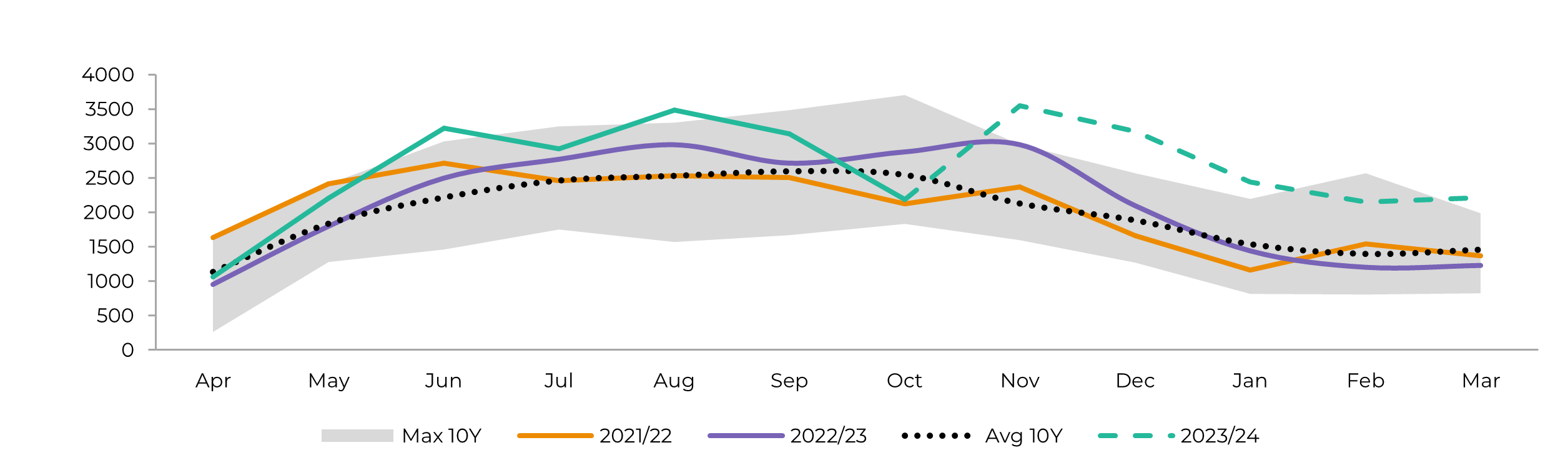

Recent price volatility is tight to the country’s ability to ship the sweetener. Port congestion due to a rainier-than-average October has induced recent gains, but dryness is coming.

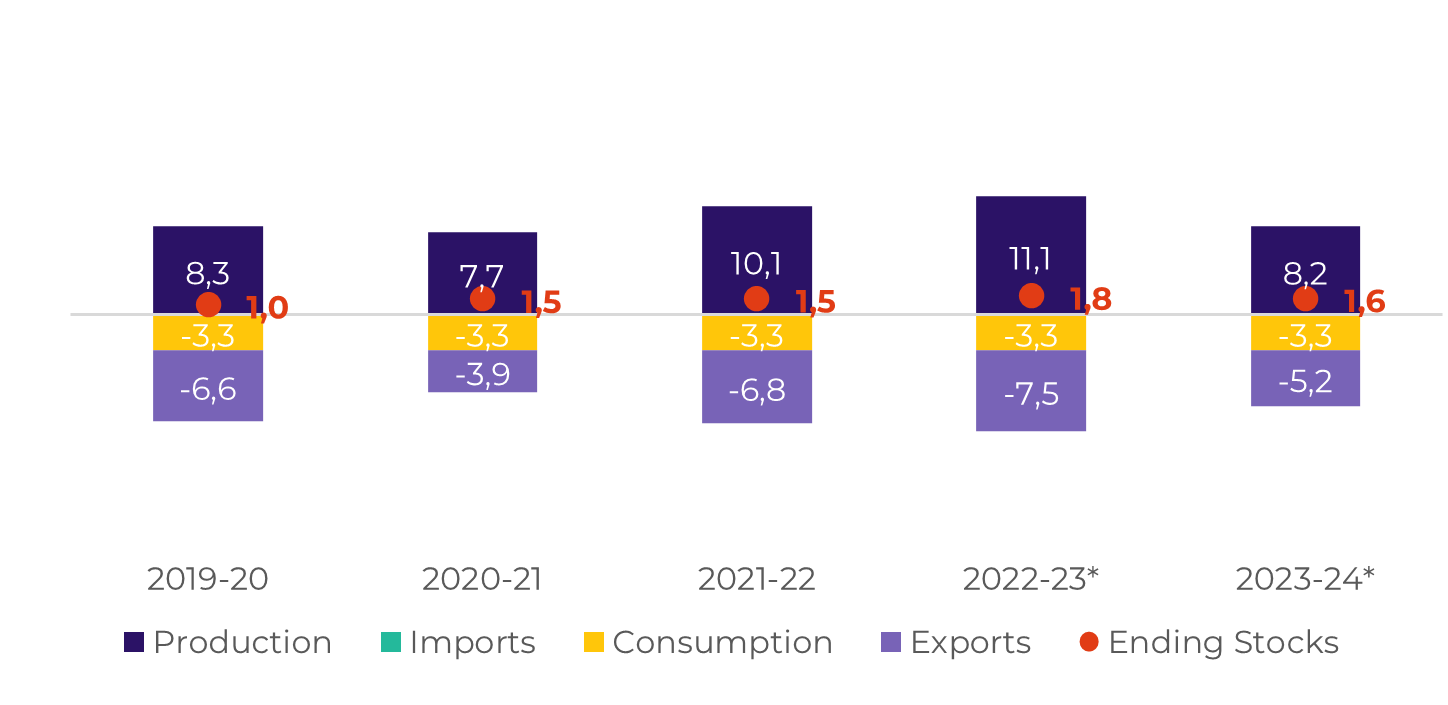

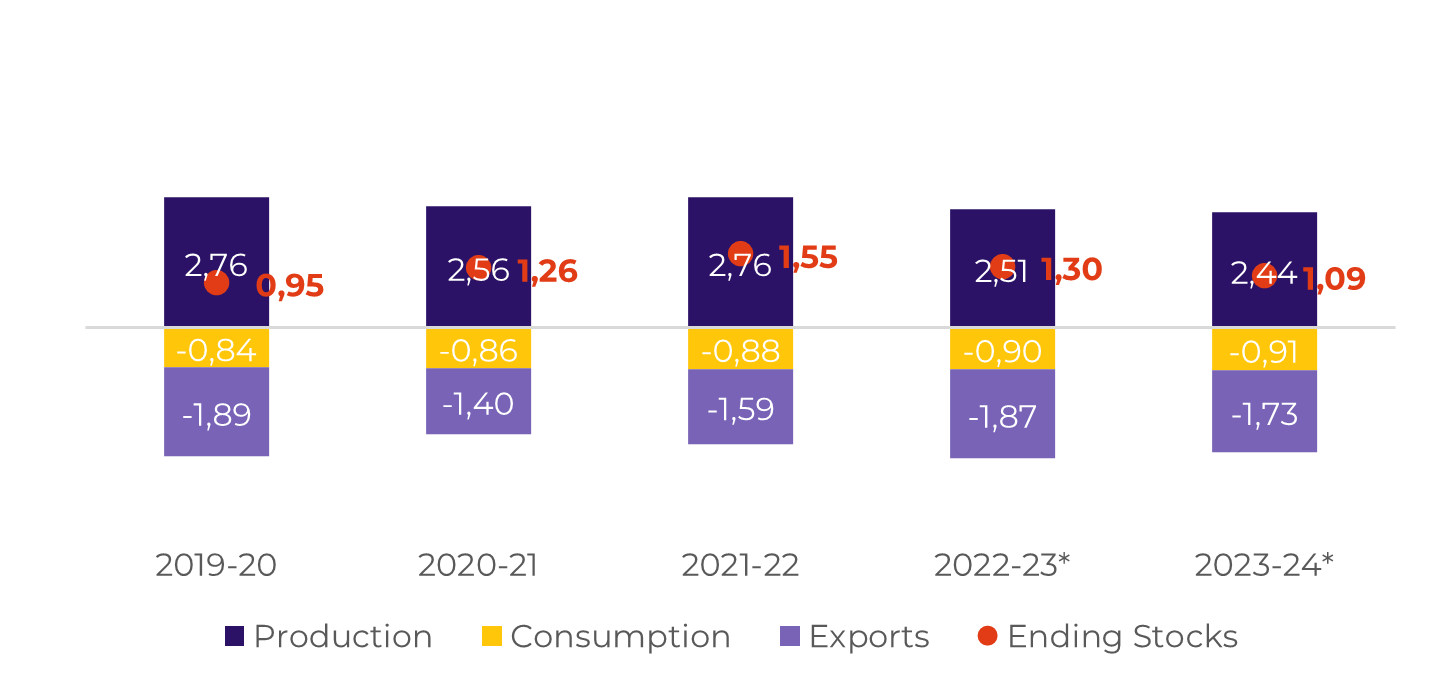

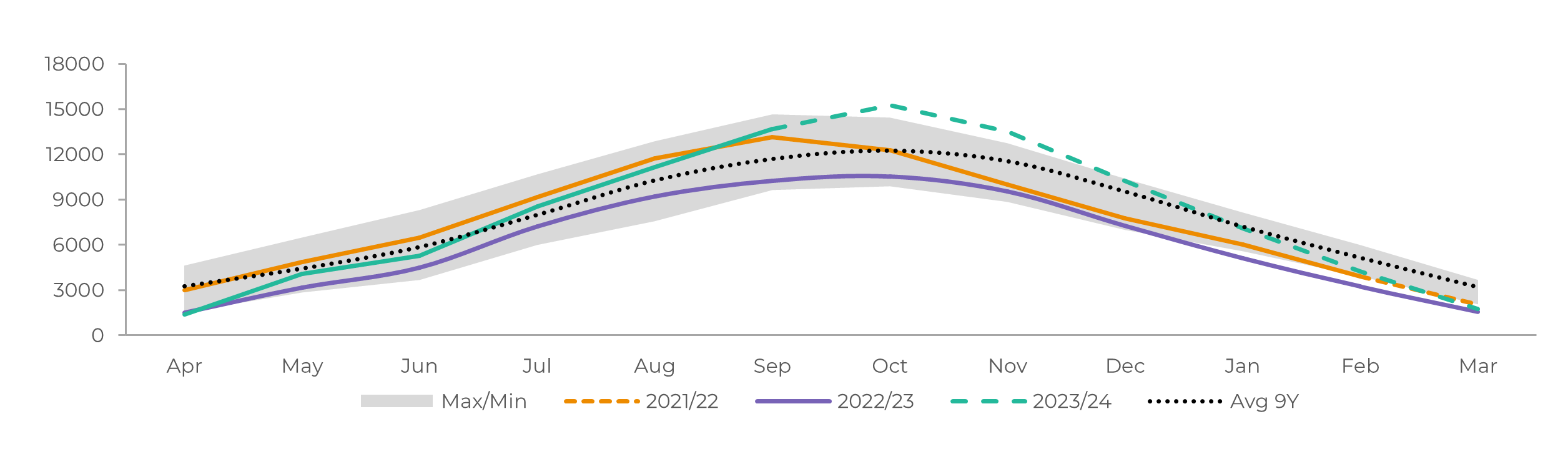

Although some models predict lower rains during Brazil's summer, prospects for 24/25 cane developments are good. The country could produce over 42Mt of sugar next season, especially considering recent investments in crystalization and the maitenance of a high sugar mix.

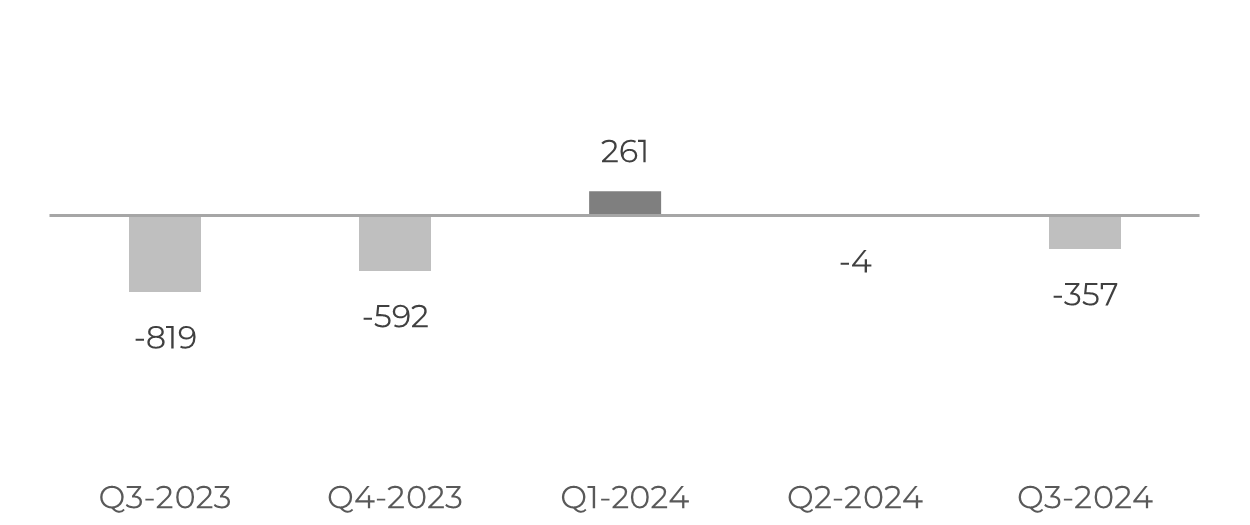

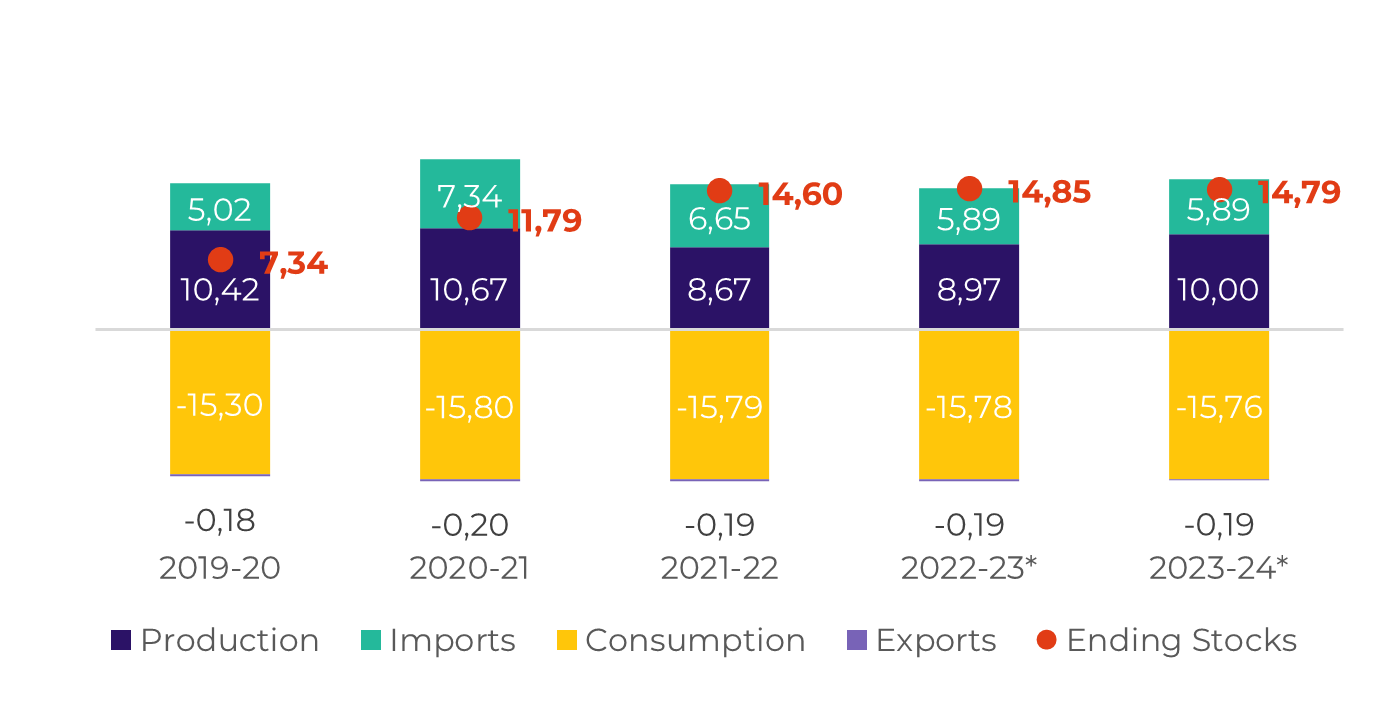

Source: SECEX, Williams, hEDGEpoint

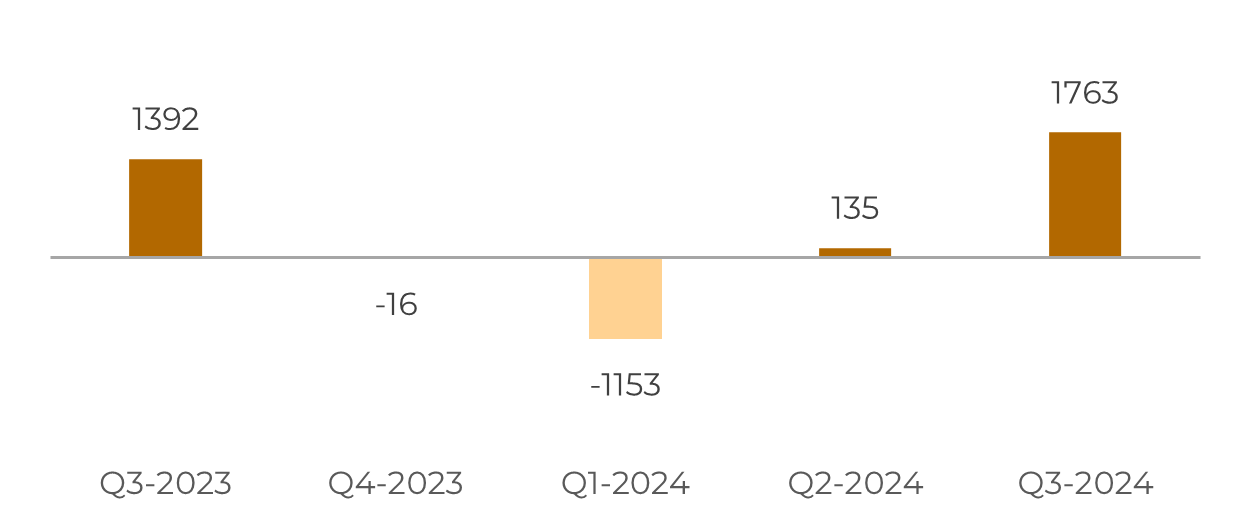

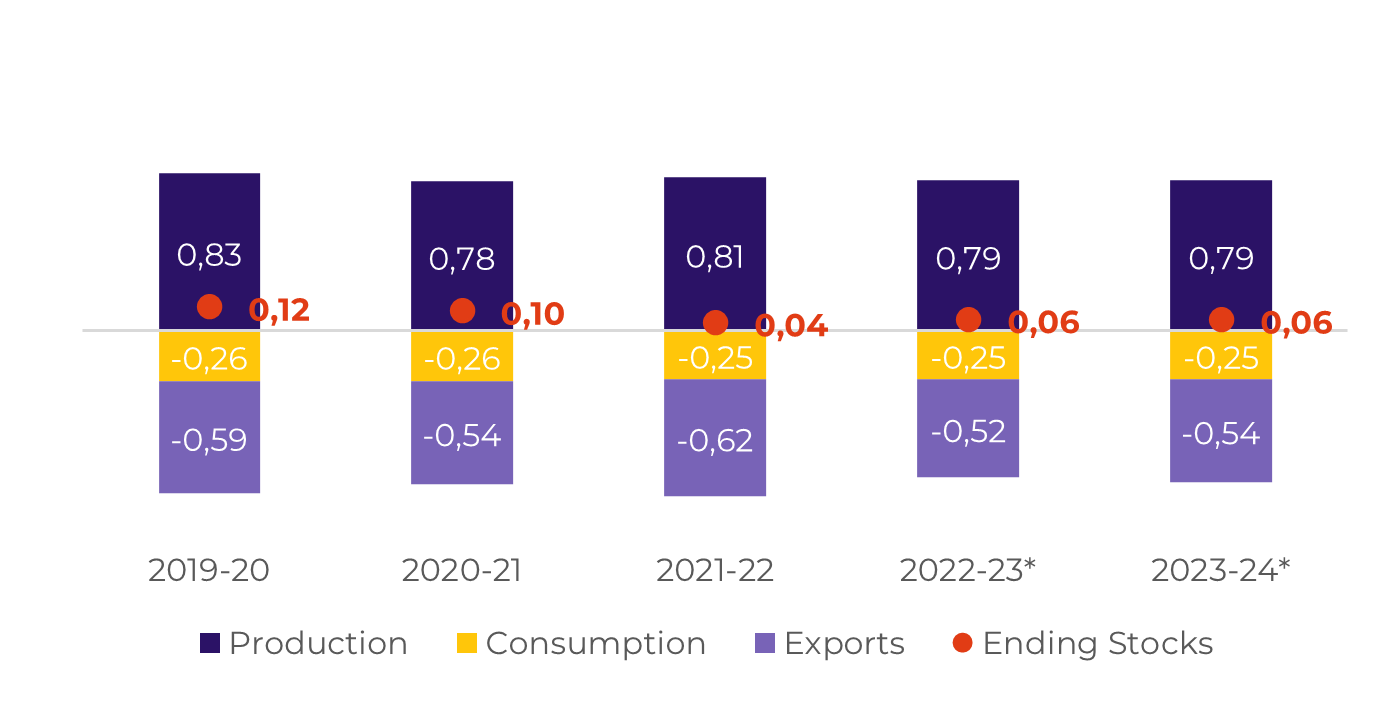

Source: Unica,MAPA, SECEX, Williams, hEDGEpoint