Market Call - Soy Complex and Vegetable Oils - Highlights

Soybean Complex and Vegetable Oils Scenarios Update

Macro Overview

Macro Overview

Soybean Complex

Global Scenario

Soybean Complex

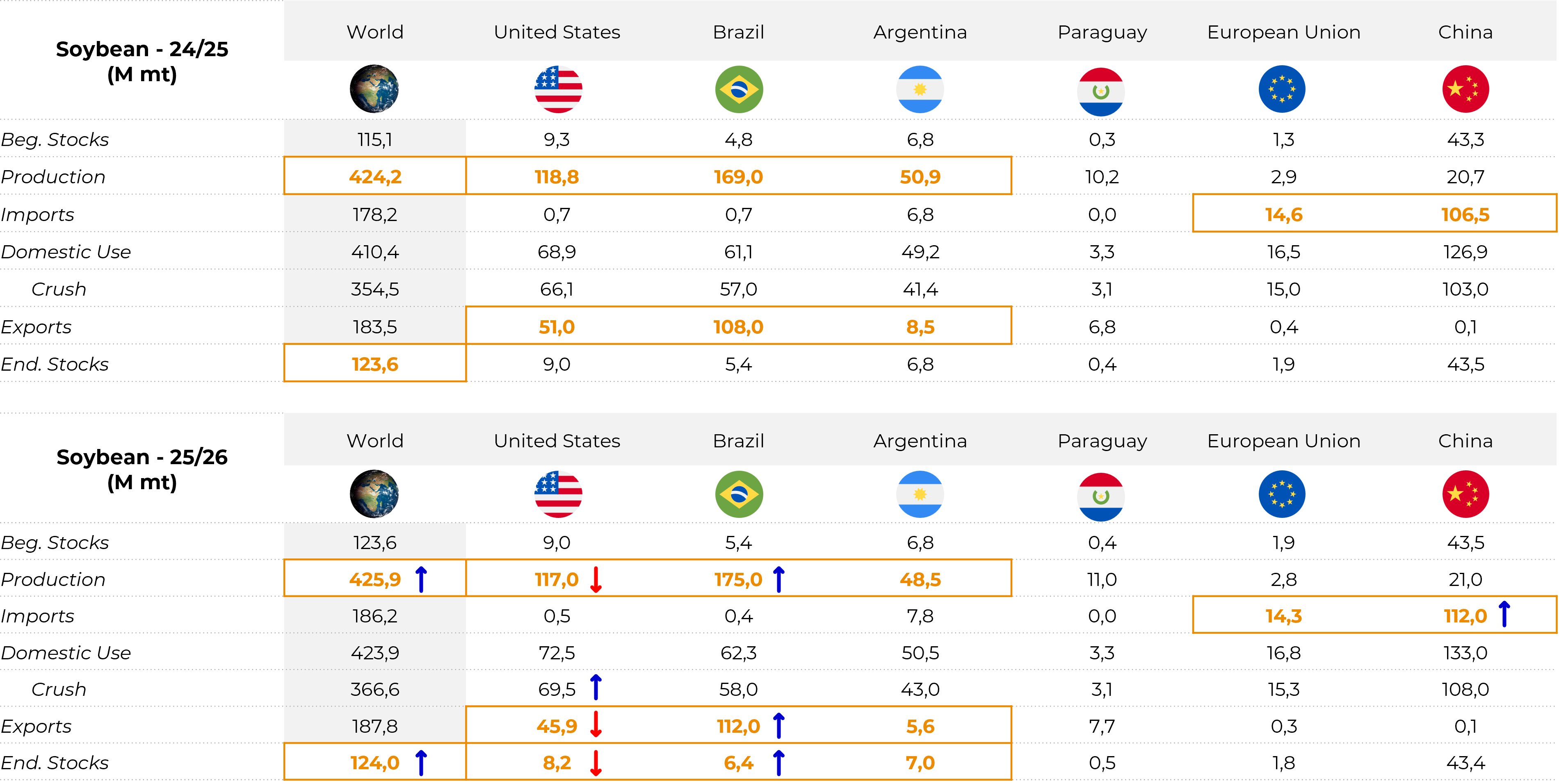

Soybean - World - Supply and Demand (M ton)

Source: USDA, Hedgepoint

China

China

- China maintains a comfortable position regarding supply security, with high stocks and adjusted crushing margins.

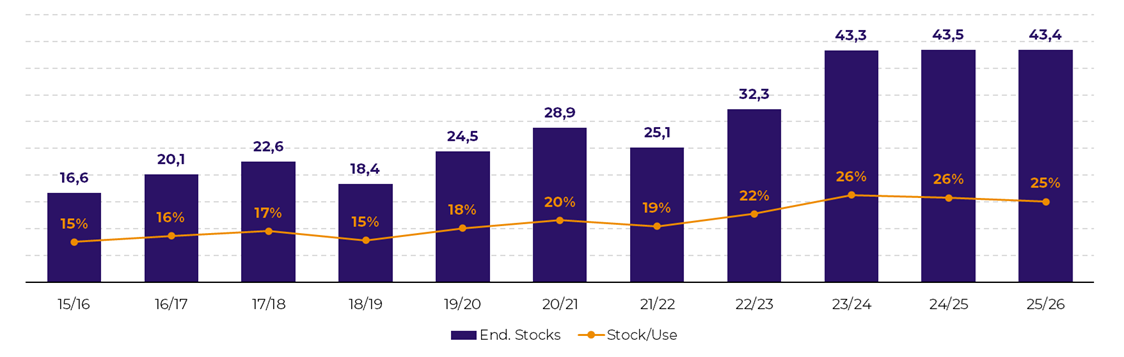

- Stocks: around 43-44 M tons, enough to cover almost three months of domestic consumption. This level reduces the urgency of purchases in the short term and allows for greater selectivity when originating soybean.

- Imports:

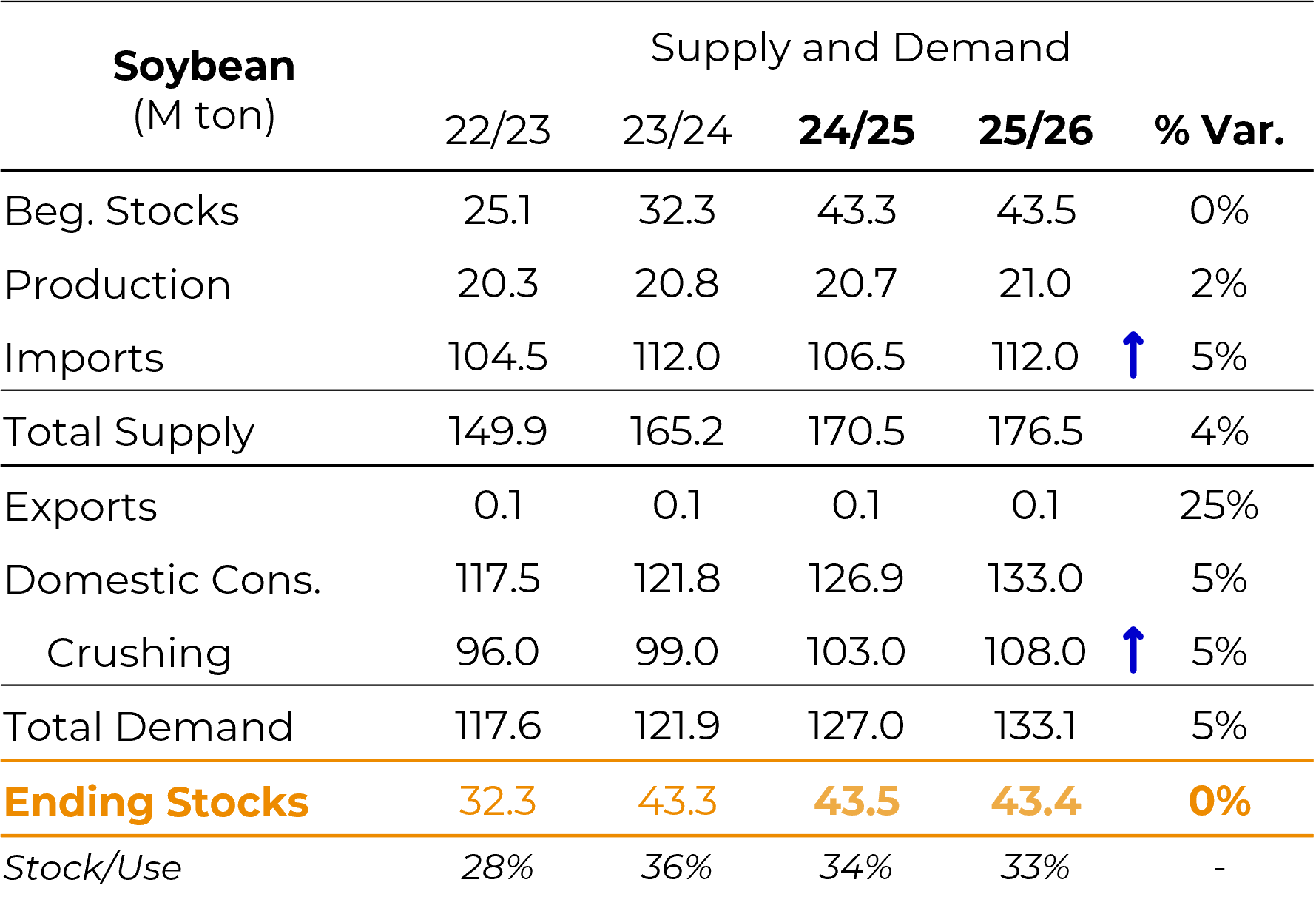

Season 2024/25: estimated at 106.5 M tons, below initial projections and down regarding the previous season.

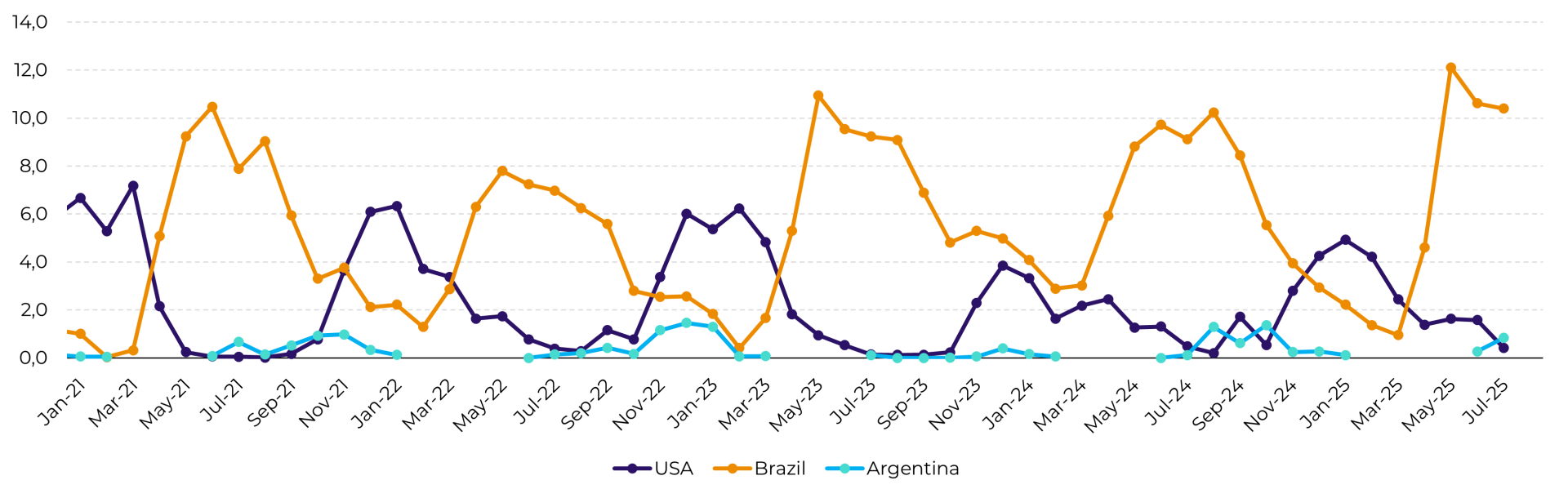

Season 2025/26: estimated at 112 M tons, supported by crushing and high stocks. - Origin of purchases: Brazil continues to be the dominant supplier, benefiting from its large availability. The US is losing ground due to tariffs, while Argentina is temporarily expanding its presence, taking advantage of the recent export tax cut.

- Prices: Currently, Brazilian soybeans are the least competitive among the three origins due to higher premiums. The US has the most competitive price but remains off the Chinese radar due to trade barriers. Argentina is gaining relevance as an alternative, offering the second most competitive price at the moment.

- Crushing: Activity should reach 103 M tons in 2024/25 and grow to 108 M tons in 2025/26, although the profitability of the industries continues to be pressured by narrower margins.

- Outlook: Chinese demand remains solid, but the strategy is to make gradual purchases, in volumes that avoid unnecessary pressure on international prices.

China Soybean - Stocks and Stock/Use (M ton, %)

Source: USDA, Hedgepoint

Soybean - China - Supply and Demand (M ton)

Source: USDA, Hedgepoint

Soybean – China Monthly Imports (M ton)

Source: China Customs, Bloomberg

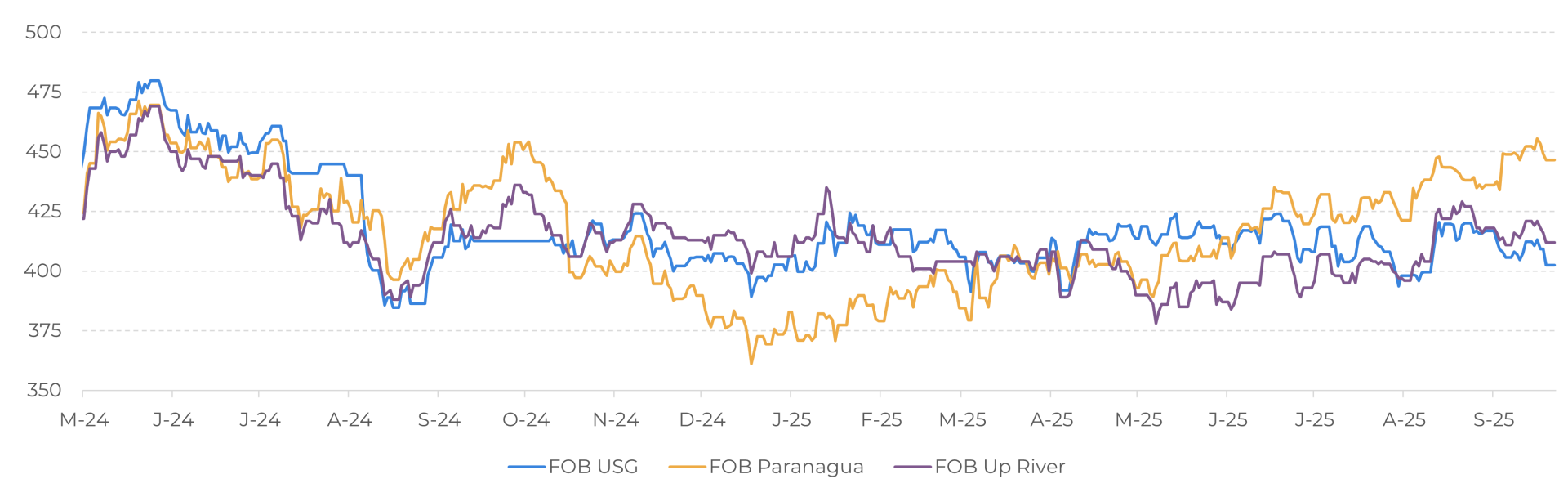

Soybean - FOB Prices - Main Origins - in USD/ton

Source: LSEG, Hedgepoint

USA

USA

- The American market is going through a time of transition and uncertainty, with a large crop (but lower than last season), weakened exports and expectations placed on energy policy.

- Crop 2025/26: estimated at 117 M tons, down on the previous season. The result reflects a strong reduction in planted area, partially offset by a likely record yield.

- Harvest: the harvest is progressing at a normal pace, within the average of recent crops. The weather should be favorable for machine progress in the coming weeks, with no major potential problems.

- Crop conditions: worsening, with approximately 61% in good/excellent condition at the moment, down on the previous week and on the same period last year. Despite favorable weather during most of the development, it is still possible to see yield and production cuts in the next USDA reports due to the recent worsening of conditions.

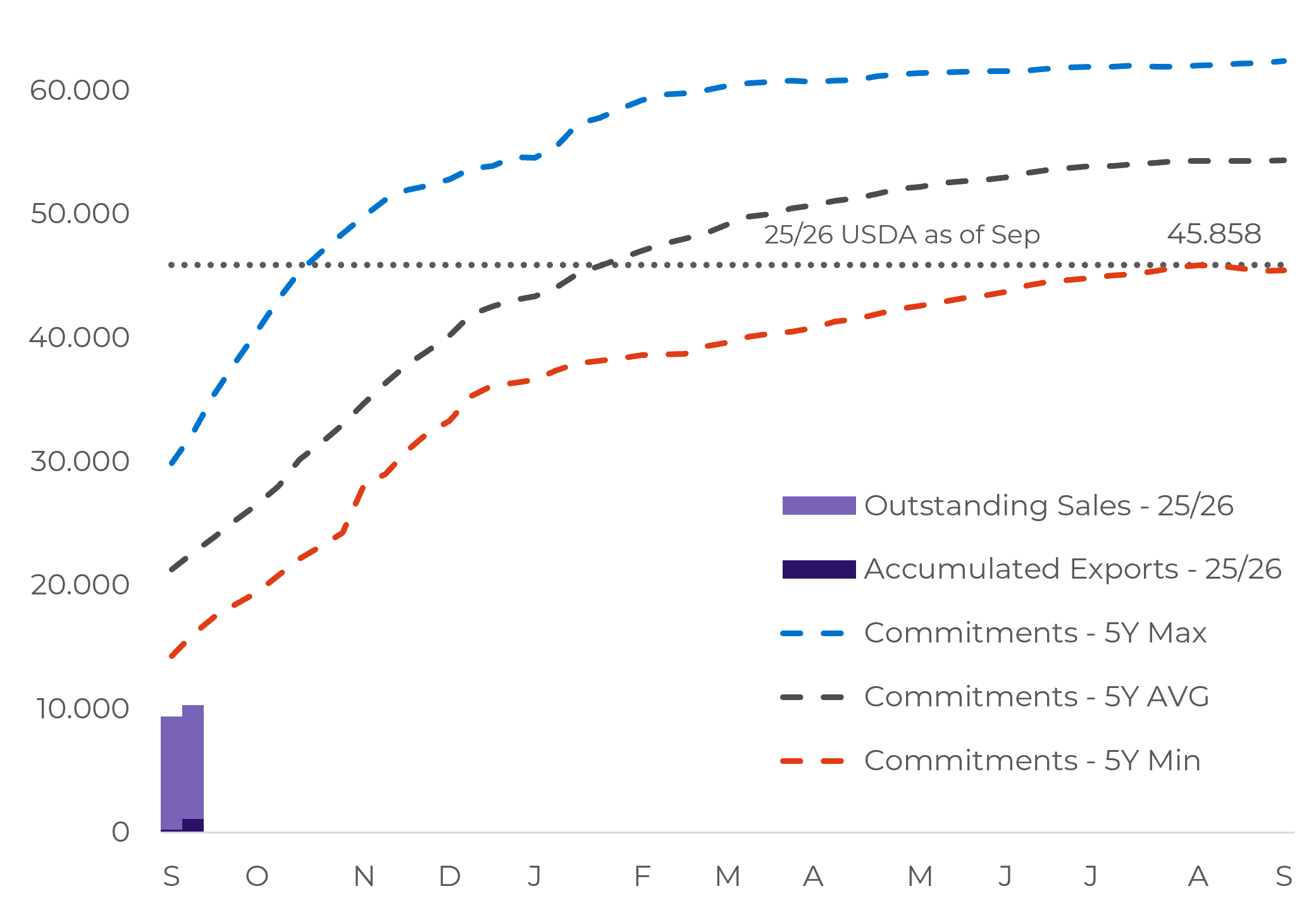

- Exports: continue at a slow pace. Only 10.3 M tons have been registered so far, compared to almost 16 M tons in the same period of the previous cycle. China's absence from US soybean purchases remains the main obstacle to a recovery in the flow.

- Crush and EPA: Domestic demand for soybean oil is the point of support. The Environmental Protection Agency's (EPA) proposal to raise the mandatory blend of biofuels (biodiesel and renewable diesel) by 67% could add up to 4.5 M tons to the currently estimated crush, bringing soybean stocks to lower levels.

- Oil Share: remains at very high levels, around 50%, ensuring positive margins for processors, even though soybean meal remains under pressure.

- Prices in Chicago: oscillating between US$ 10.00 and 10.60/bu, pressured by the US harvest, the absence of Chinese purchases and a possible record crop in Brazil. A potential "bullish" trigger for the market in the short term could be the definition of the EPA proposal.

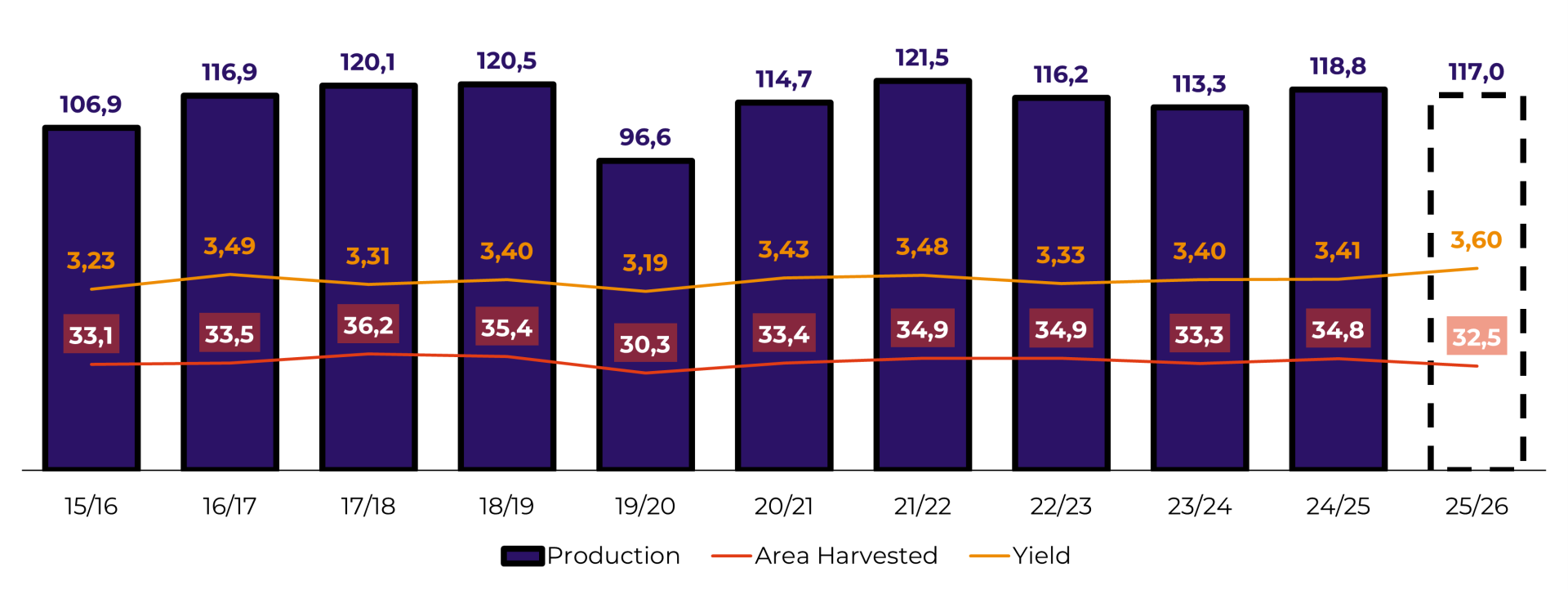

USA Soybean - Production (M ton), Harvested Area (M ha) and Yield (ton/ha)

Source: USDA, Hedgepoint

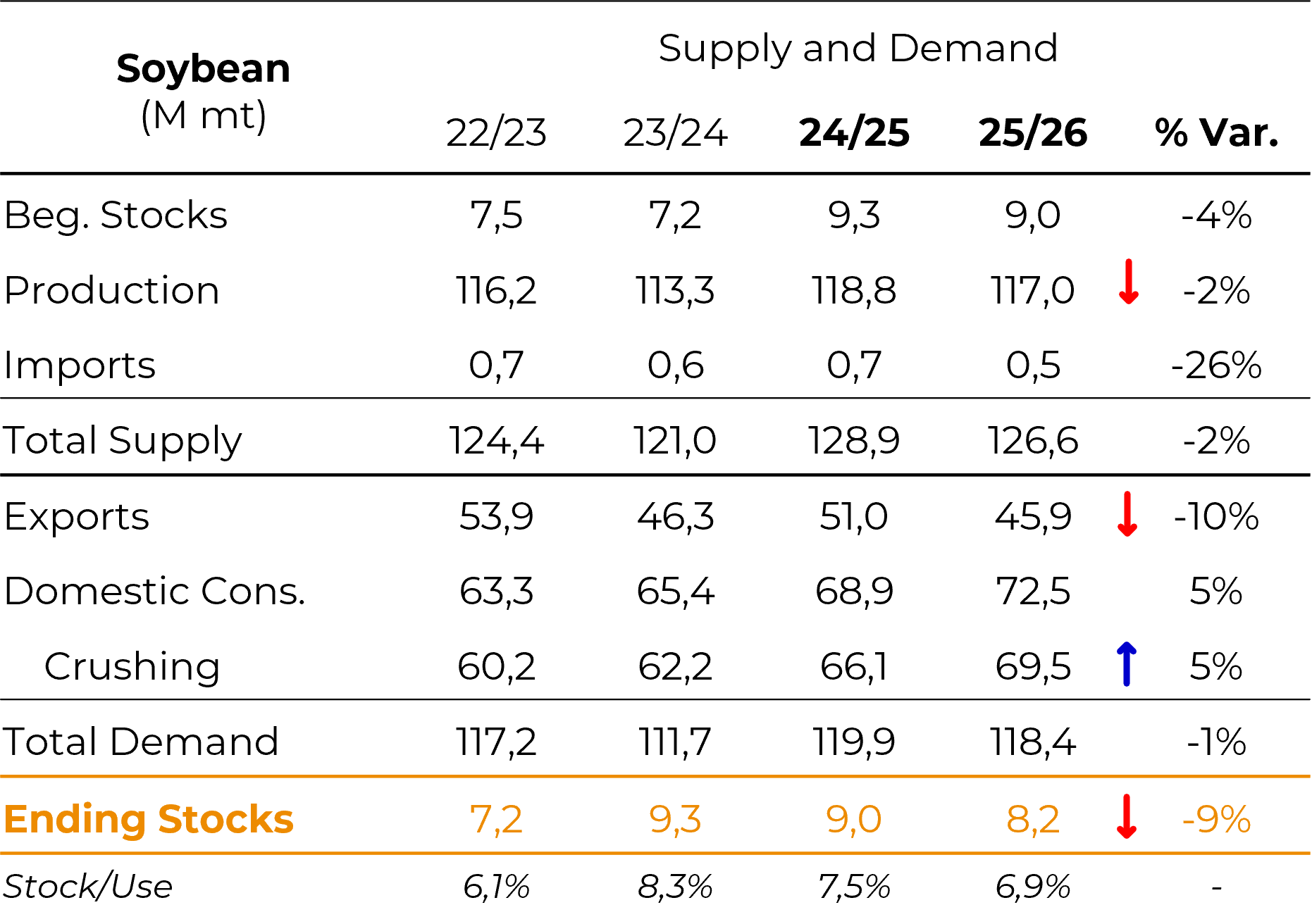

Soybean - USA - Supply and Demand (M ton)

Source: USDA, Hedgepoint

USA Soybean - Export Sales - Current Crop (M ton)

Source: USDA, Hedgepoint

Brazil

Brazil

- Brazil is consolidating its position as the main global origin but faces growing challenges in terms of margins and farmer sales.

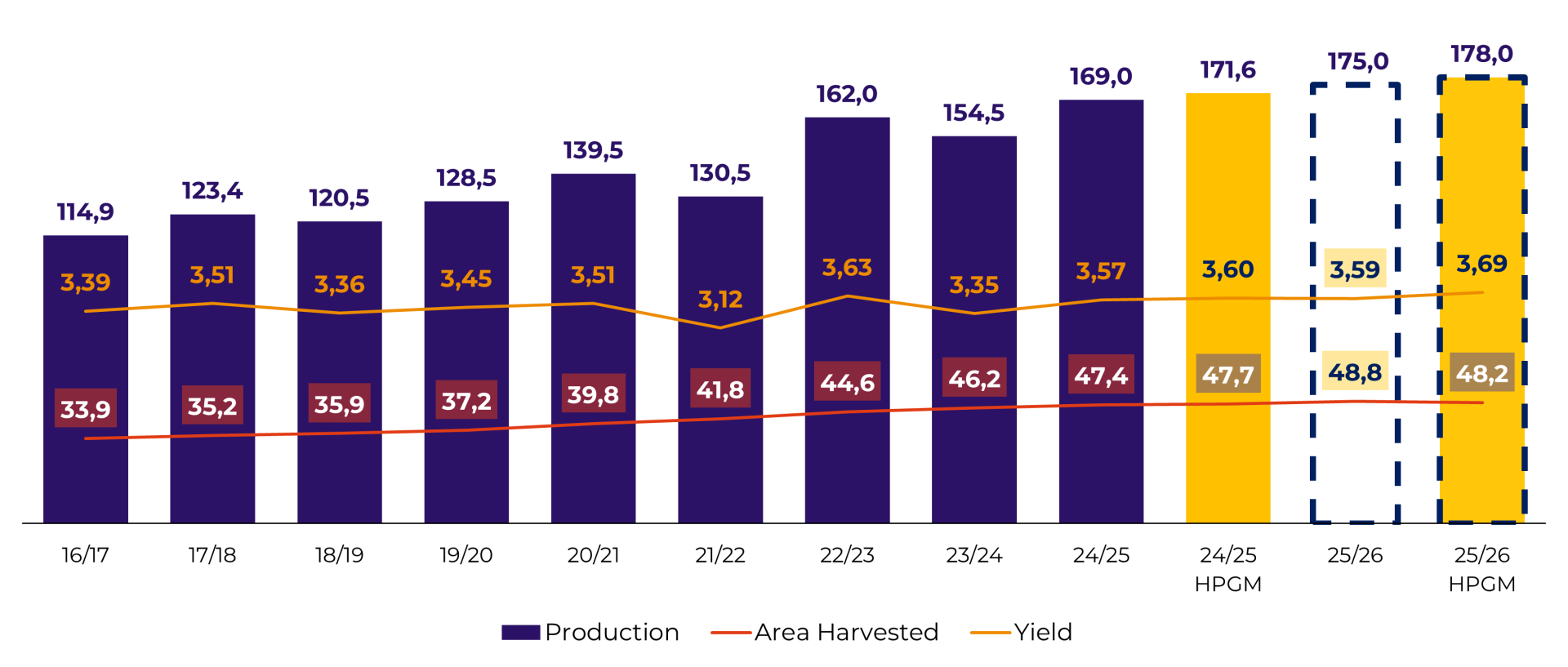

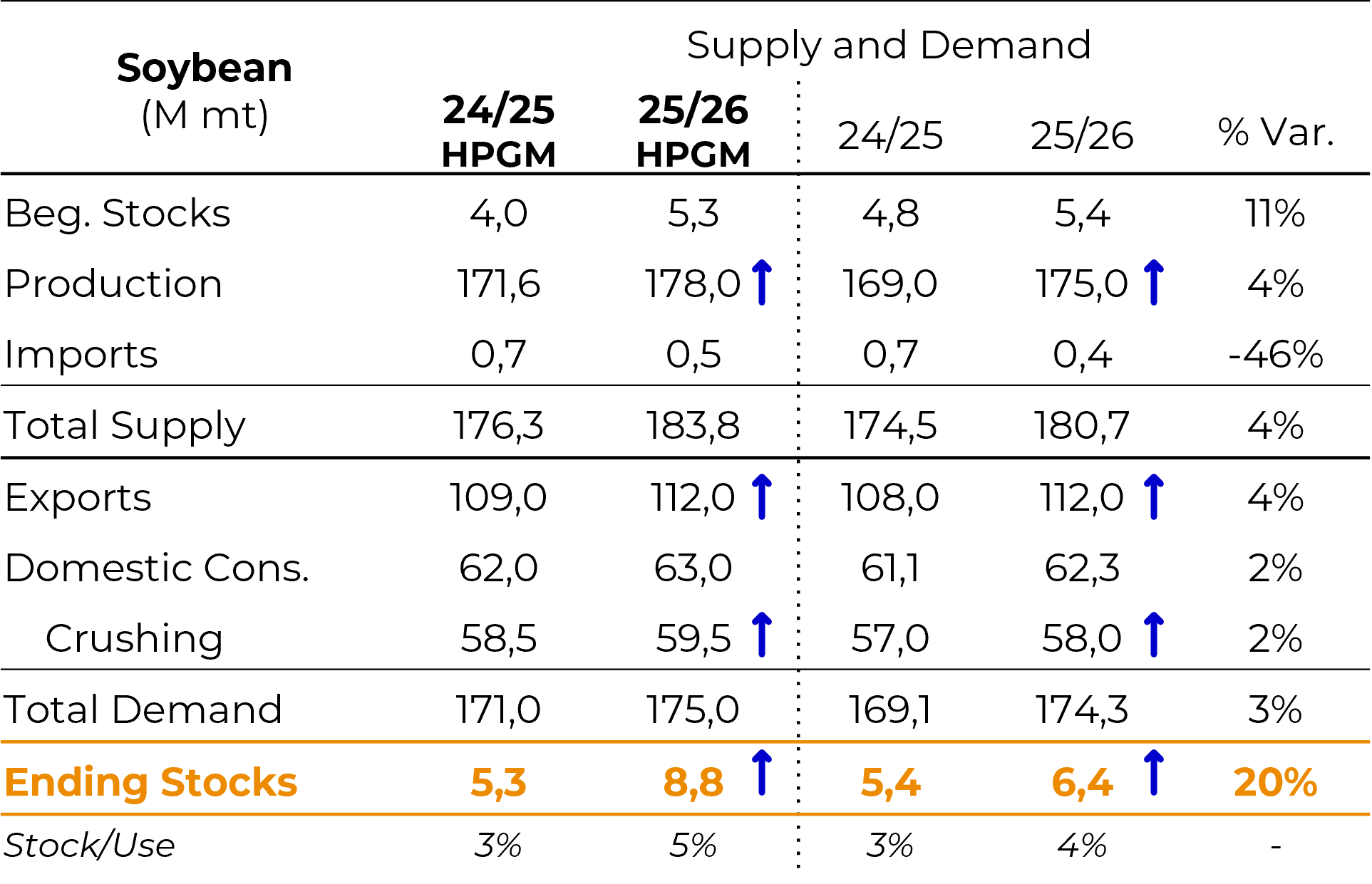

- Crop 2024/25: production revised to 171.6 M tons due to the high yields recorded in several states in the central belt of the country.

- Crop 2025/26: Hedgepoint's initial projection points to a production of 178 M tons, which could represent a new record crop. Attention is focused on the possible effects of La Niña in the south of the country.

- Exports:

Total crop 2024/25 estimated at 109 M ton, supported mainly by increased Chinese demand due to the trade war. Current export line-up reinforces sentiment.

For 2025/26, the estimate points to a new record: 112 M tons. However, a possible trade agreement between the US and China could still impact this projection - Crushing: should reach 58.5 M tons in 2024/25, maintaining an expansion trend in 2025/26 supported by greater demand for soybean oil for biodiesel.

- Crushing margins: have currently fallen to their lowest levels in recent years, which could reduce the domestic industry's appetite in October, November and December.

- Biofuels policy: the B15 blend came into effect in August, with a positive impact on soybean oil demand. We believe there is little room for further progress in 2026 due to the election year.

- Farmer Sales: Around 16% of the old crop is still available and approximately 20% of the new crop has been sold, reflecting a more cautious attitude on the part of producers.

- Prices: soybeans remain in the R$126/60kg bag range in the Rondonópolis/MT reference area, sustained by firm premiums.

- Planting and weather: The arrival of the rains has unlocked planting work, which despite initial delays is within the average for this time of year. La Niña should demand special attention for the south of the country this season. The weather will be a key factor from now on.

Brazil Soybean - Production (M ton), Harvested Area (M ha) and Yield (ton/ha)

Source: USDA, Hedgepoint

Soybean - Brazil - Supply and Demand

Source: USDA, Hedgepoint

Argentina

Argentina

- Argentina is regaining ground in the international market, but its competitiveness remains dependent on weather and fiscal policy.

- 2025/26 crop: estimated at 48.5 M tons, lower than the previous cycle, due to the migration of area to corn as a result of tighter soybean margins.

- Exports: gaining traction with the temporary tax cut, the so-called "retenciones". Soybean sales could exceed 10 M tons in the 2024/25 season.

At this point, we would like to point out that up until the date of our presentation (24), the tax cut was still in effect, and rumors were pointing to Chinese importers buying around 1.3 million tons of Argentine soybeans. However, the following day (25), the Argentine government announced the cancellation of the tax cut, citing that the target volume of dollars generated by exports had already been reached. On Friday (26), official figures showed the results of exports during the tax exemption period:

Argentina - Sworn Declarations of Foreign Sales - Decree 682/2025

Source: Subsecretaría de Mercados Agroalimentarios e Inserción Internacional.

- Large volumes were recorded for export, in a totally atypical move in the Argentine market. Argentine sales of the soybean complex expanded greatly during the short tax-free period, negatively impacting the market in Chicago and export premiums in Brazil. Estimates for exports of the Argentine soybean complex are expected to be positively adjusted in the next USDA reports.

- Crushing: expected to grow in 2025/26, reinforcing the country's position as the main exporter of by-products.

- Soybean Meal: exports projected at 29.7 M tons in 2025/26, consolidating world leadership in soybean by-products.

- Soybean Oil: exports are expected to reach 6.6 M tons in 2025/26.

- Weather: La Niña brings risks to production, but the current maps for October/November do not indicate major problems for the start of planting and initial development of the crop.

Palm Oil

Indonesia & Malaysia

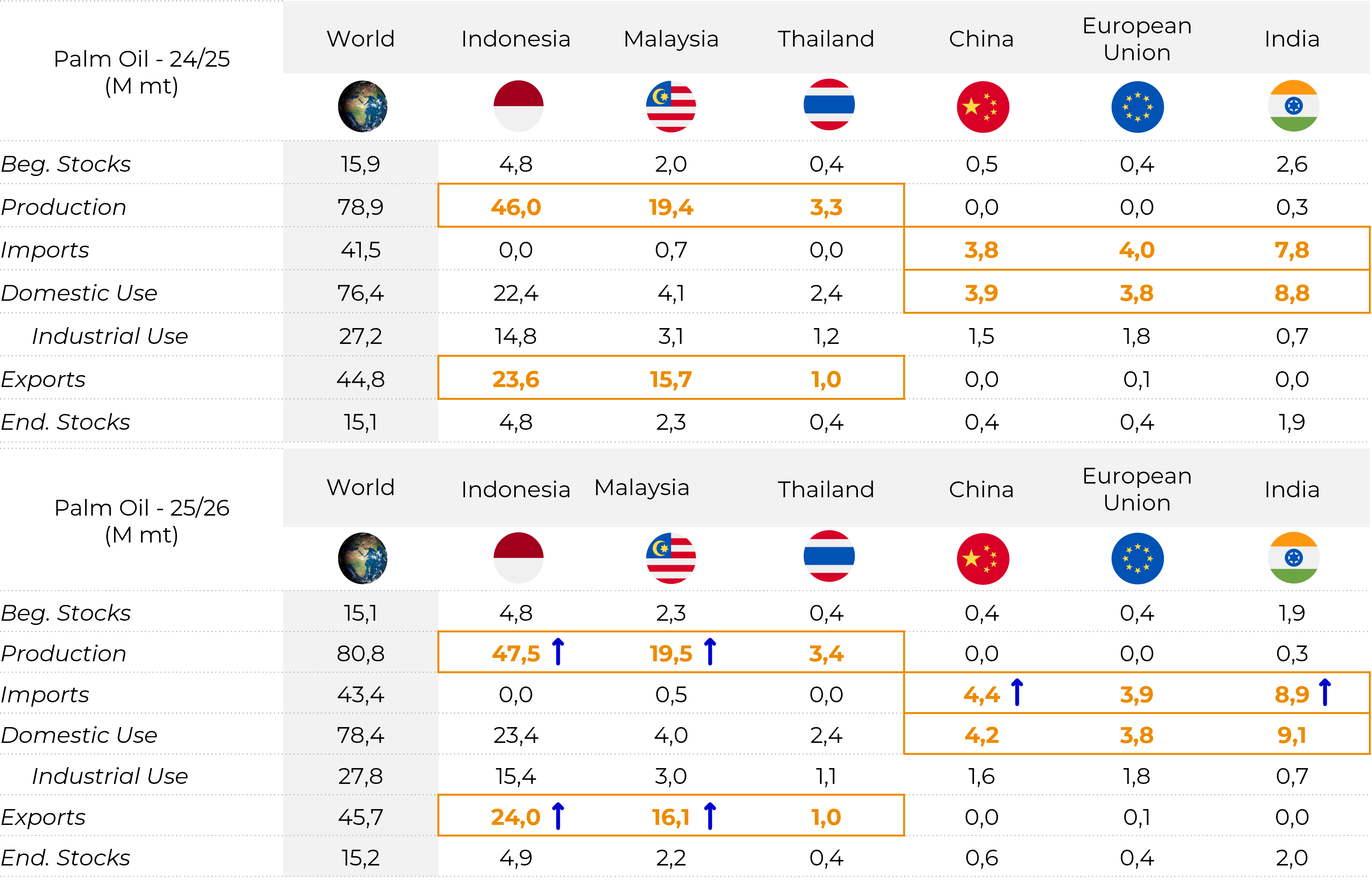

- The palm oil market is going through a phase of rebalancing, marked by growth in supply and recovery in demand.

- Production 2025/26: Indonesia is expected to produce 47.5 M tons (+3%), while Malaysia is expected to produce 19.5 M tons (+1%).

- Exports: Indonesian exports estimated at 24 M tons in 2025/26. Malaysia is expected to ship around 16 M tons.

- Demand: India, the world's main importer, is expected to increase its imports of palm oil to 8.7 M tons, favored by the recent reduction in import tariffs on vegetable oils.

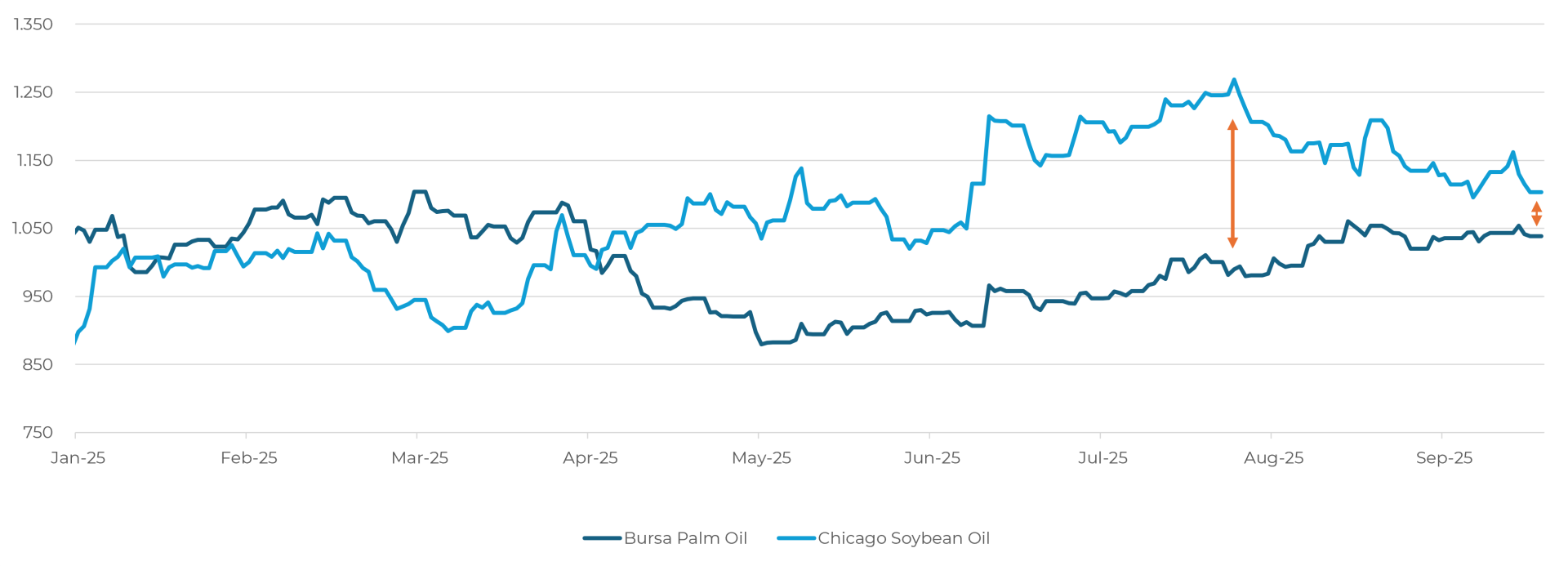

- Prices: the price differential between palm oil and soybean oil has fallen in recent months. This movement has restored competitiveness to the palm by-product and strengthened price recovery in the short term.

Palm Oil - World - Supply and Demand (M ton)

Source: USDA, Hedgepoint

Prices Comparison - Palm Oil vs Soybean Oil (USD)

Source: LSEG, Hedgepoint

Bulls and Bears

Bullish factors

- EPA proposal in the US, with potential to increase crushing and reduce stocks.

- High oil share, sustaining crushing margins.

- Relatively tight stocks in the US.

- Firm premiums in Brazilian ports due to Chinese demand.

- Recovery in Indian demand for vegetable oils.

Bearish factors

- US harvest weighs on prices in Chicago.

- China still out of the American market.

- High stocks in China, reducing the urgency of purchases.

- Competitiveness of Argentinian soybeans with temporary tax exemption.

- Potential record crop in Brazil (close to 180 M tons).

- Depressed margins in Brazilian crushing.

Final considerations

Final considerations

Link - September's Call

Written by Luiz F. Roque

Luiz.Roque@hedgepointglobal.com

Reviewed by Thais Italiani