The global macroeconomic backdrop continues to be dominated by expectations surrounding US monetary policy. The Federal Reserve is signaling the possibility of interest rate cuts starting in September, a move that would have a direct impact on currency flows. The prospect of a fall in the US rate tends to strengthen emerging currencies, especially the real, by widening the interest rate differential. The real has been on an upward trend since the beginning of the year, a trend that could gain intensity in the coming months.

However, there are additional risk factors for Brazil. The 2026 electoral process is already starting to be priced in, and historically, the approach of the electoral calendar tends to generate greater exchange rate volatility, especially in the last quarter of the previous year. In addition, global trade tensions - especially protectionist measures and ongoing retaliation between the US and China - maintain relevant uncertainties for international commodity flows. In this context, the grain market operates under the strong influence not only of agricultural fundamentals, but also of the macroeconomic environment.

The 2025/26 cycle begins with expectations of a robust supply. World production is expected to grow by more than 60 million tons regarding the previous cycle, driven by the USA. However, demand is also advancing significantly, sustained by consumption for feed and growth in industrial use, mainly for ethanol. The global picture signals an abundance of supply, but with important nuances: any climatic mismatch in South America or unexpected increase in Chinese demand could alter the balance.

• Ending stocks projected to fall, reflecting stable production and growth in consumption.

• Pig farming margins at low levels, which limits incentives for an immediate increase in feed use. Despite this, the herd remains high and stable.

• If the Chinese government chooses to replenish strategic stocks (around 190-200 M tons), there is room for additional imports, creating a window of opportunity for Brazil and Argentina, as occurred in 2023/24, when Brazil exported more than 20 M tons to the country.

• In the short term, American corn tends to continue to be more competitive, which could have an impact on Brazil's exports.

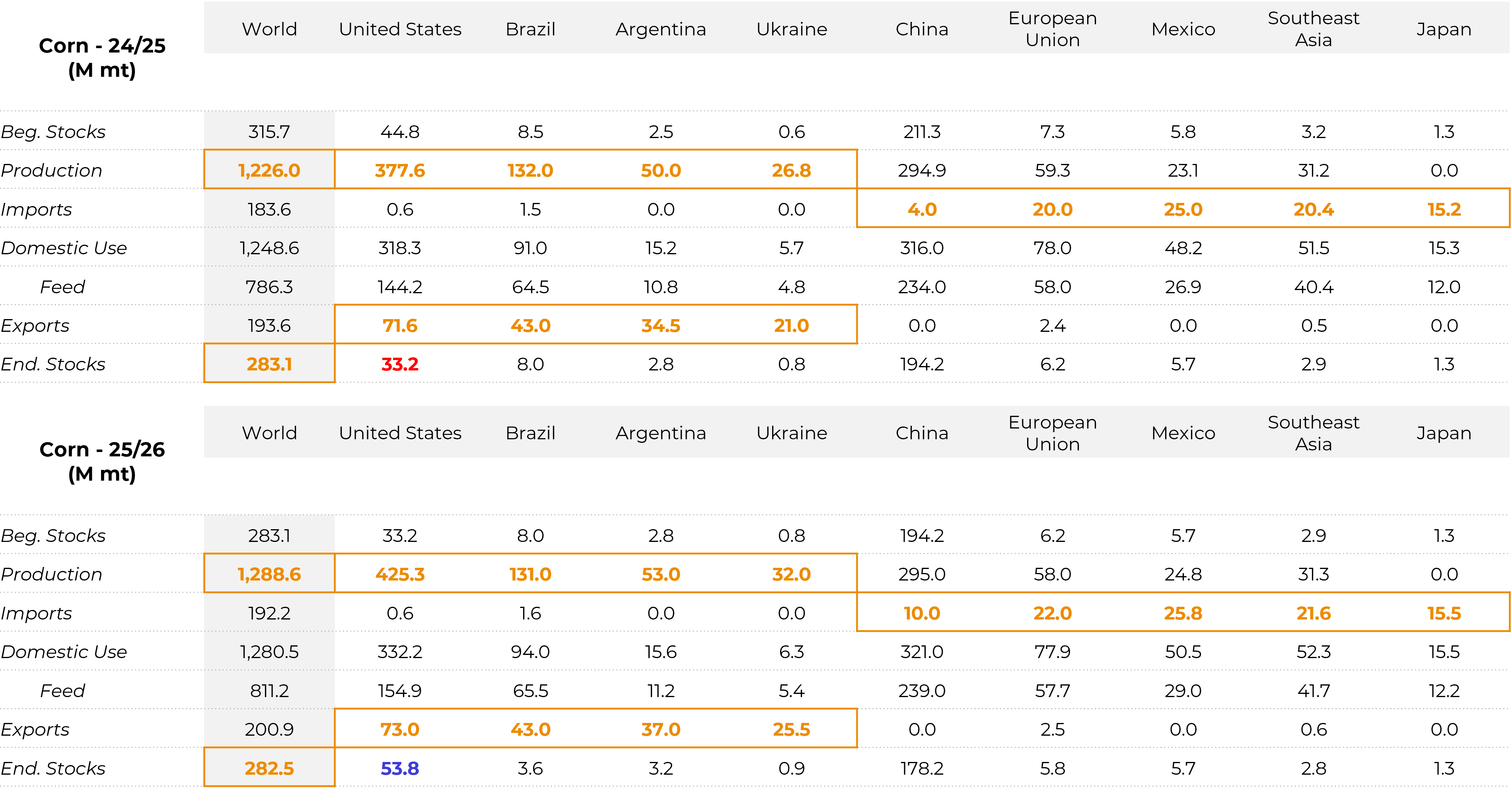

• The USDA surprised the market in August by projecting a record crop of 425 M tons, well above average expectations (406-407 M tons). This is the largest crop ever recorded in the country.

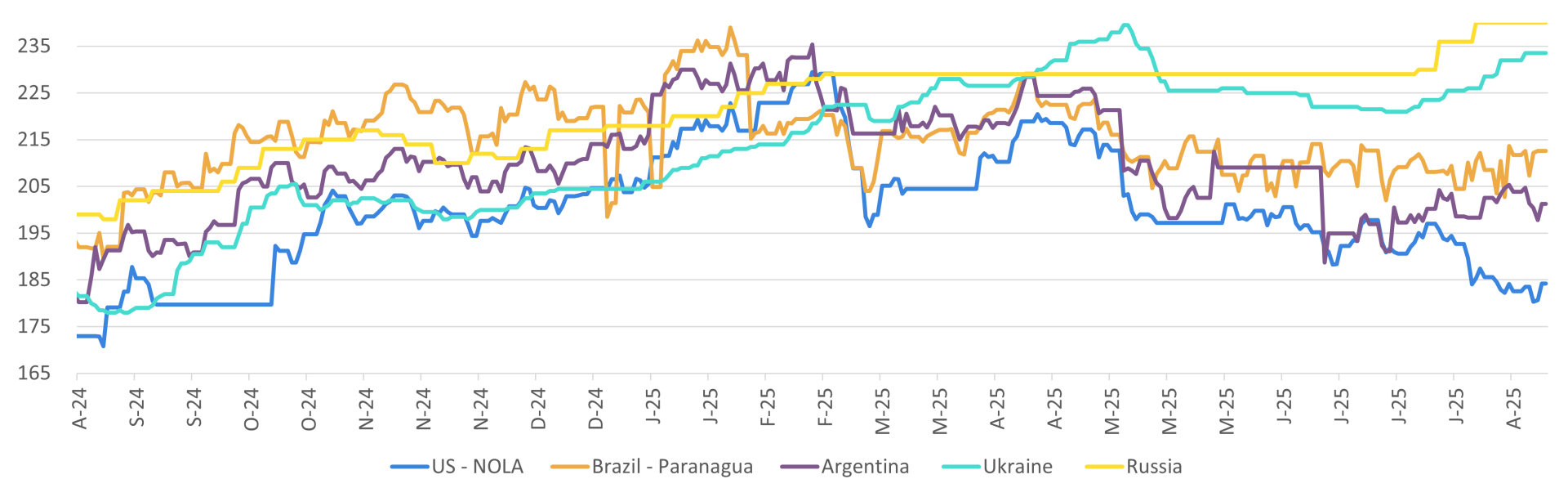

• Stocks are expected to rise from 33 M tons to 53 M tons, increasing the pressure on contracts in Chicago, which have already broken through the floor of US$ 4.30/bu, working close to US$ 4.00/bu.

• Exports are coming in at a strong pace: more than 18 M tons have already been sold for 2025/26, practically double the previous year at this time.

• The weather has been favorable throughout the crop's development, with vegetative indices (NDVI) above the historical average and good conditions for the start of the harvest.

• Risk: possible yield revisions by the USDA in September/October could partially reduce the estimate, adjusting stocks downwards. Even so, the picture remains comfortable.

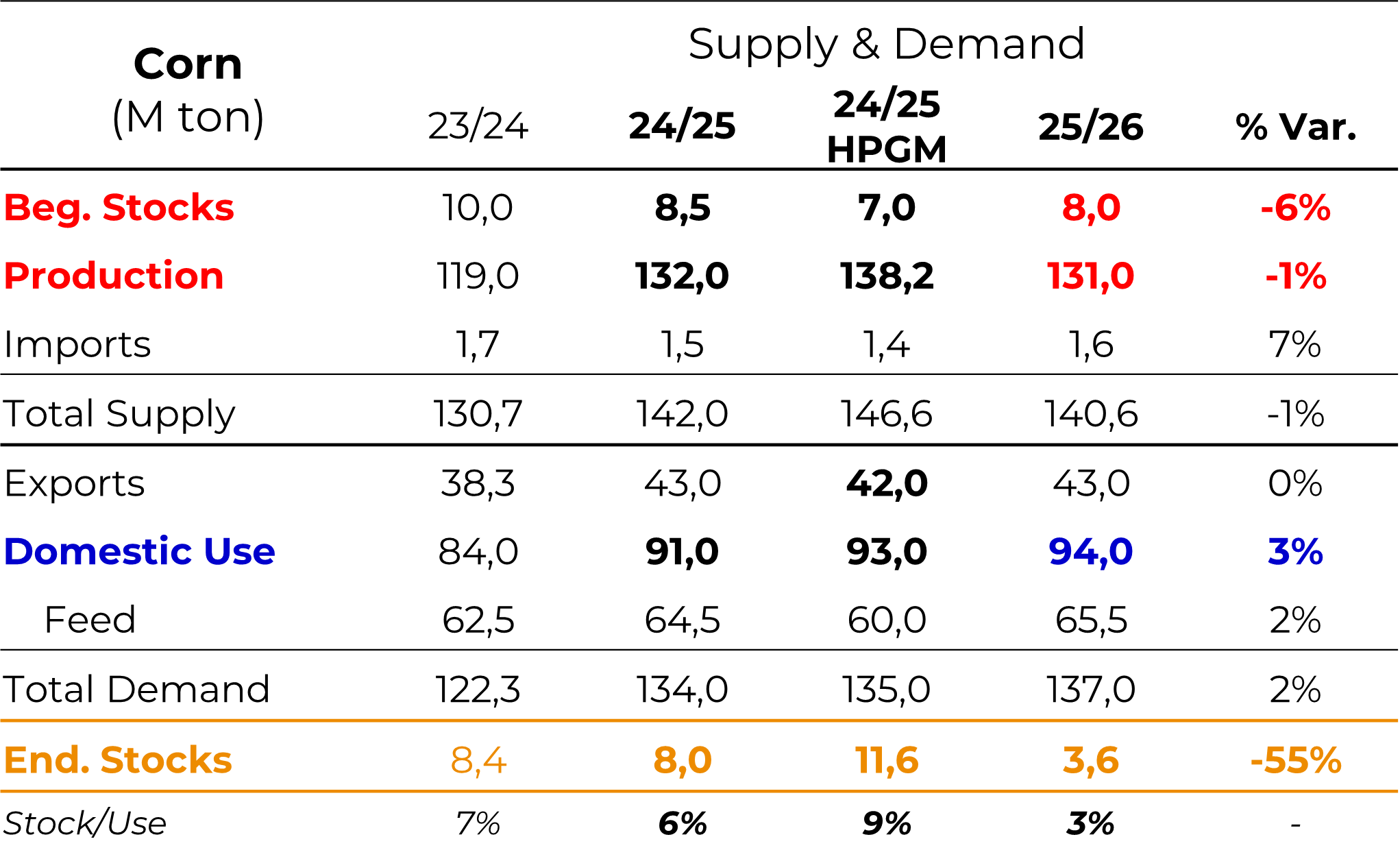

• Hedgepoint revised the total 24/25 crop to 138.2 M tons, up from the June estimate (+3.7 M tons) and the USDA (132 M tons). The figure reflects record yields in several regions of the Midwest.

• Ending stocks projected at 11.6 M tons, looser regarding the previous cycle.

• Domestic consumption is expanding, driven by corn ethanol. In the 2024/25 season, around 24 M tons should be used to produce ethanol, and this volume could double in a few years with the entry of new plants.

• Exports are estimated at 42 M tons, but there is a risk of a reduction given the strong competitiveness of American corn.

• Marketing of the 2nd crop remains slow (43% vs. 50% of the historical average), with producers holding back part of the volume in the expectation of better prices.

• Domestic prices (Campinas) around R$64-65/sc, pressured by ample supply.

• On the international market, Brazil will also have to compete with Argentina, which is expected to increase exports in the next cycle.

• Current production estimated at 50 M tons, with the possibility of an increase for 2025/26, given that corn margins exceed those of soybean. The area is expected to grow.

• Unified exchange rate by the Milei government has reduced distortions and increased predictability, encouraging early marketing: producers have already sold around 5% of the new crop (vs. 1% in the same period last year).

• Exports are expected to grow, competing directly with Brazilian corn in the second half of the year.

• Relevant climate risk: NOAA projects a 60% chance of La Niña in 2025, which could bring drought to Argentina and southern Brazil, affecting yields.

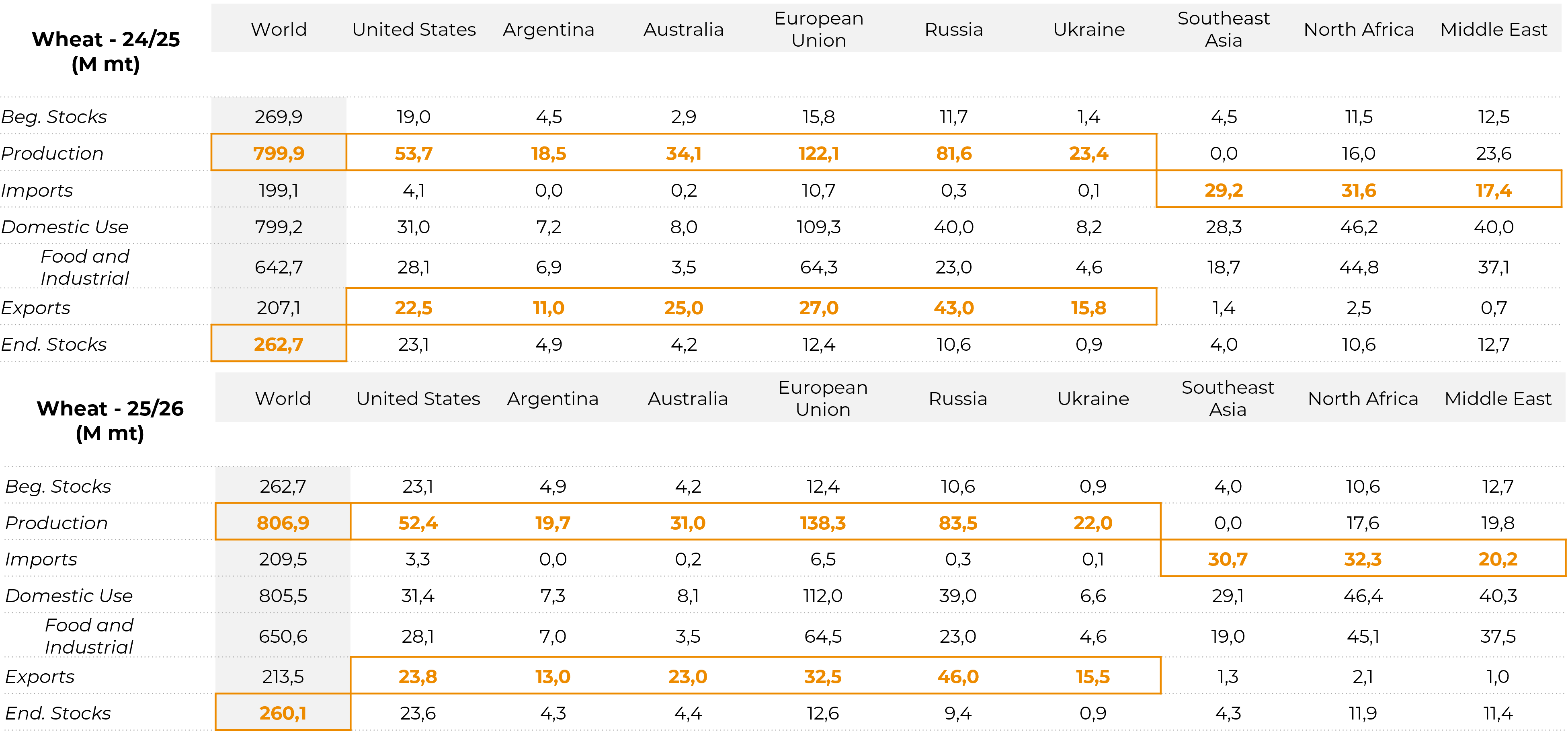

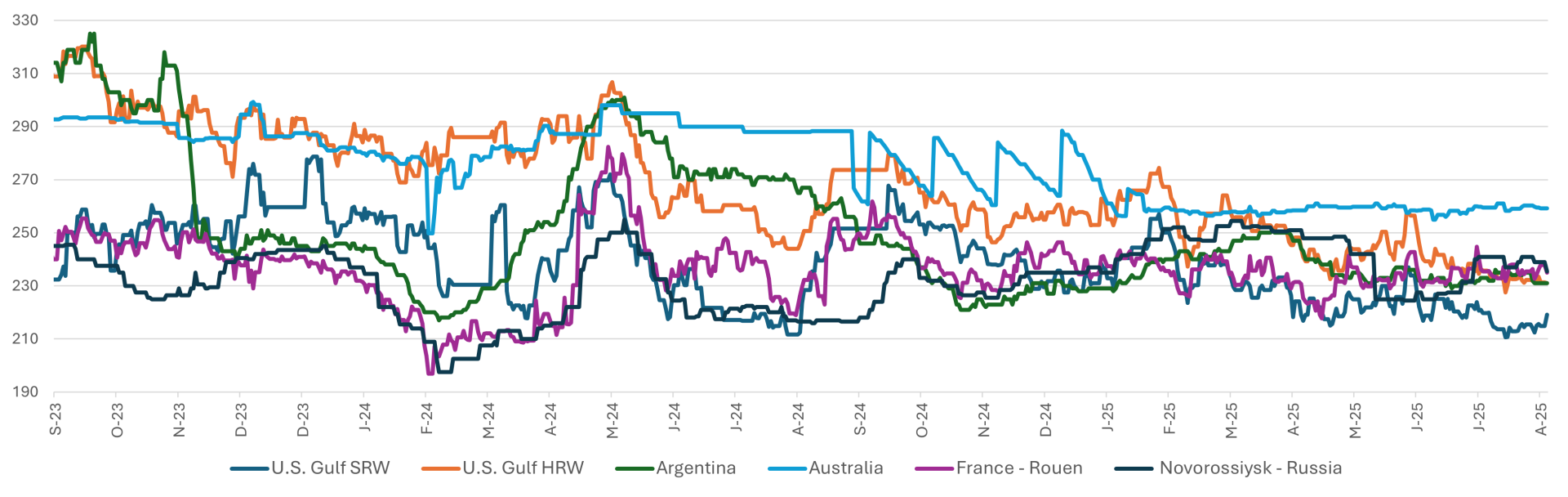

The global wheat market in 2025/26 presents a picture of ample supply. Production tends to exceed that of the previous year, mainly driven by the European Union and Russia, while Ukraine continues to be limited by the war. Global stocks, however, are not growing at the same pace and should remain close to 2024/25 levels, suggesting balance but still with downward pressure due to abundant supply.

• Production slightly down on last year's crop, due to the smaller area, but sustained by good yields.

• Exports may increase slightly (up to 24 M tons), while stocks remain high.

• Chicago remains under pressure, reflecting the weight of ample global availability and strong international competition.

• Crop estimated at 138 M tons, against 122 M tons in the previous cycle.

• Imports are expected to fall from 11 M tons to around 6 M tons, while exports are expected to increase.

• The gain in European competitiveness is also putting pressure on Ukrainian exports, which are already suffering from logistical restrictions and taxes re-established by the EU.

• Projected production close to 20 M tons, with exports on the rise.

• In Brazil, the wheat area continues to be limited by unattractive margins, especially in the south (RS and PR), maintaining dependence on Argentine wheat imports.

• Production estimated at 20-23 M tons, well below pre-war levels (33 M tons).

• In addition to logistical restrictions, the return of import taxes in the EU reduces Ukrainian wheat's access to the European market.

• Exports should fall again.

• Production is expanding, with exports favored by the (almost total) removal of export taxes.

• Despite occasional weather problems during the crop's development, harvests indicate above-average yields, consolidating Russia as the world's largest exporter.

• Potential increase in corn imports by China, should the government decide to rebuild strategic stocks.

• Continued growth in demand for corn for ethanol in Brazil, adding a new layer of structural consumption.

• Risk of La Niña returning.

• Possibility of downward revisions to American corn yields.

• Possible diplomatic advances that end or reduce trade conflicts, especially involving China.

• Record crop of corn in the US, with high stocks and exports at a fast pace.

• Expansion of wheat supplies in the European Union, Russia and Argentina.

• Seasonal harvest pressure in the US (corn and wheat) and Brazil (corn).

• Argentine producers encouraged to sell earlier, increasing competition.

• Speculative funds heavily sold in corn and wheat, reinforcing the short-term bearish trend.

The grain market enters the 2025/26 cycle under strong influence from the abundance of global supply, especially corn in the US and wheat in the European Union and Russia. The predominant bias is downwards, with prices under pressure in Chicago and an impact on international benchmarks.

However, upside risks remain on the radar: China's greater share of imports, the effects of a possible La Niña and adjustments to US crop estimates could reverse some of the pressure. For Brazil, domestic consumption of corn for ethanol is emerging as a new structural demand vector, reducing dependence on exports in the medium term.

In summary, the base scenario points to pressured prices in the short term, but the extent of weather and political uncertainties requires constant monitoring, with the market highly sensitive to any sign of change in the global supply and demand picture.

To watch the full August Call on the Corn and Wheat markets, click on this

link.