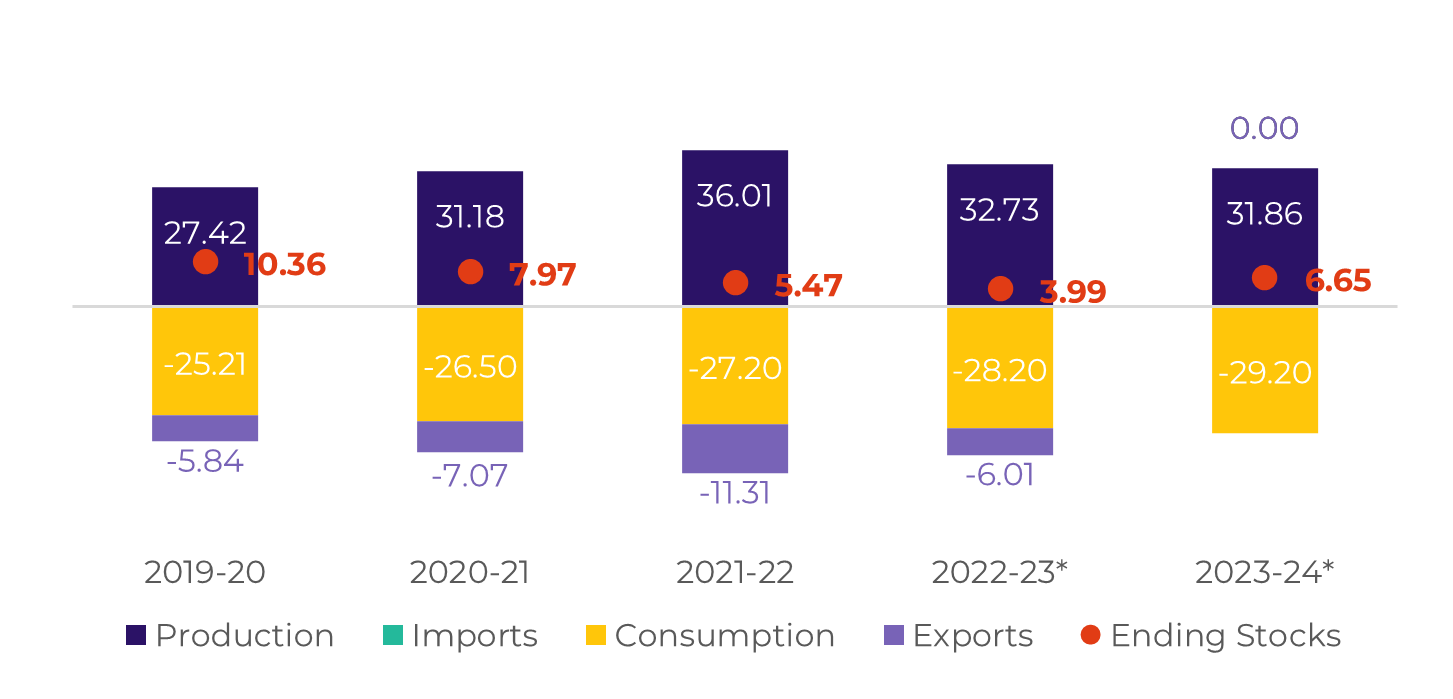

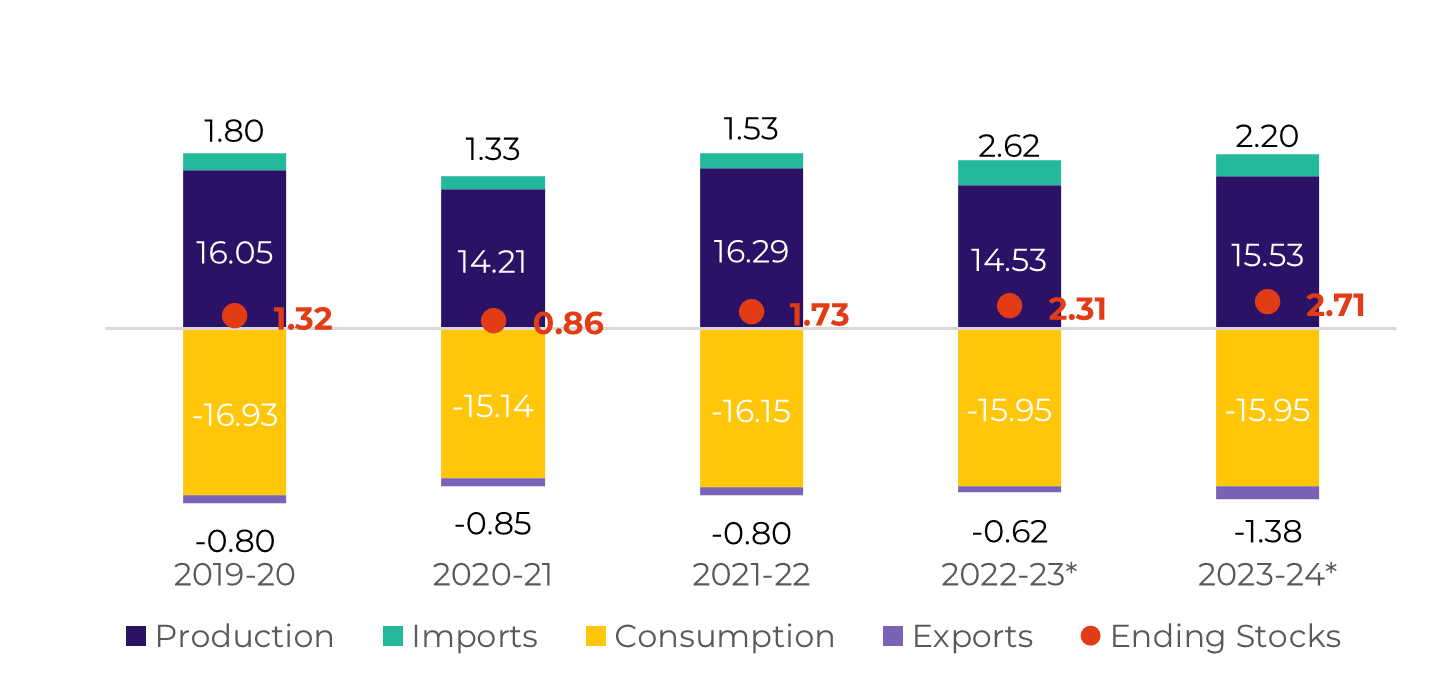

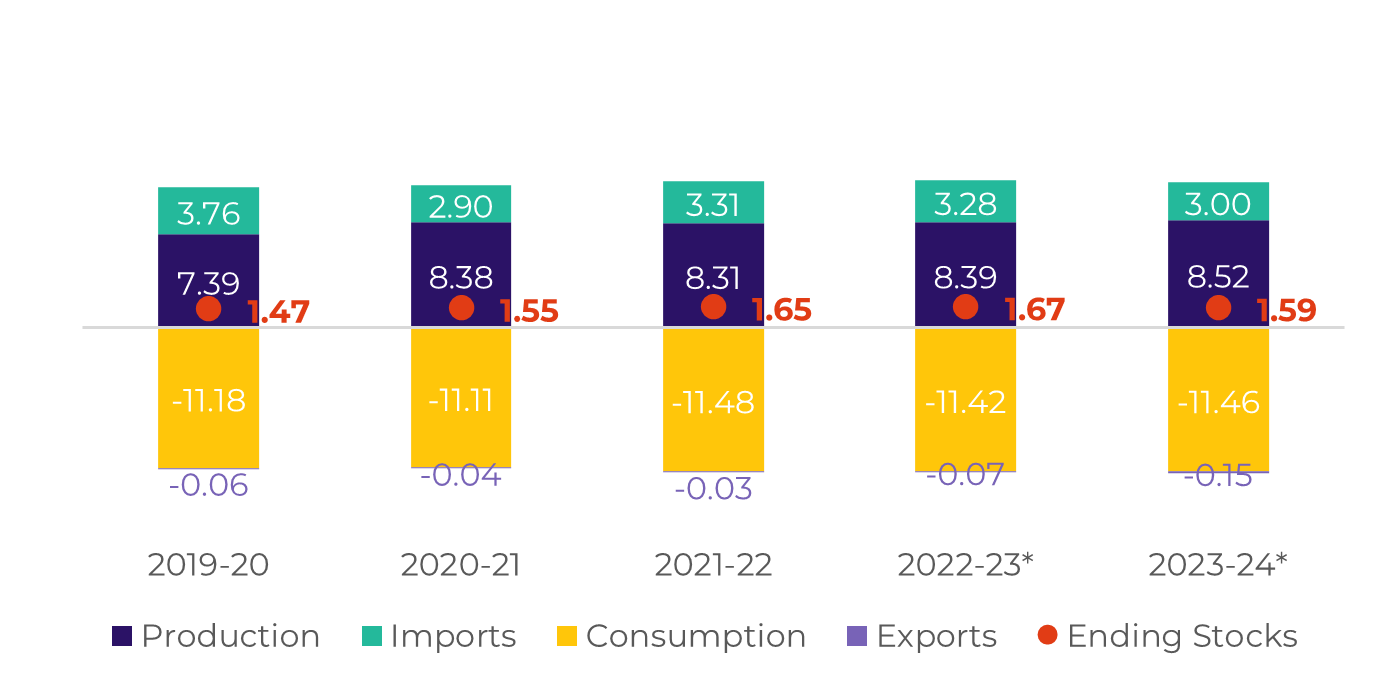

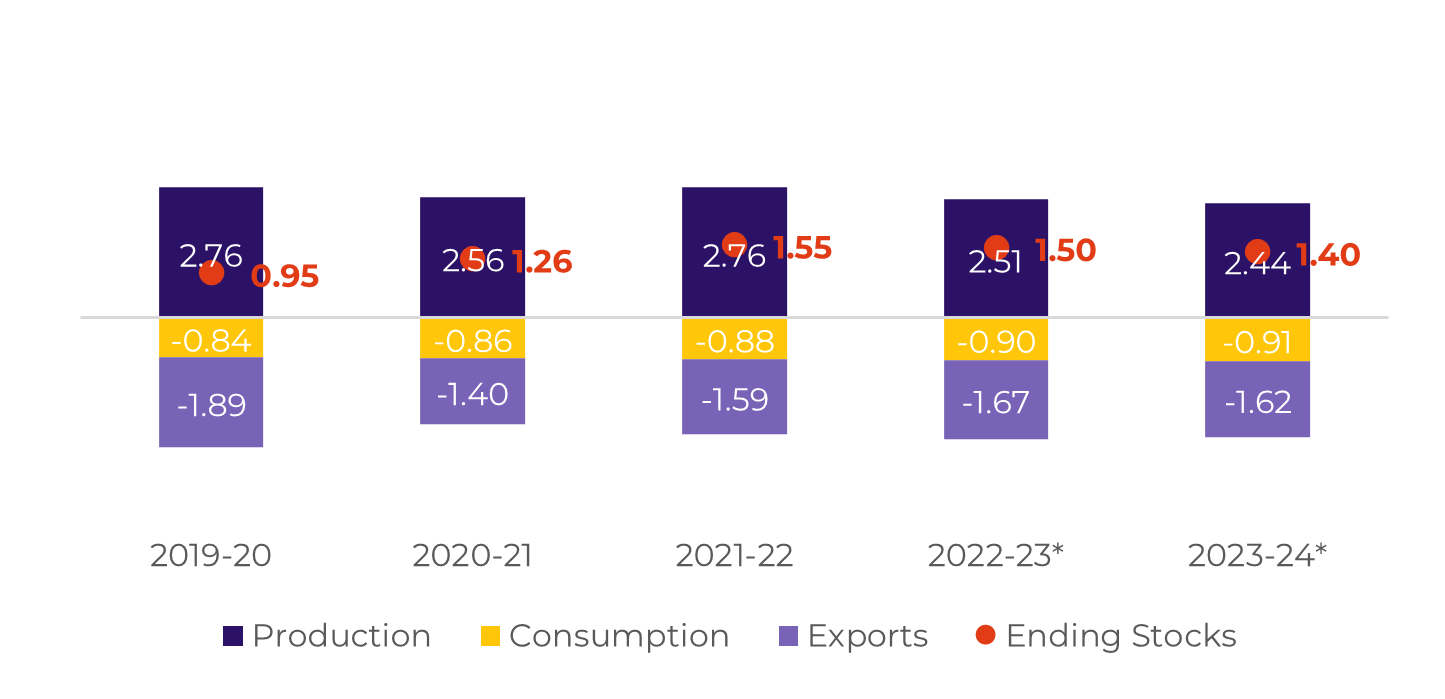

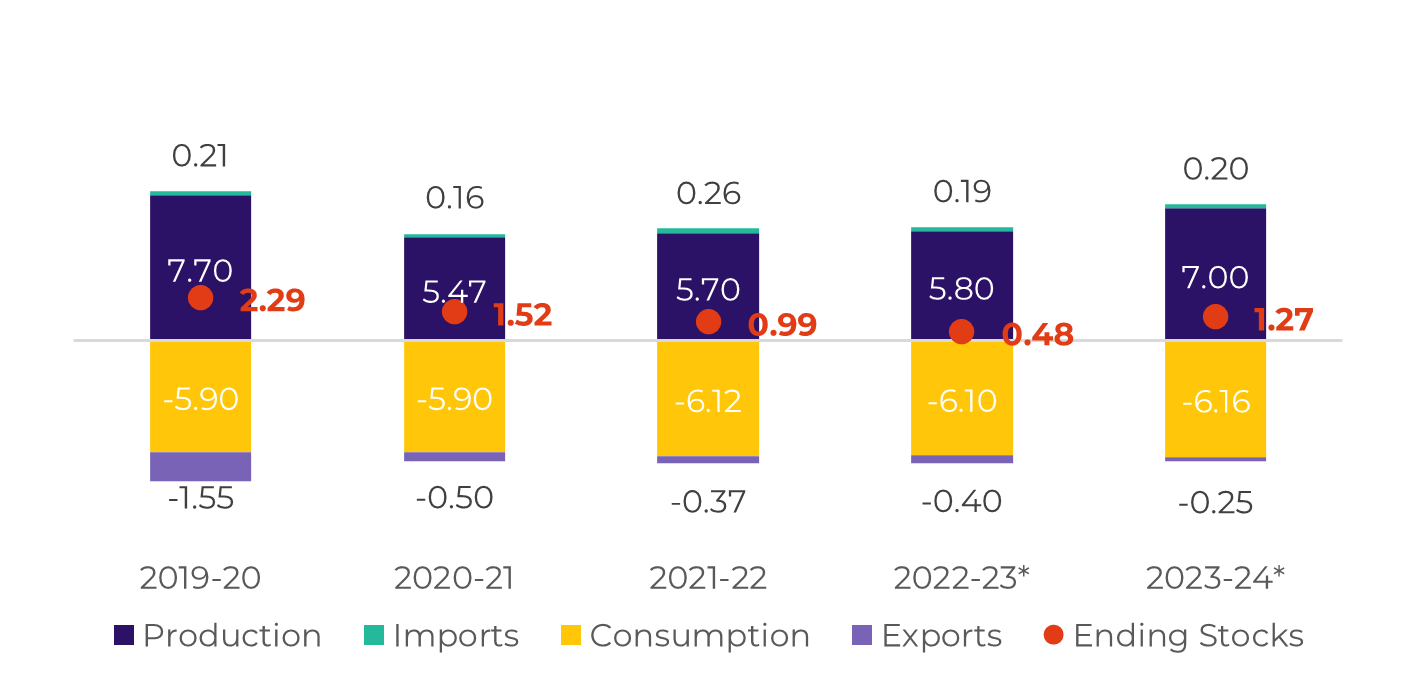

Source: Unica, MAPA, SECEX, hEDGEpoint

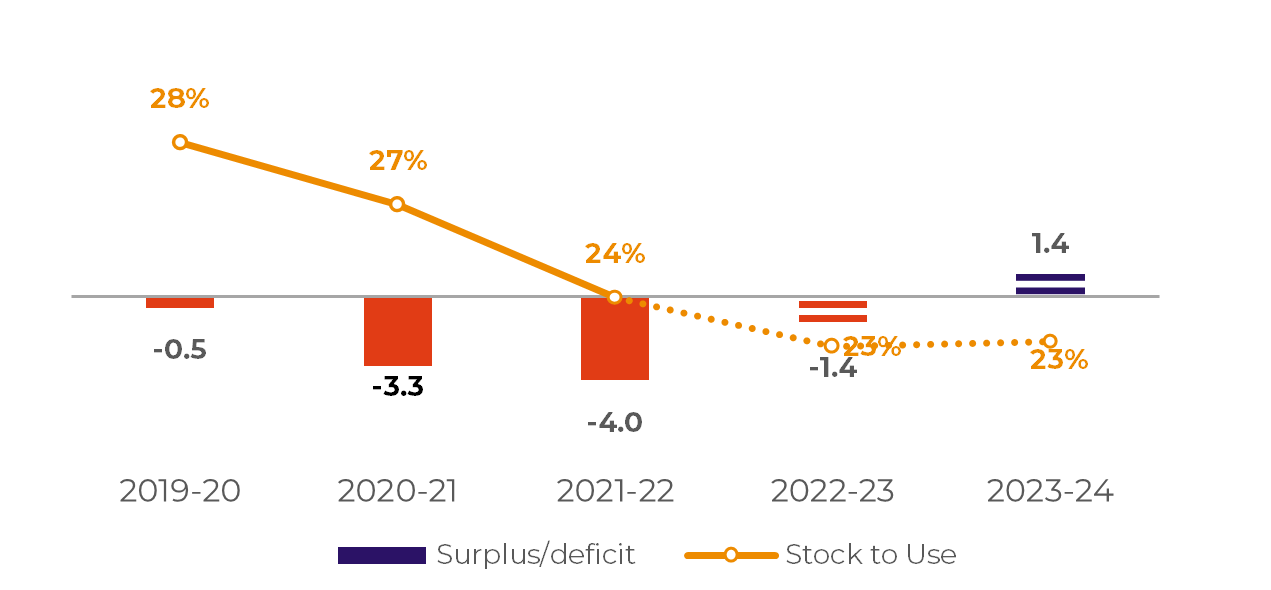

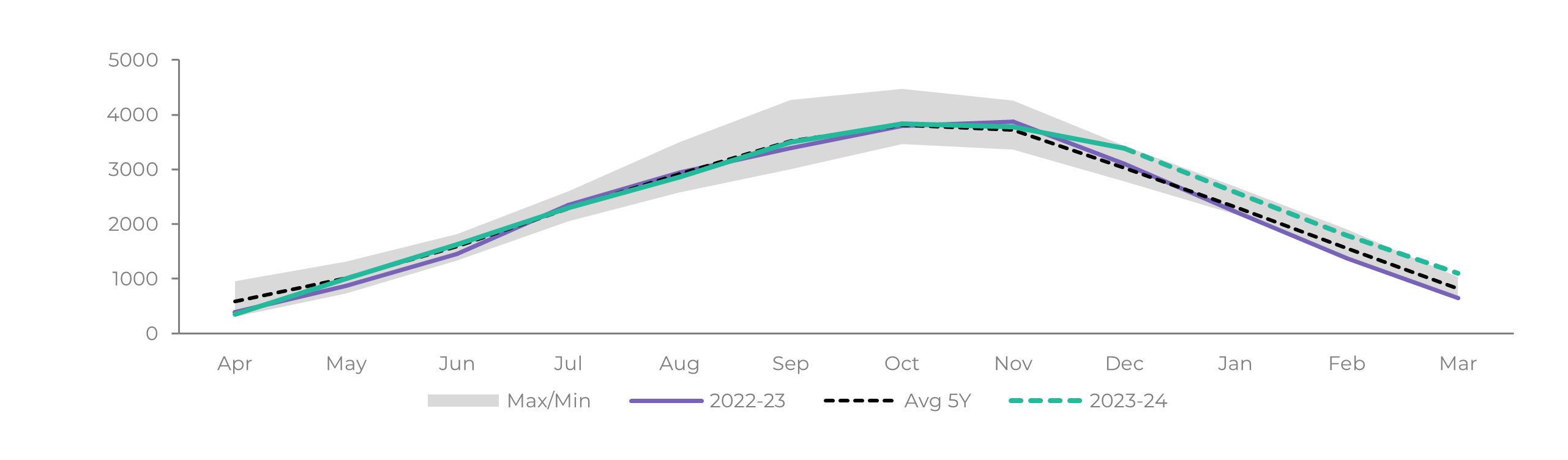

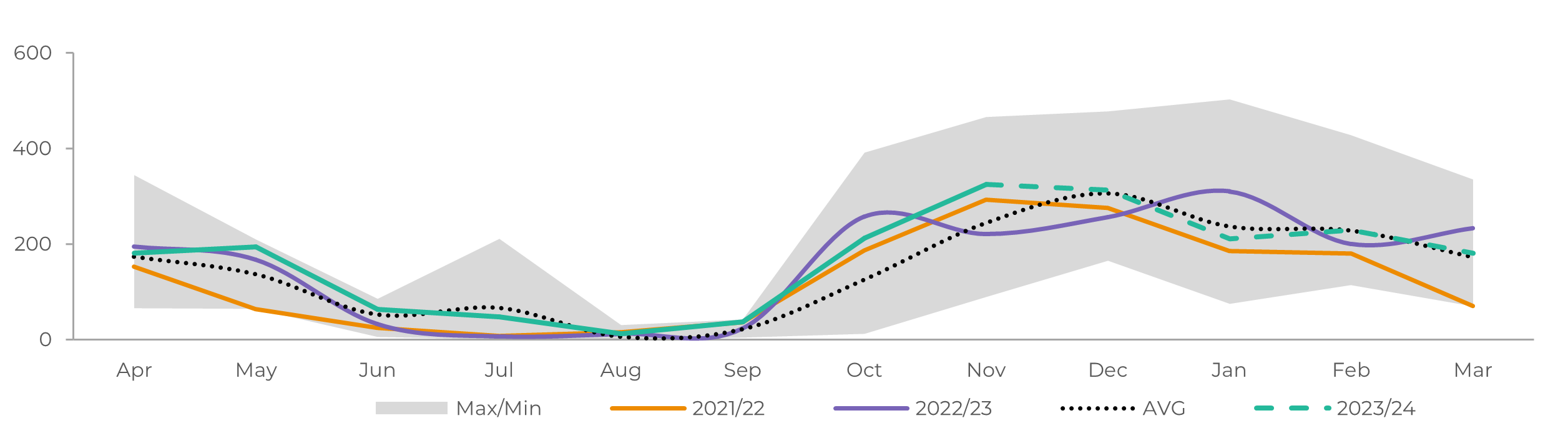

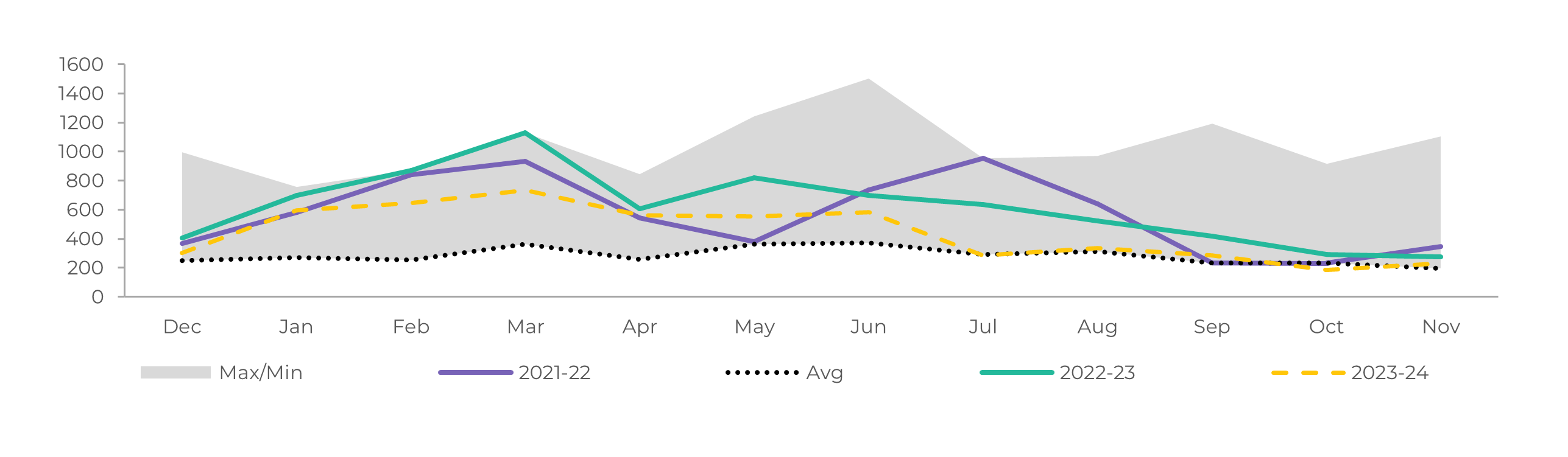

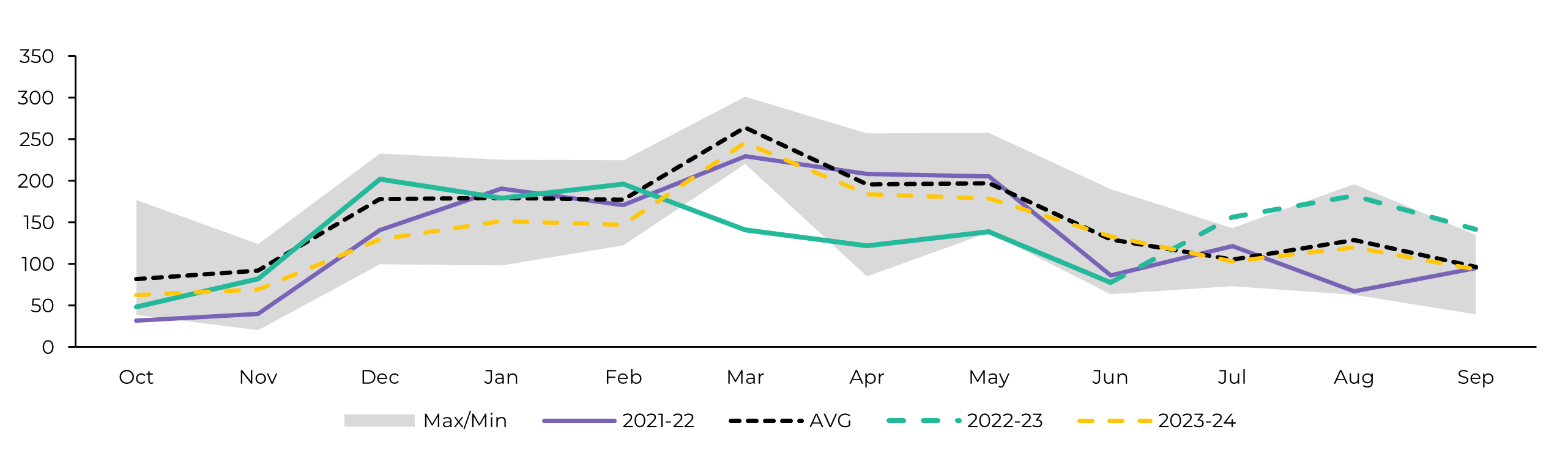

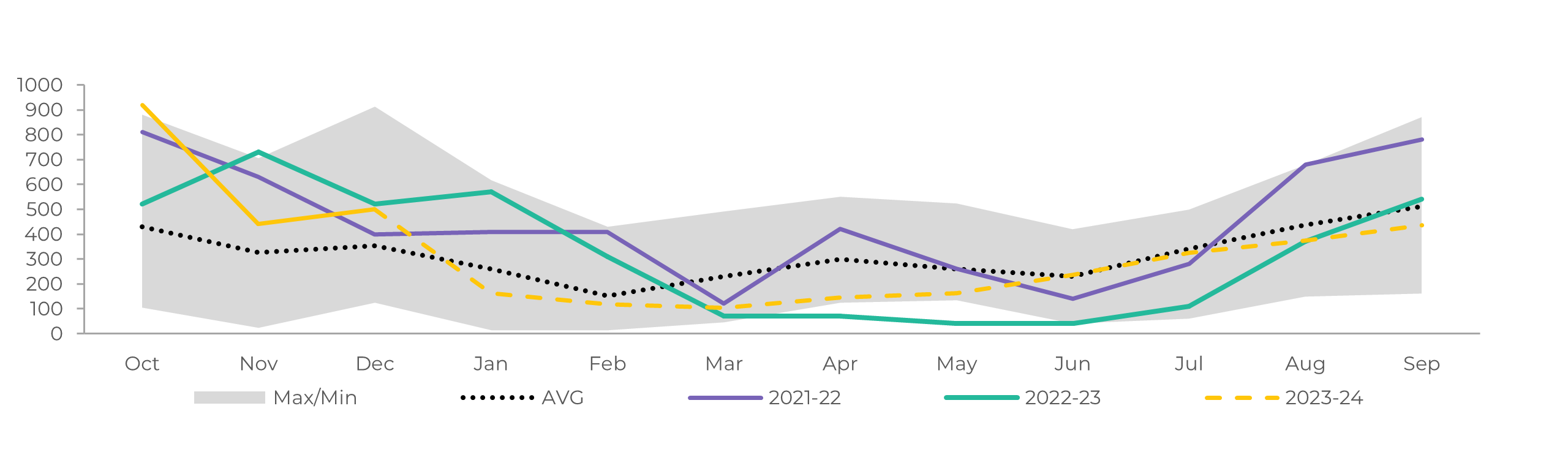

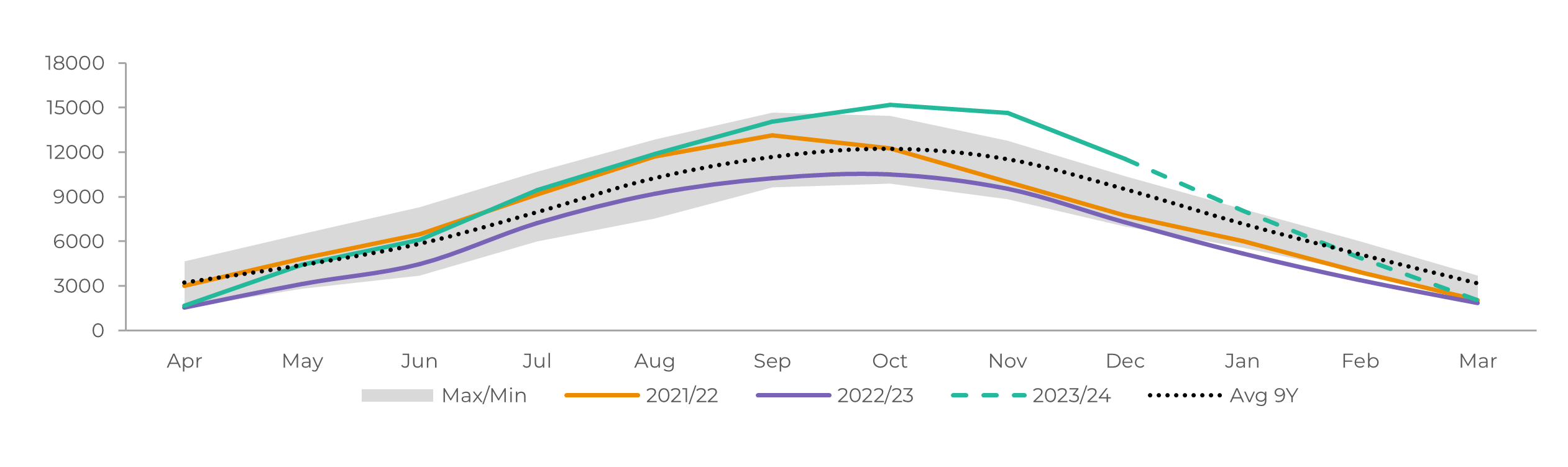

Crushing has already reached 645.4Mt by January's first fortnight. This means that if the weather remains average or slightly below, the region could end up crushing all of its 23/24's availability - which is close to 655 Mt.

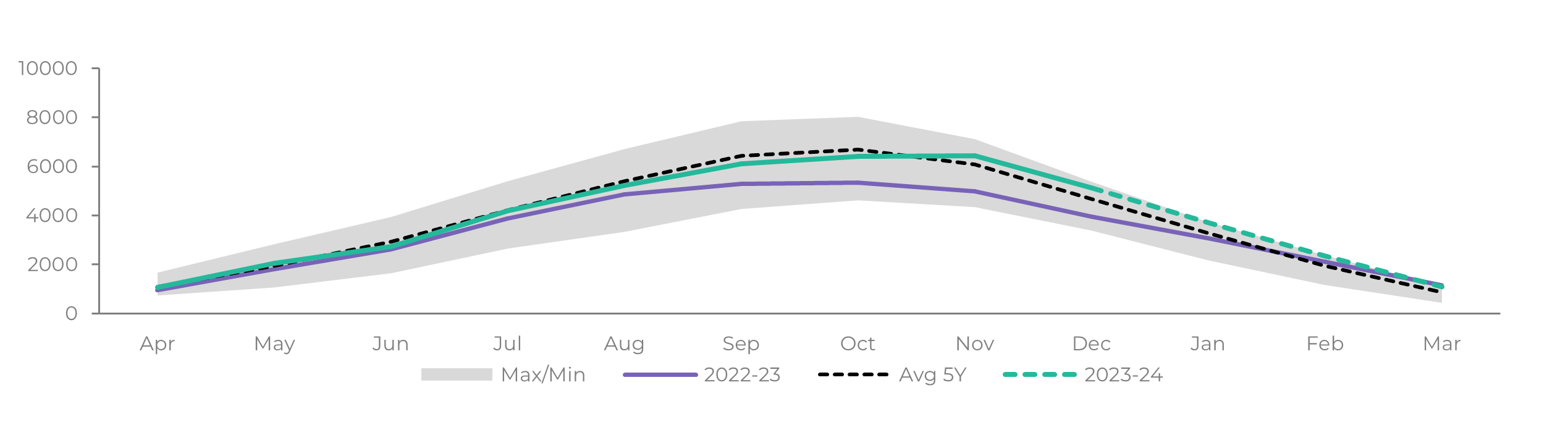

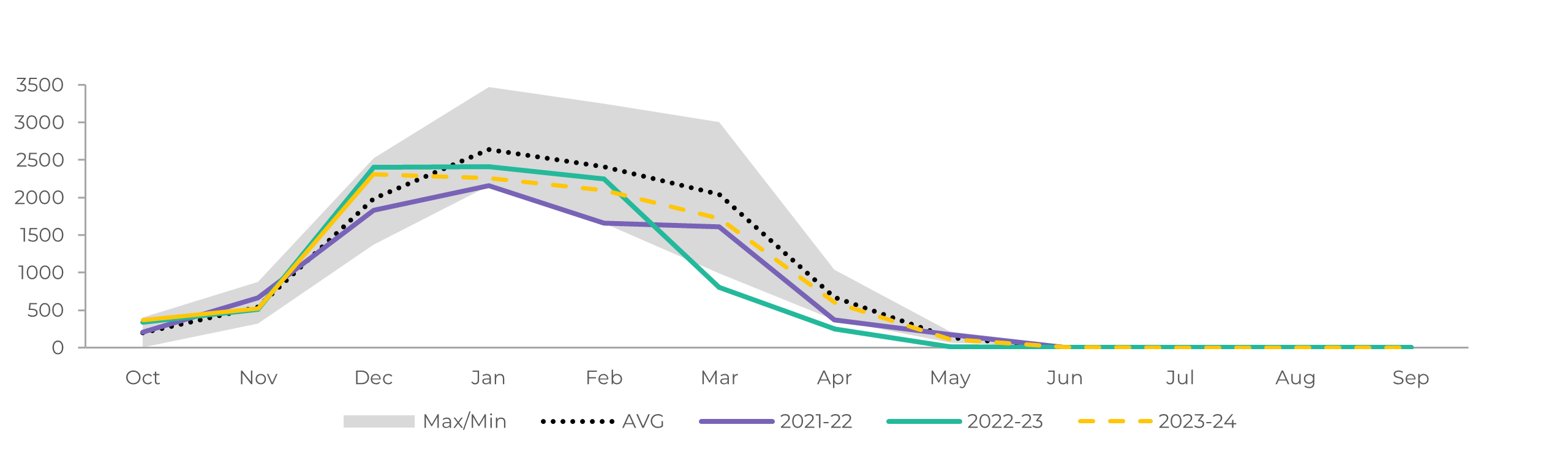

For the next season, weather hasn't been completely favourable for cane development, therefore, we should not expect crushing to reach the same levels as in 23/24. Currently, we estimate around 620 Mt of cane, which, when coupled with a higher sugar mix of nearly 51%, could lead to the Center South region's second-best sugar production level. Note that while there is a bullish risk regarding weather, investments in the crystallization process could induce higher sugar mix.

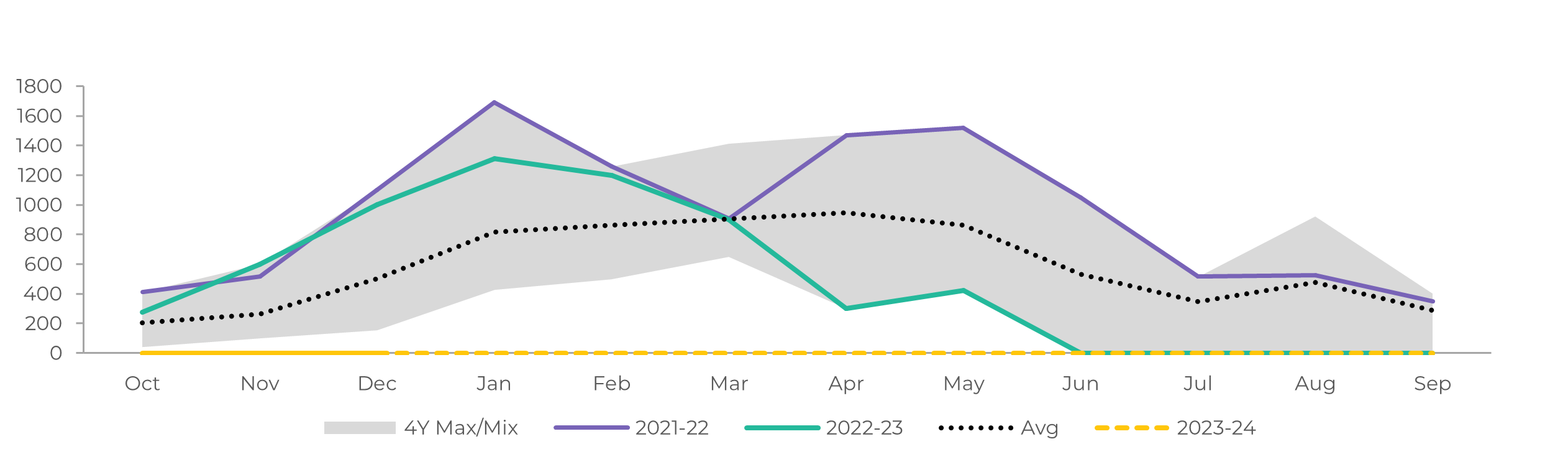

Source: SECEX, Williams, hEDGEpoint

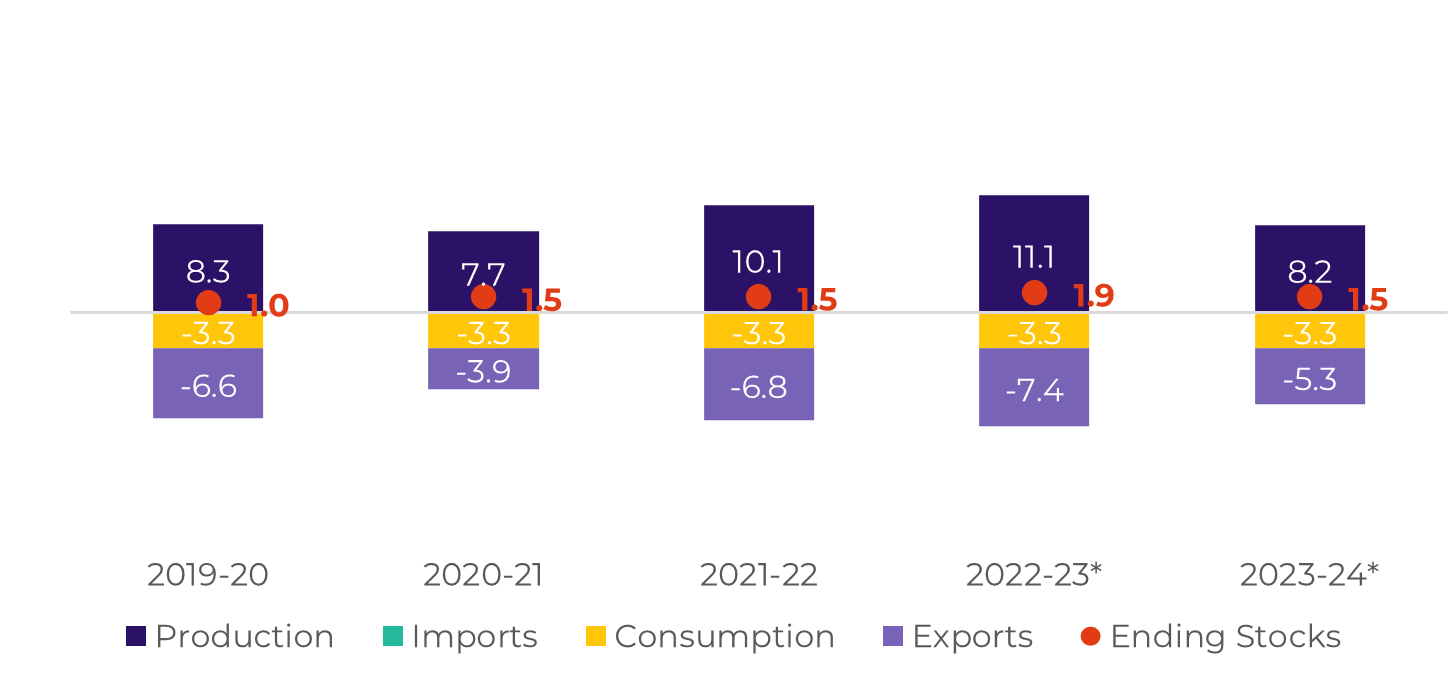

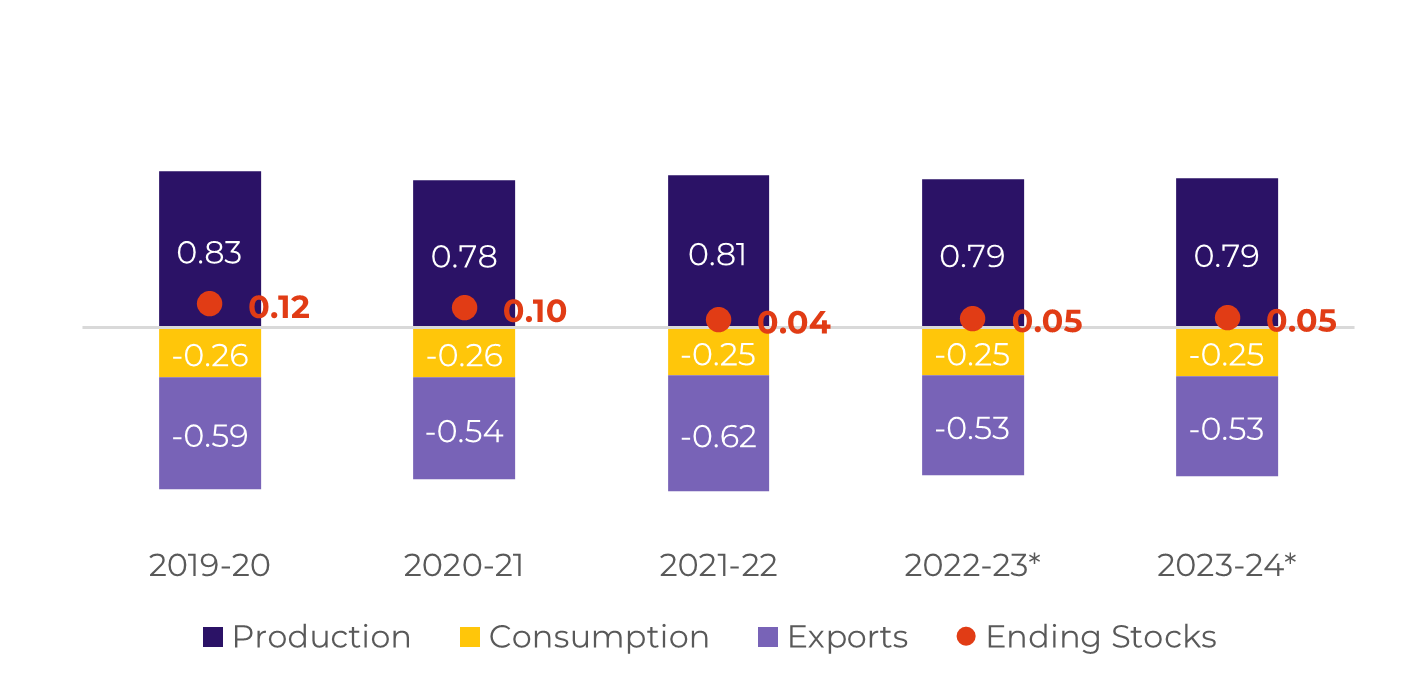

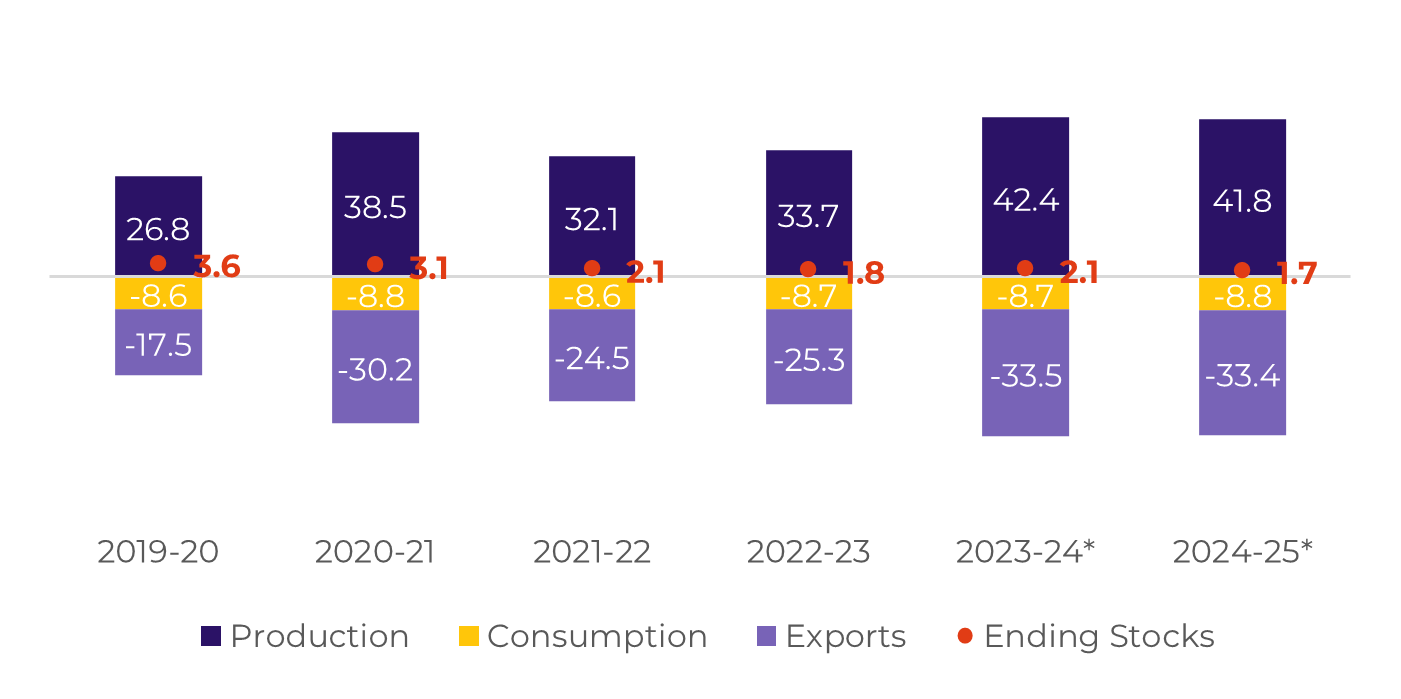

Source: Unica,MAPA, SECEX, Williams, hEDGEpoint