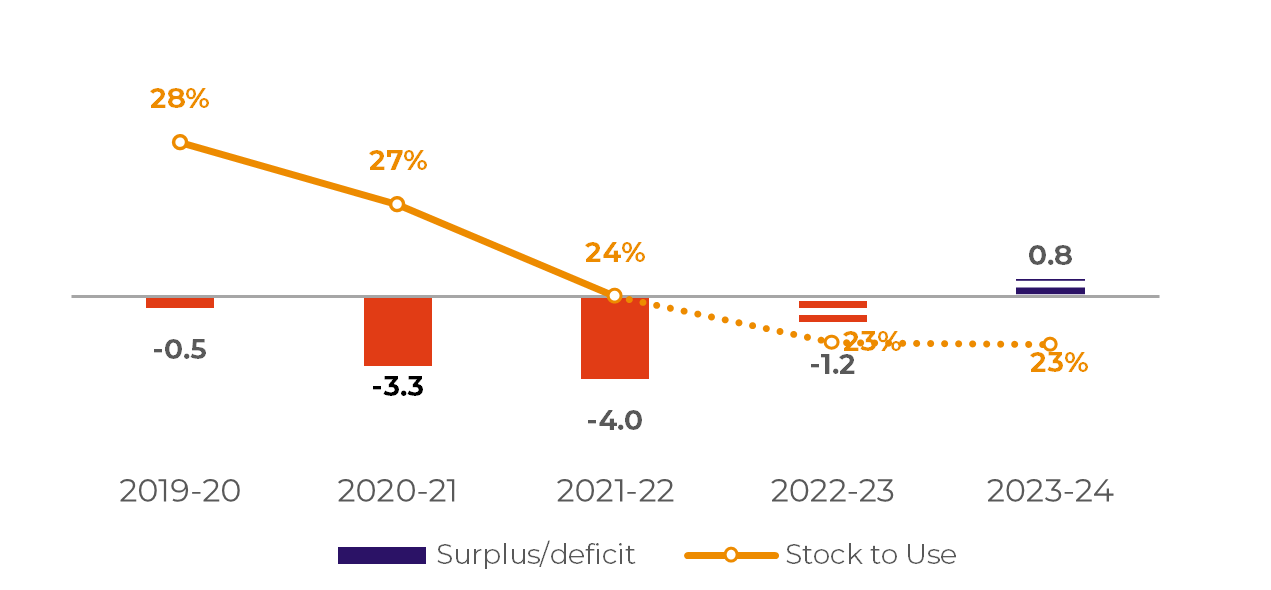

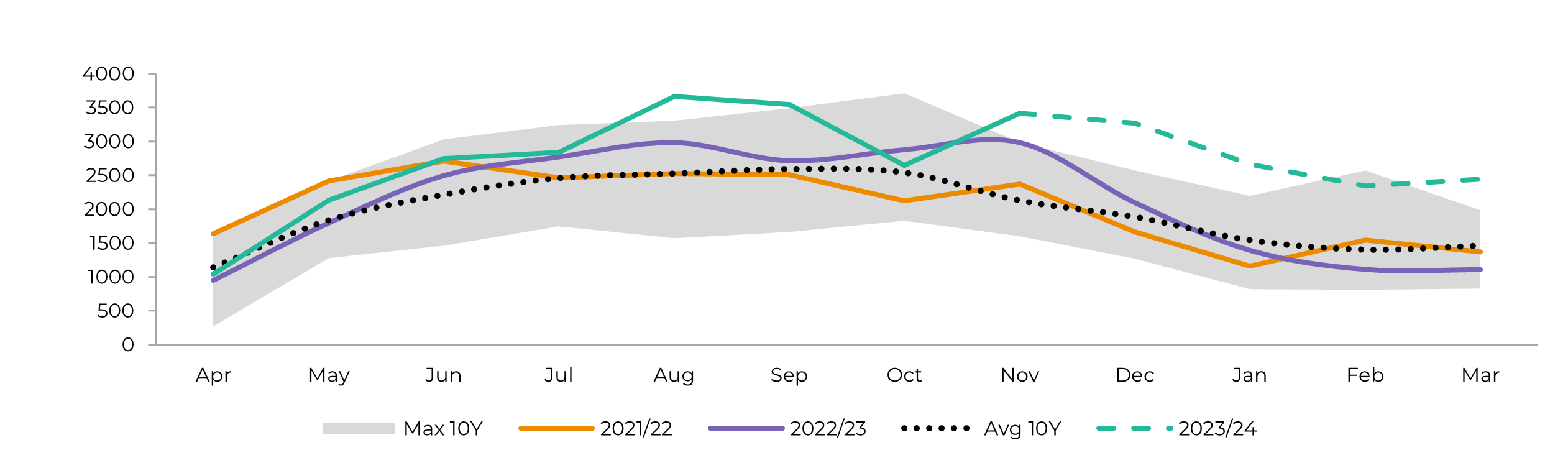

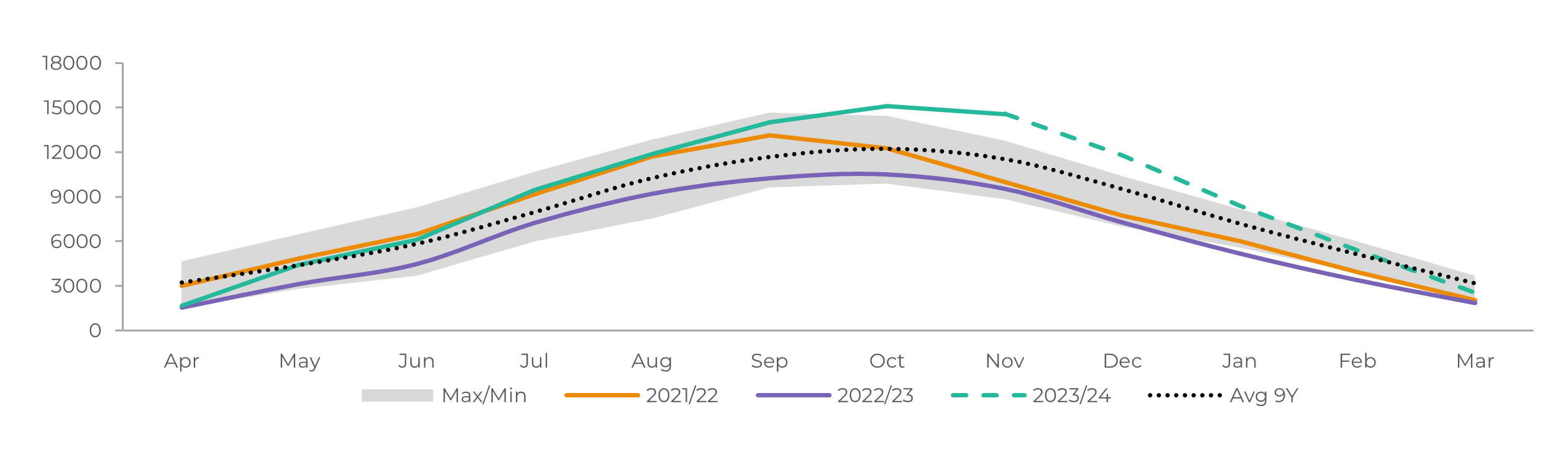

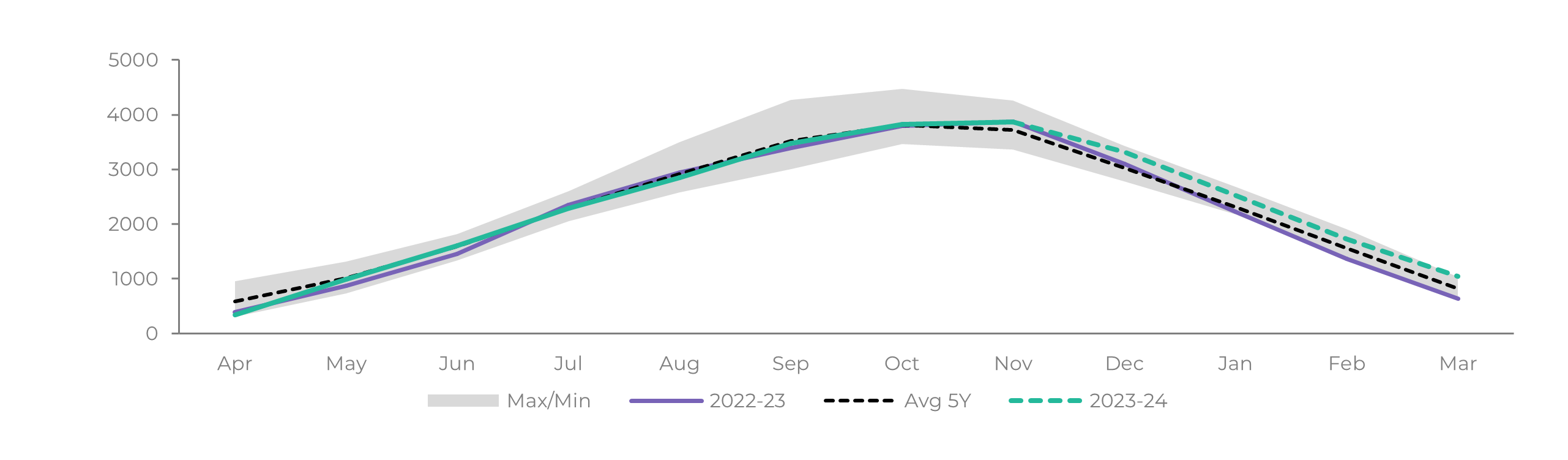

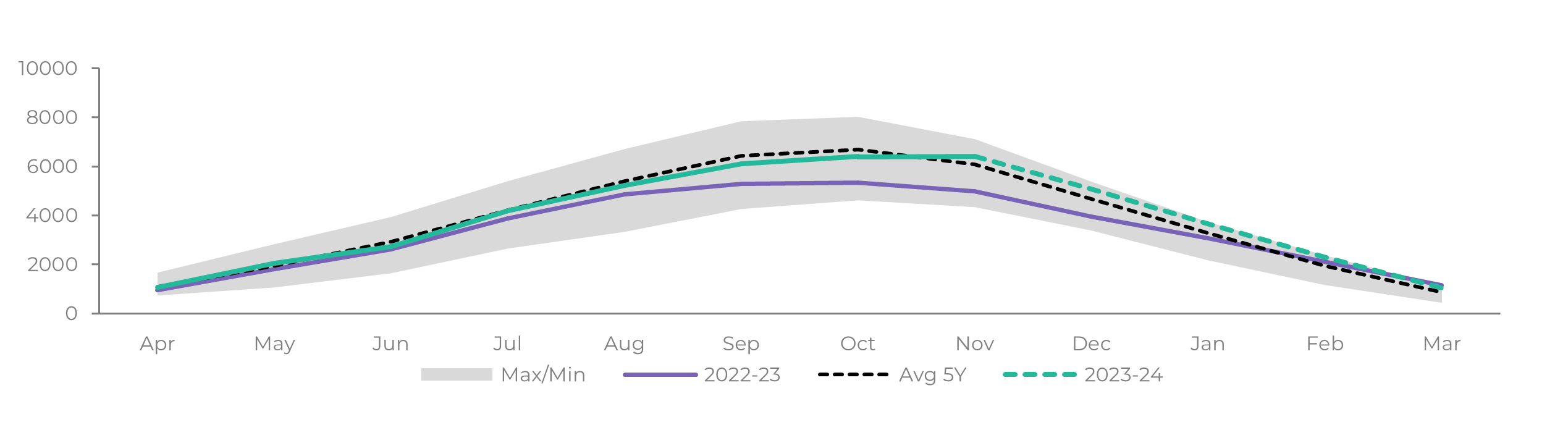

Prices melted as a result of the recent shift in fundamentals. Brazil has proven that paying enough leads to major investments and capacity expansion, while demand might be more cautious than in previous years.

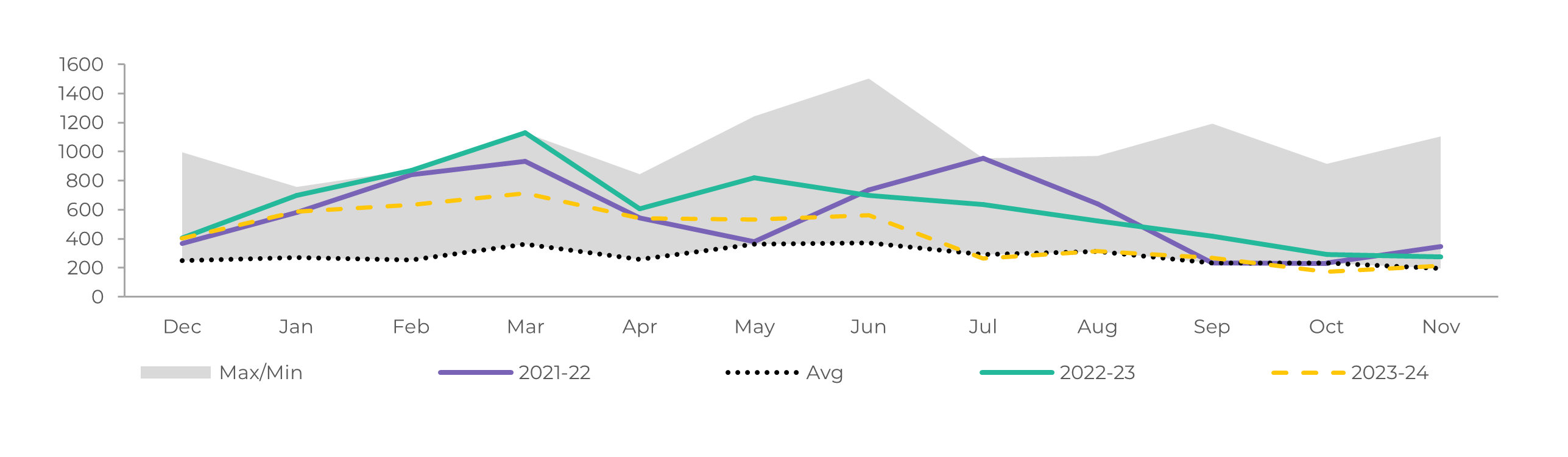

As a result, the trade flows' deficit doesn't seem as deep as once expected, being easily settled through import seasonality, especially as market expect another year of excelent results in Center-South during 24/25.

Of course, weather will remain a source of volatility, as recent hot weather can impact cane's development in Brasil. However, the conversion to an ENSO-neutral condition in mid-2024 also allows some optimism regarding the Northern Hemisphere's 24/25 season - yes, it is too soon to peg.

Still, it seems like we are walking away from catastrophy. Higher future availability complies with an inverted curve, while higher availability from Brazil induces a small carry between October24 and March25.