The global backdrop continues to be dominated by political and trade uncertainties. The recent announcement of a second wave of tariffs by Donald Trump, including Brazil among the countries affected, has imposed additional volatility on the market, with the tariffs possibly taking effect on August 1st. The main concern is the impact of inflation in the US, which could force the Fed to keep interest rates high, jeopardizing the expectation of a rate cut in September.

In the foreign exchange market, the dollar is depreciating against other currencies. This movement has a direct impact on Brazil, where the real continues to appreciate, challenging the competitiveness of Brazilian soybeans on international markets.

The global weather, under a neutral ENSO pattern, contributes to weather stability in the northern hemisphere, favoring the development of crops in the US and reducing the volatility typical of the weather market at this time of year.

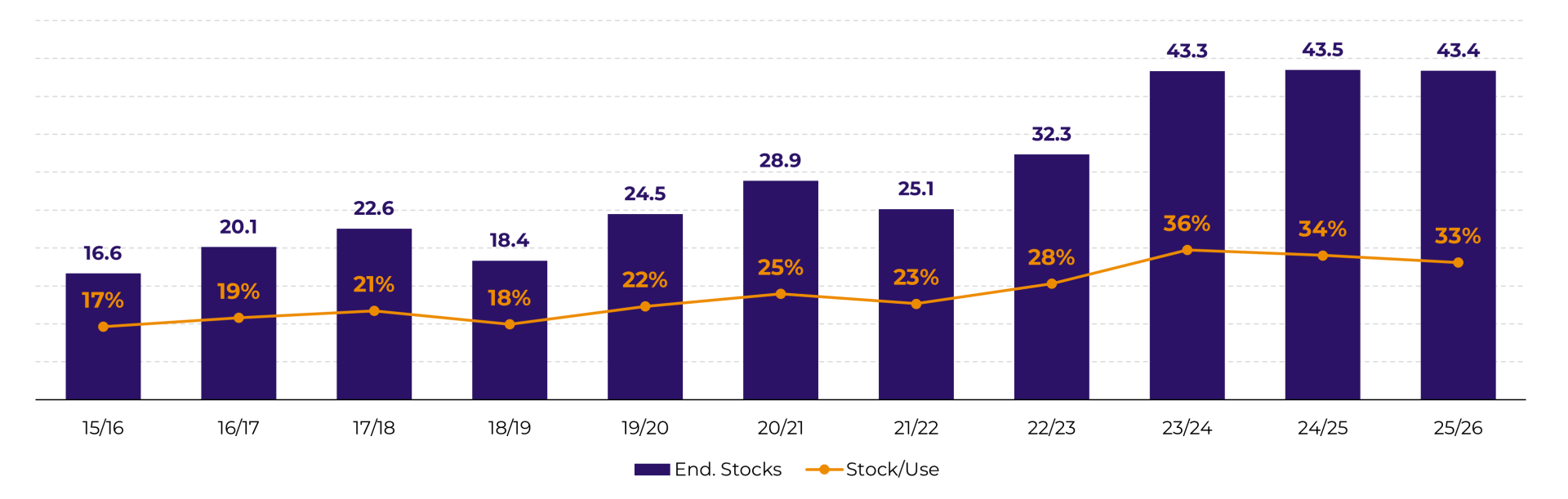

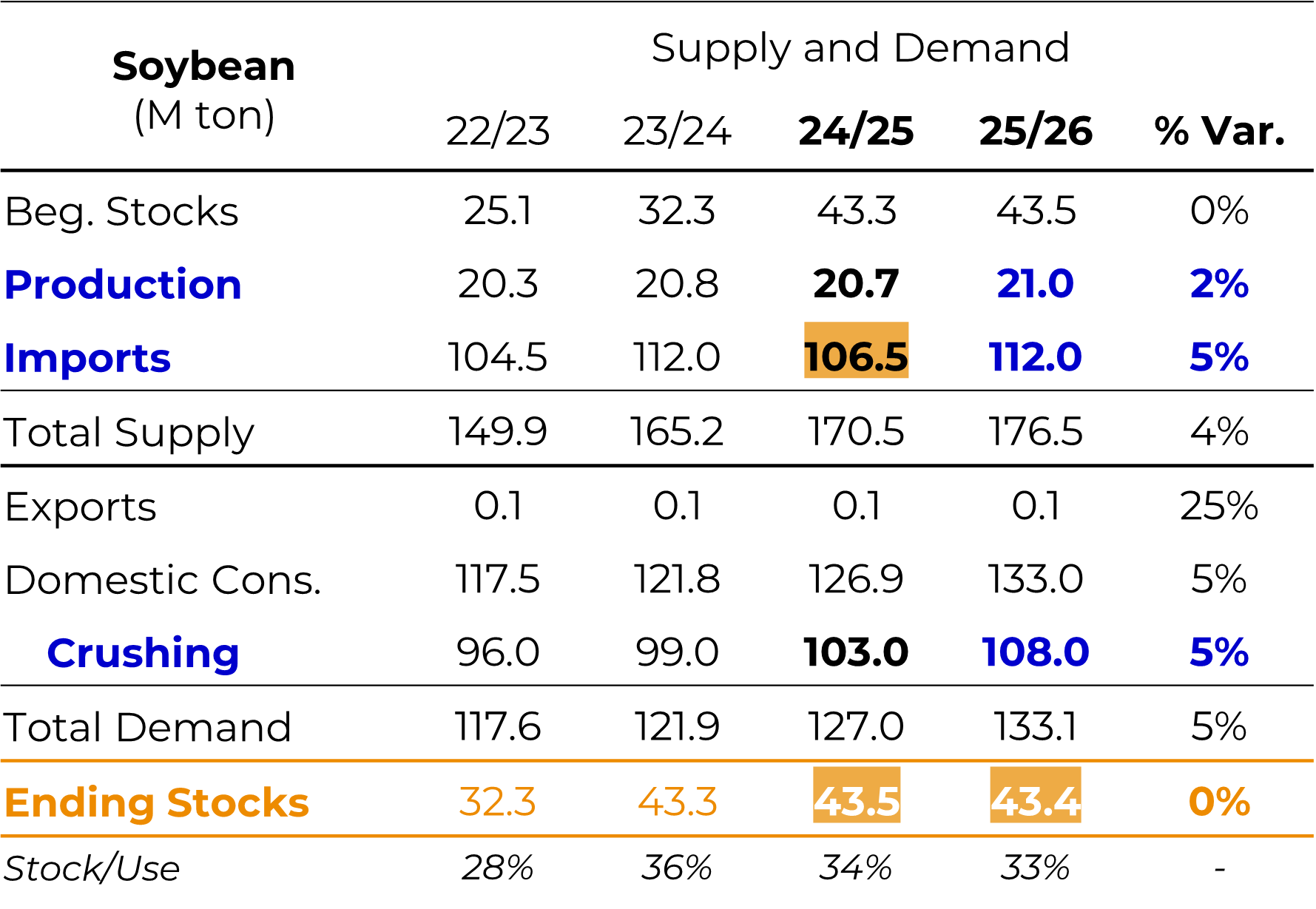

China has maintained stocks of more than 40 million tons for the third consecutive crop, reinforcing its food security strategy. This position reduces the sense of urgency in purchases, which, coupled with unattractive crushing margins, should limit demand in the short term. Ending stocks are estimated at 43.5 million tons for 2024/25, which represents a stock/use ratio of 34%. For 2025/26, stocks are projected at 43.4 million tons, with a stock/use ratio of 33%.

Imports for 2024/25 have been revised downwards, from 108 to 106.5 million tons, reflecting a lower appetite in the face of stock recomposition and weaker crushing margins. Even so, the USDA projects a rise to 112 million tons in 2025/26, although this projection depends on an improvement in crushing margins and domestic demand.

Chinese crushing continues to expand, estimated at 103 million tons for 2024/25 and 108 million tons for 2025/26, but with limited profitability.

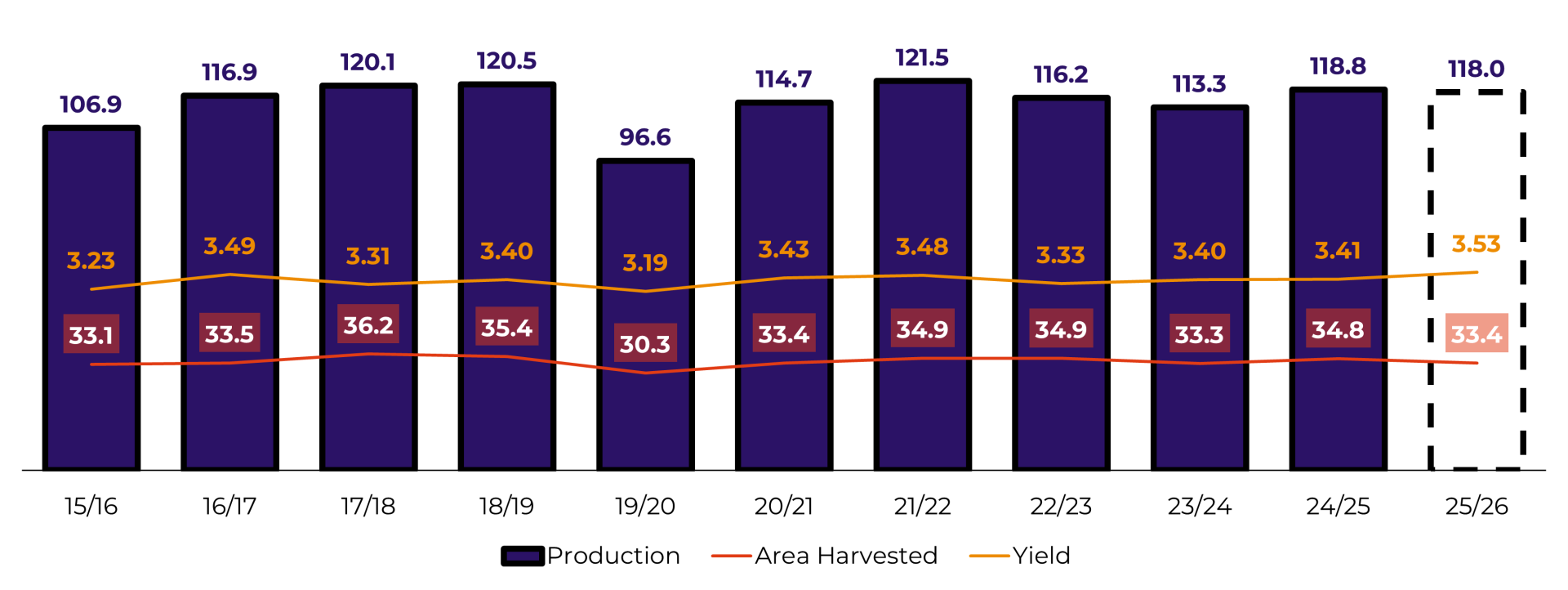

The 2025/26 crop remains at the center of market discussions, with a special focus on the favorable weather that supports expectations of record yields, even with a reduced area. According to the USDA, 70% of crops are in good or excellent condition (compared to 68% in 2024), signaling a "full crop". However, we must remember that the month of August is decisive for soybean development.

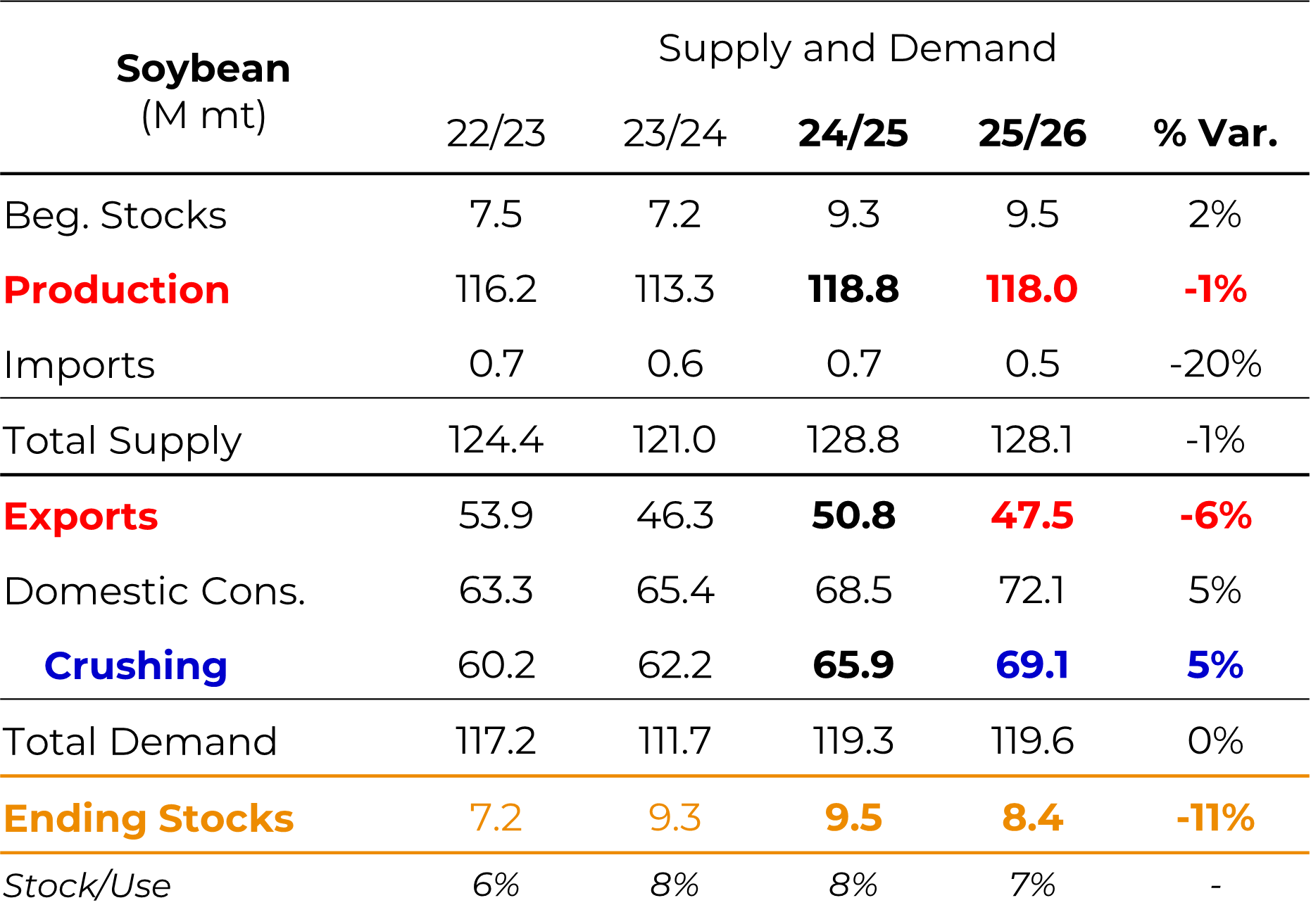

The US Environmental Protection Agency's (EPA) proposal to increase the mandatory biofuel blend to 67% is a key factor. Soybean oil accounts for approximately 70% of biodiesel and renewable diesel production. If approved, the proposal could generate an increase in crushing of between 2.5 and 5 million tons, which could bring US ending stocks down to between 4 and 7 million tons.

In the case of soymeal, the increase in supply is unlikely to be accompanied by growth in demand. Herds are stable and cannot absorb the possible additional volume. The result: stocks projected at levels three times higher, with a natural downward bias.

As for soyoil, potentially growing demand, tight stocks and positive margins make the scenario bullish. Funds have maintained a long position in oil, unlike grain and meal.

The oil share is now close to 50%, the highest level since the 2021/22 season, which would historically justify prices theoretically above US$ 12 per bushel for soybean in Chicago. However, the market continues to trade between US$ 10.00 and US$ 10.50, indicating some disconnect between fundamentals and pricing.

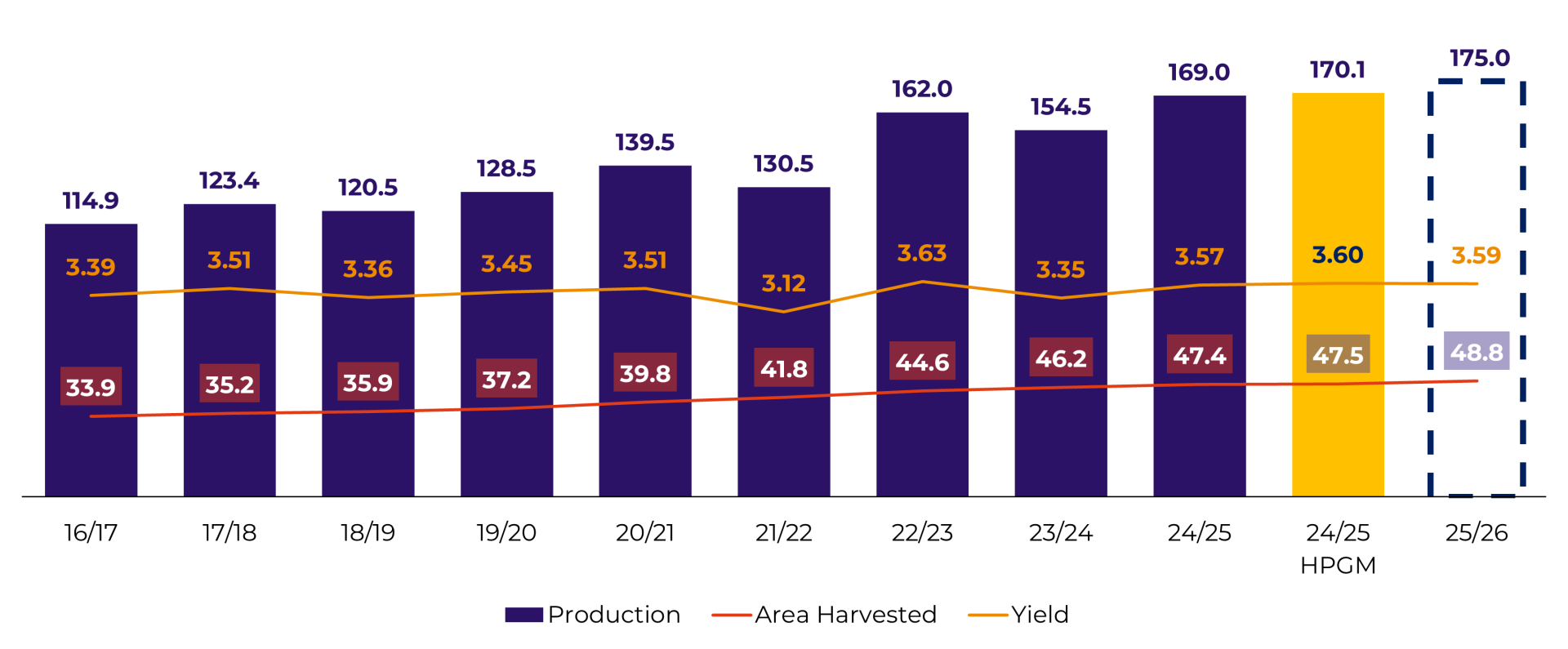

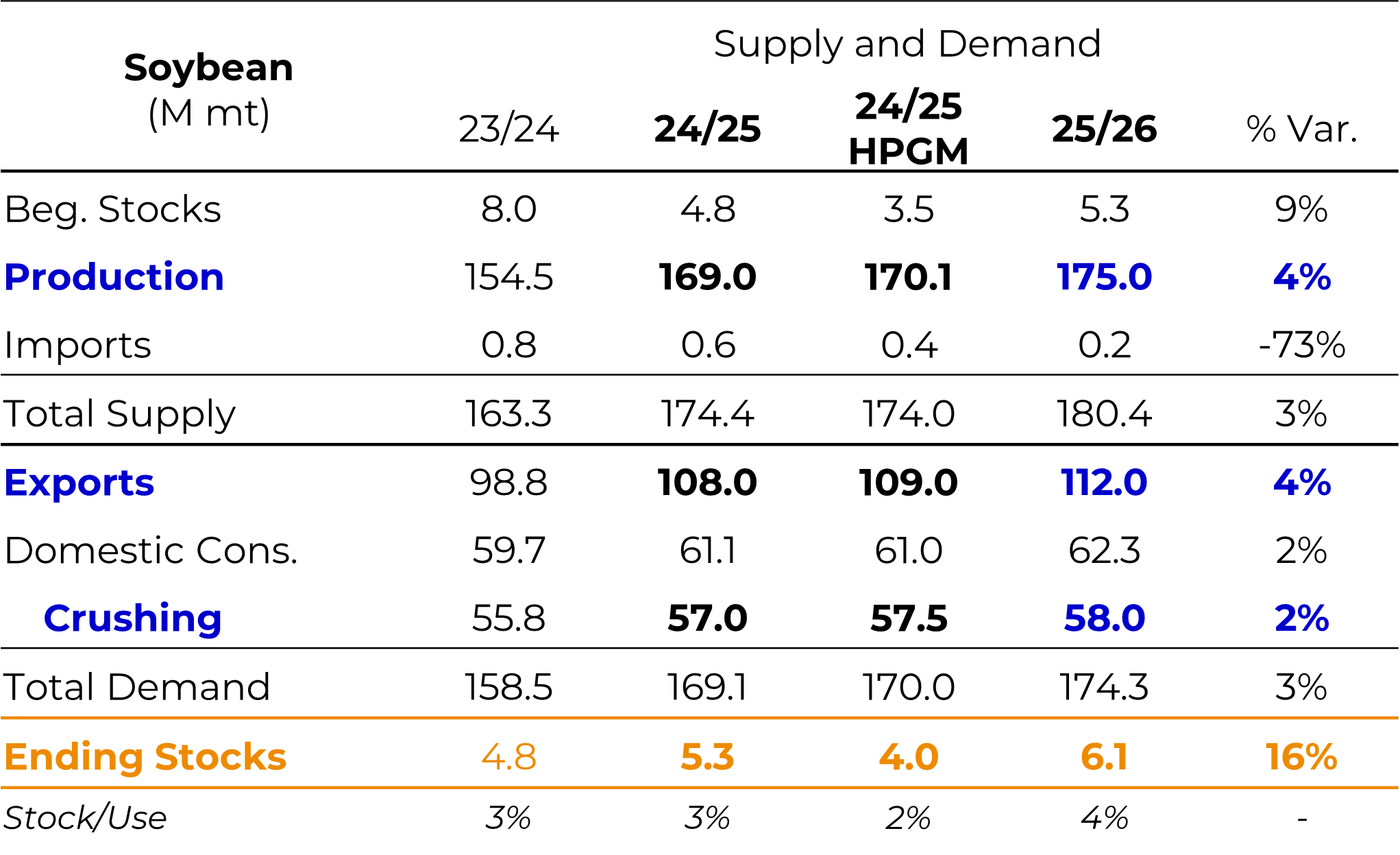

The 2024/25 crop is practically consolidated at 170 million tons, with exports potentially reaching a record 109 million tons due to strong Chinese demand. Crushing remains strong and will be reinforced by the introduction of B15 (biodiesel blend) from August.

For the 2025/26 crop, the discussion is already turning to a new production level: between 180 and 185 million tons, if weather and technology advance together.

The second half of the year will be marked by a dispute between exports and the domestic market. The crushing margin has been falling, although it is within the seasonal range. The decision between selling soybean or corn is also on the agenda: corn may be held back more, favoring the supply of soybean.

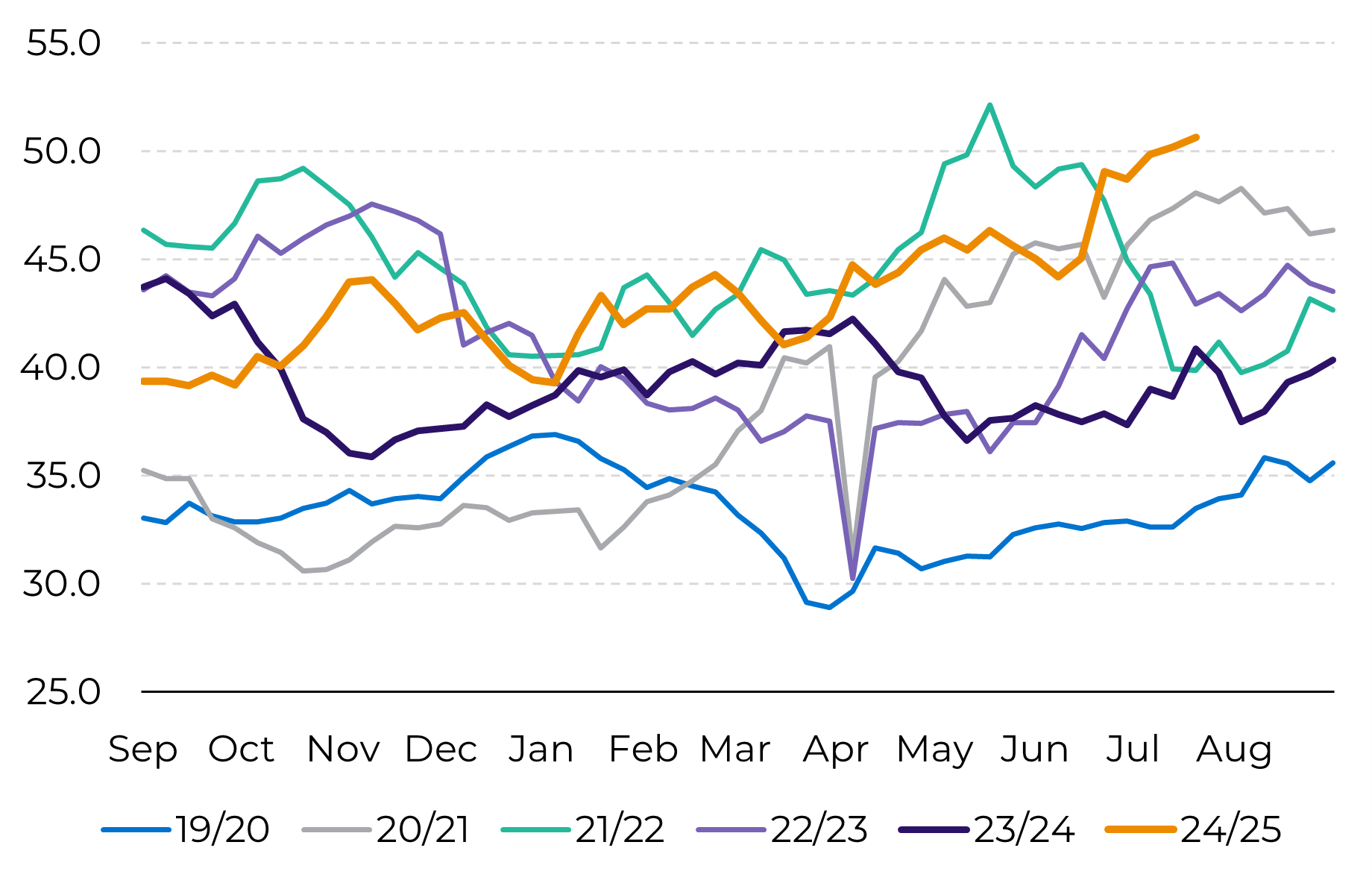

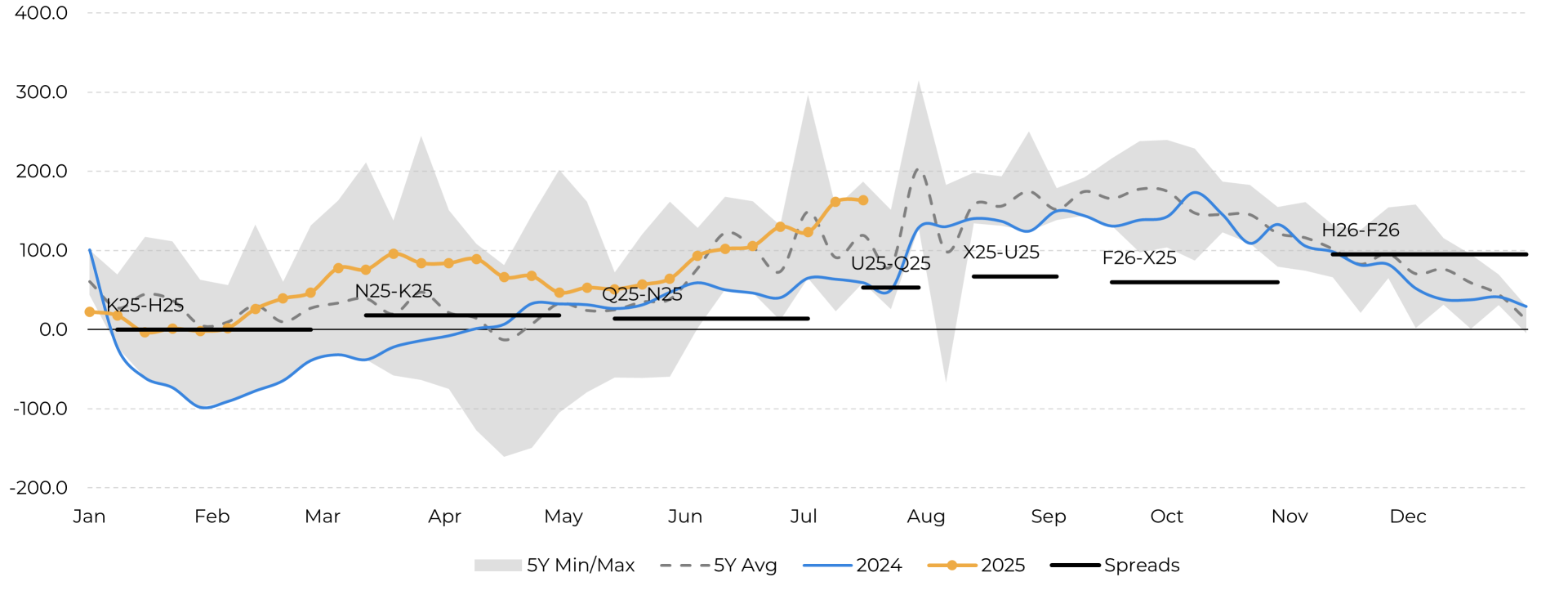

High basis premiums are supporting prices at the moment, partially compensating for Chicago and the exchange rate.

Crushing industry:

• Crushing margins under pressure, although within the seasonal range.

• Meal: Uncertainties regarding exports due to the return of Argentina and a possible increase in American supply.

• Oil: more positive outlook with B15 and potential increase in domestic demand.

Source: CME, Esalq, Hedgepoint

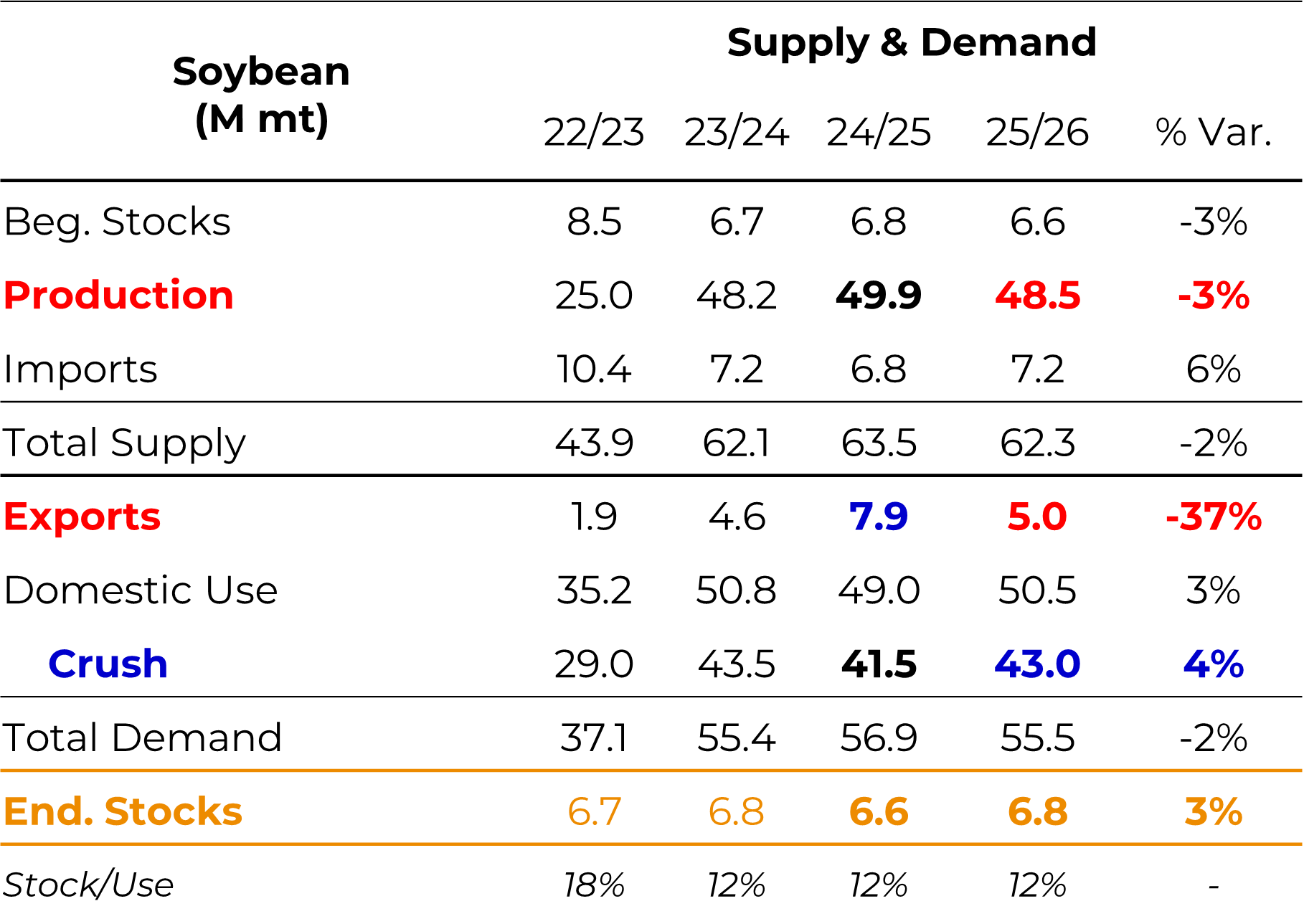

Argentina is once again gaining relevance in the market after the collapse of the 2022/23 crop. Production for 2024/25, although below potential, has reached consistent levels (~50 million tons), which should allow for exports of up to 8 million tons of grain. Reforms by the Milei government and a more stable exchange rate favor Argentina's competitiveness.

By 2025/26, soybean areas are expected to migrate to corn due to the cereal's better profitability, which should reinforce Argentina's focus on crushing and exporting meals and oil, putting pressure on competitors such as Brazil and the USA. The industrial processing park remains robust and focused on exporting by-products.

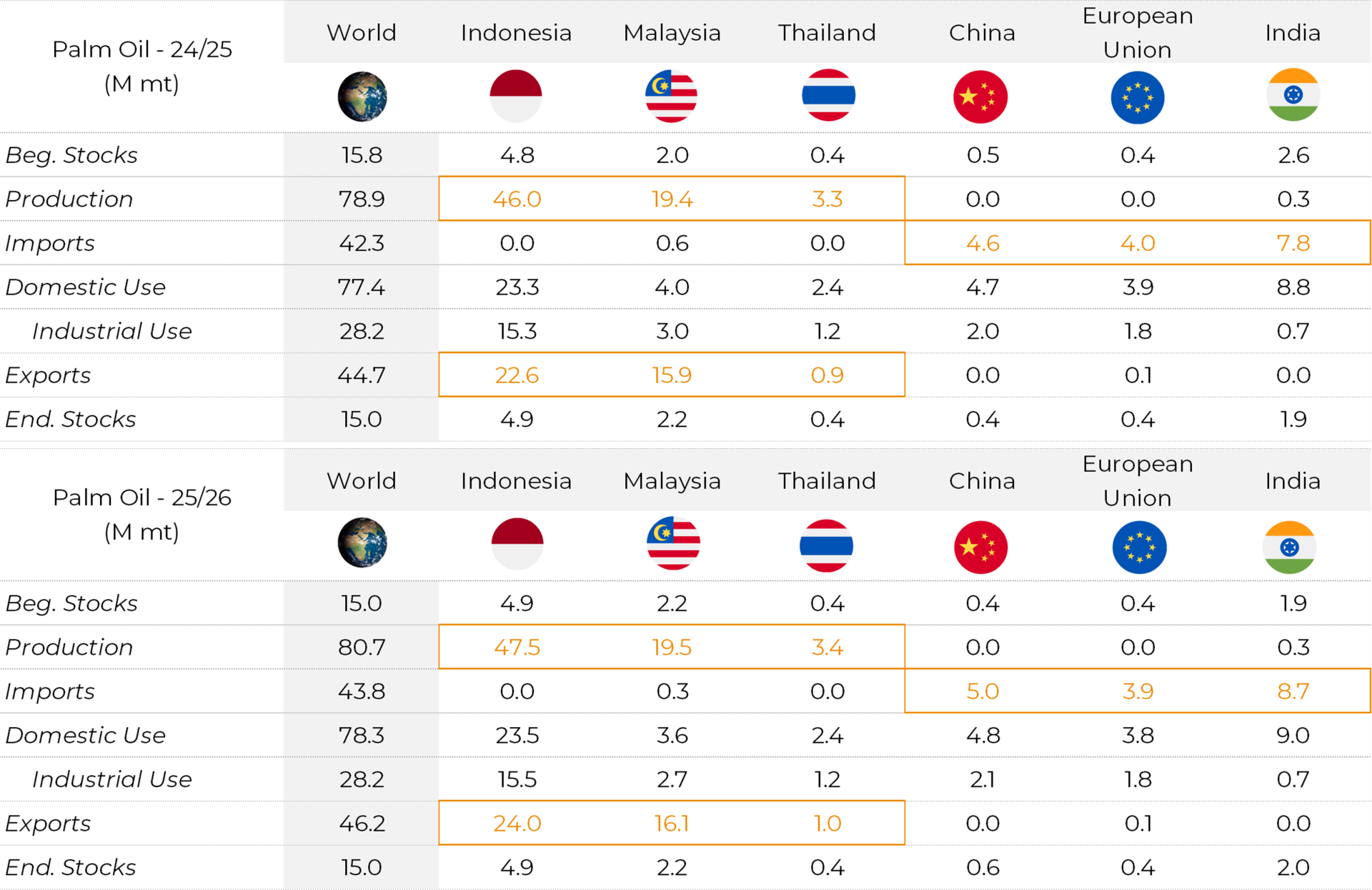

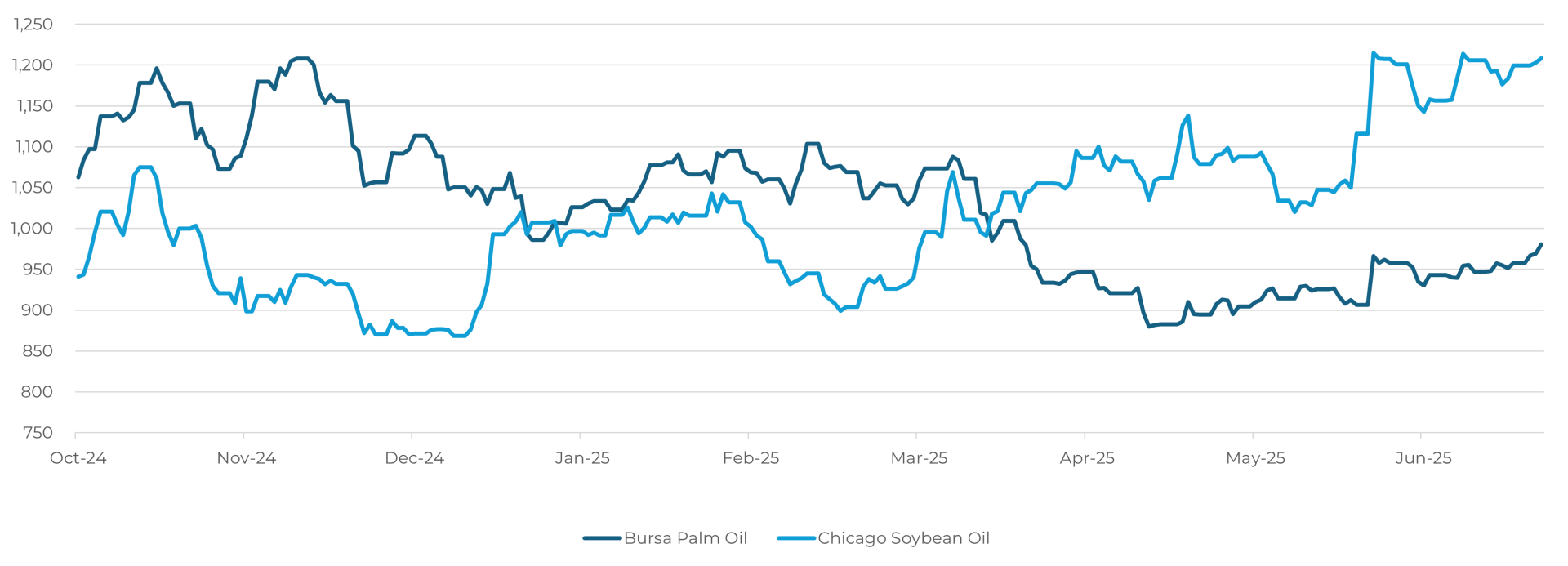

The 2025/26 season points to growth in production and exports in the two main global producers, Indonesia and Malaysia. The big news is in India, the world's largest importer of palm oil, which has reduced import taxes and is expected to increase its purchases from 7.8 to 8.7 million tons in 2025/26.

The spread between palm oil and soybean oil prices is tending to narrow, with room for the palm by-product's prices to appreciate. Global demand for vegetable oils is expected to grow, with India's recovery as a consumption vector standing out.

• EPA proposal with a direct impact on soybean oil and crushing.

• Oil share at high levels and incentive to crush in the US.

• Tight soybean and oil stocks in the US.

• Sustained Brazilian premiums in the second half of the year.

• Reduced taxes on vegetable oils in India and a probable increase in Indian imports of palm oil.

• Favorable weather in the US and expectations of a full crop.

• High soybean stocks in China.

• Growing competition between Argentina, the US and Brazil in the meal market.

• Absence of a definitive agreement between China and the US.

• Abundant supply of soybeans in South America and Brazil's great production potential in 2025/26.

The soybean complex enters the second half of 2025 with opposing forces acting simultaneously. While soybean oil has positive fundamentals, especially in the US, soybean meal is under structural pressure from oversupply. Soybean is in the middle of the battlefield, influenced by weather, premiums and the trade uncertainties between China and the US.

Monitoring the unfolding of the EPA, the weather situation in the US and China's purchasing strategy will be key to repositioning trading and hedging strategies over the coming months.

To watch the full July Call on the soybean and vegetable oil markets, click on the link below: