The global macro environment is characterized by a return to volatility, driven primarily by the conflict between the United States and Iran. Although the level of volatility (as measured by indicators such as the VIX) has not yet reached historically extreme levels, there has been a significant shift from the recent period of lower risk.

In the financial sector, the structural depreciation of the dollar stands out, reflecting:

• Persistent inflation in the United States (CPI at recent record highs);

• Deteriorating growth expectations;

• Pressure on U.S. Treasury yields.

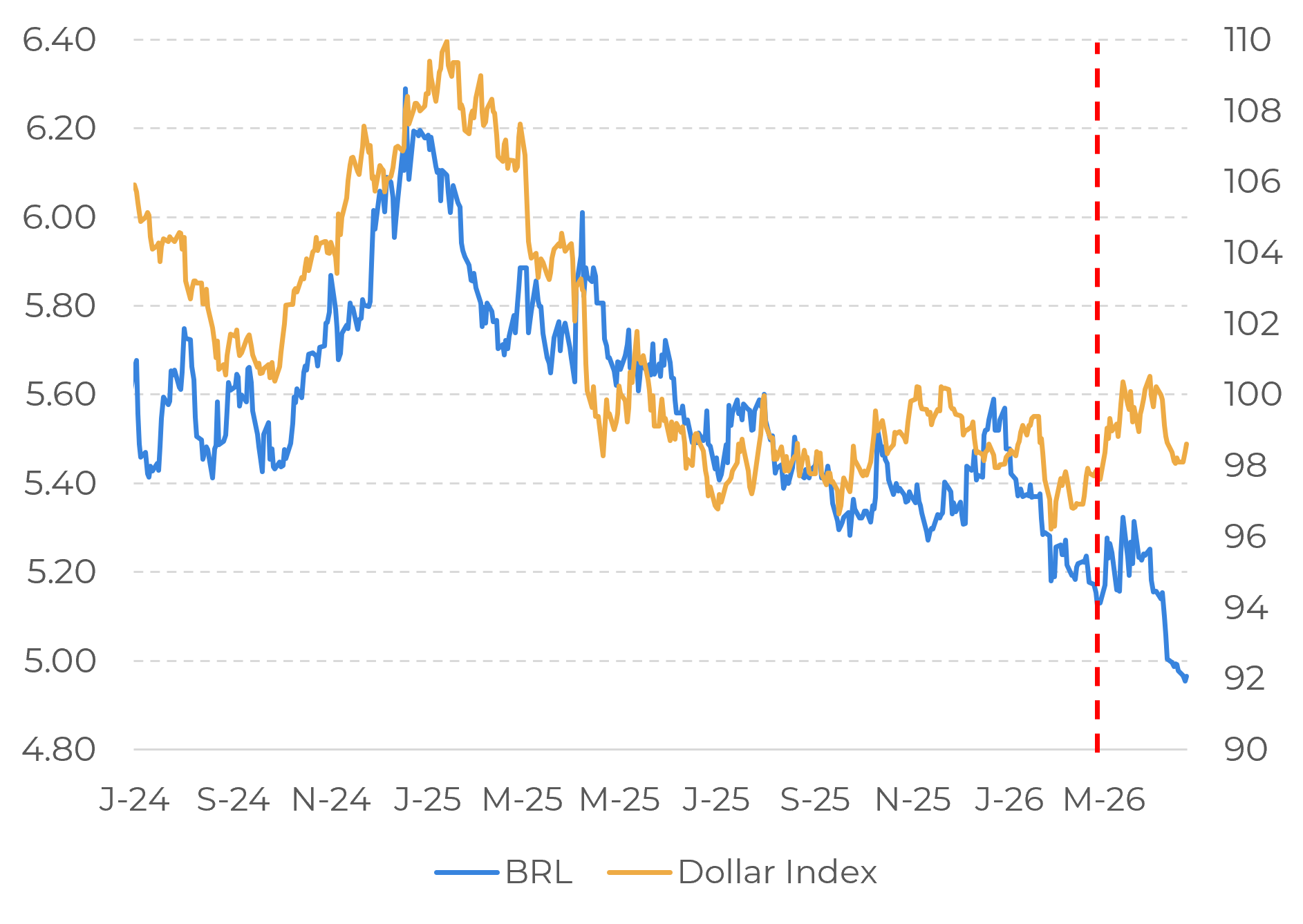

This context favors capital flows to emerging economies, particularly Brazil, which features:

• A high real interest rate differential;

• Inflow of foreign capital;

• Appreciation of the real (below R$5/USD).

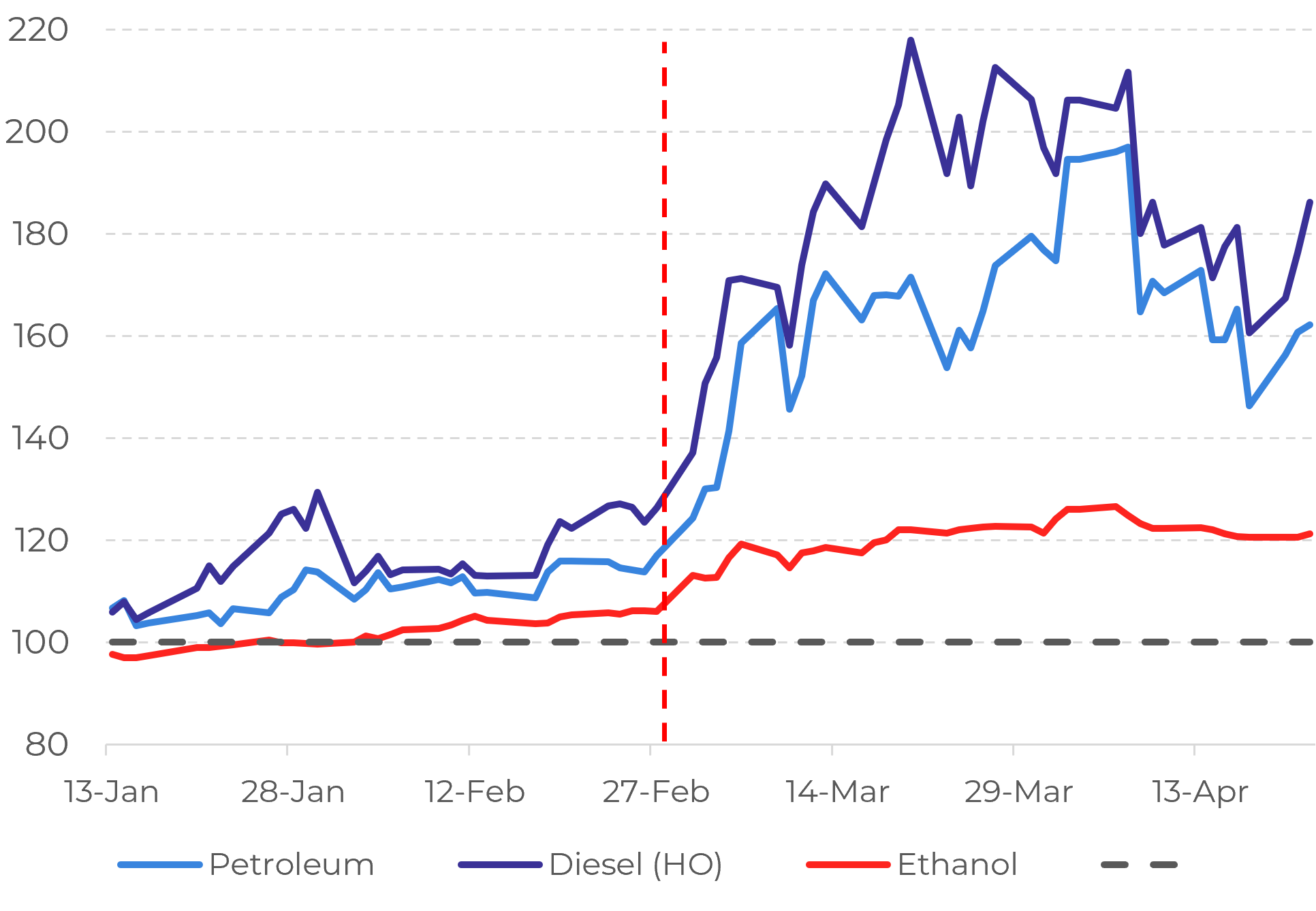

At the same time, a global inflationary shock is observed:

• Rising energy prices (oil and diesel);

• High international freight rates;

• Fertilizers (especially urea) near historic highs.

This environment directly pressures agricultural production costs and creates uncertainty regarding future decisions on acreage and investment.

One of the central themes of the macroeconomic context is the resurgence of biofuels as a global strategic driver:

• Rising oil prices drive up ethanol and biodiesel;

• Vegetable oils (soybean oil, palm oil) are benefiting from this price appreciation;

• There is indirect support for corn and soybeans, but it is strong in derivatives.

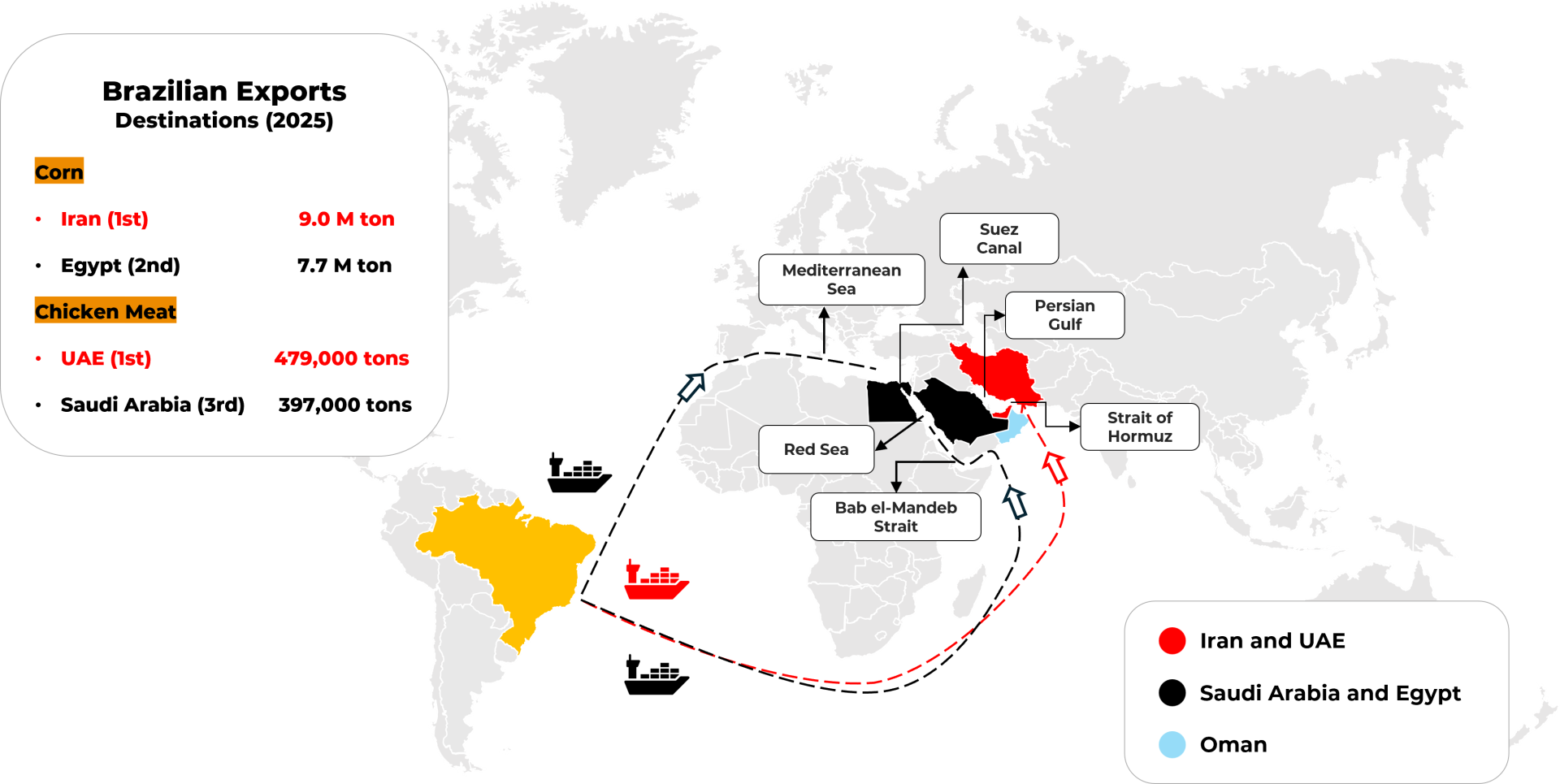

Additionally, there is a significant logistical risk:

• The Middle East is home to major destinations for Brazilian exports (corn and animal protein);

• Disruptions to shipping routes (Strait of Hormuz, Red Sea) could impact trade flows.

The macroeconomic environment currently acts as a supporting factor for soybeans and corn through biofuels and capital flows, but simultaneously increases costs and logistical risks. The net result is greater volatility and price sensitivity to exogenous events.

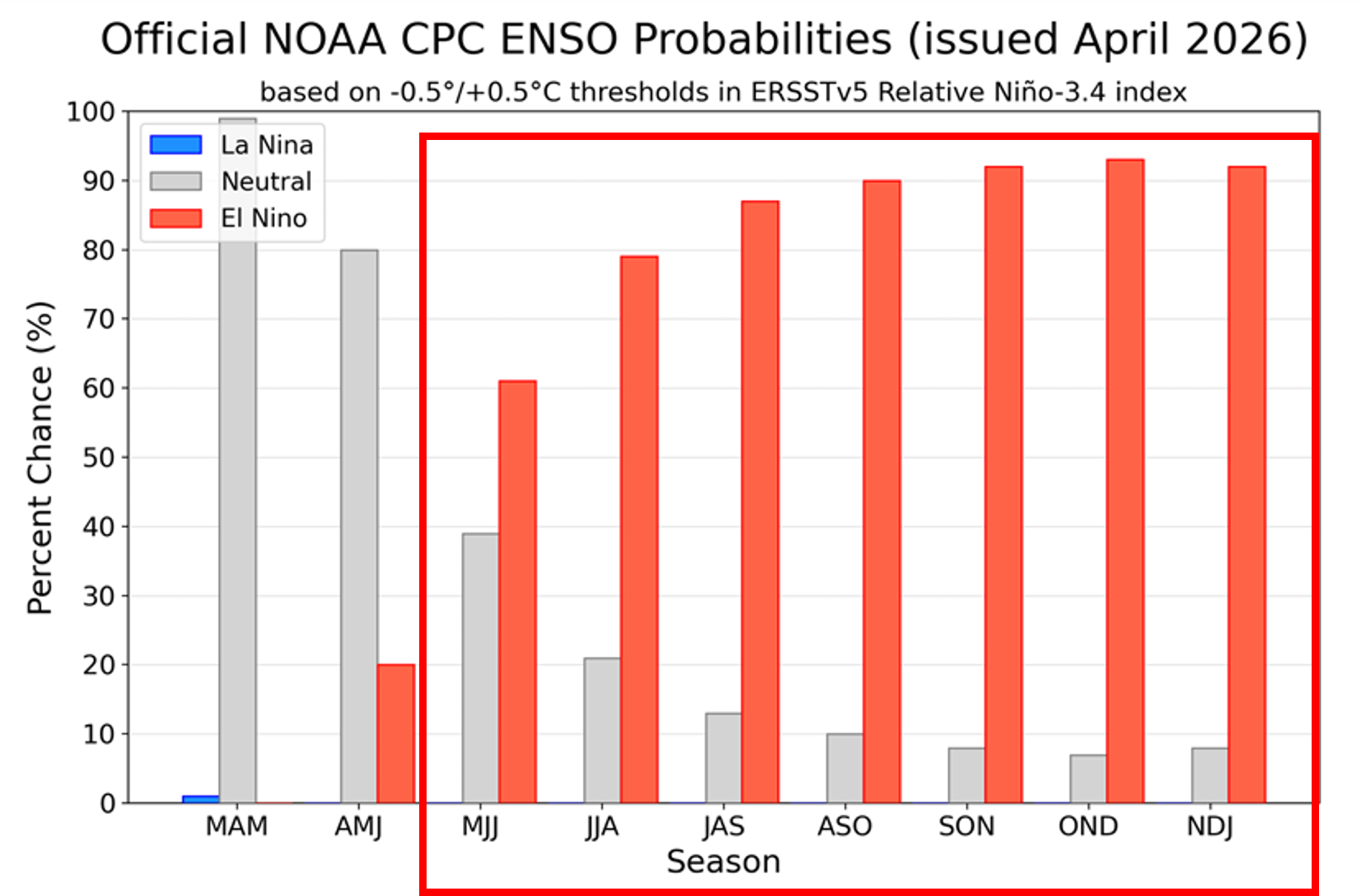

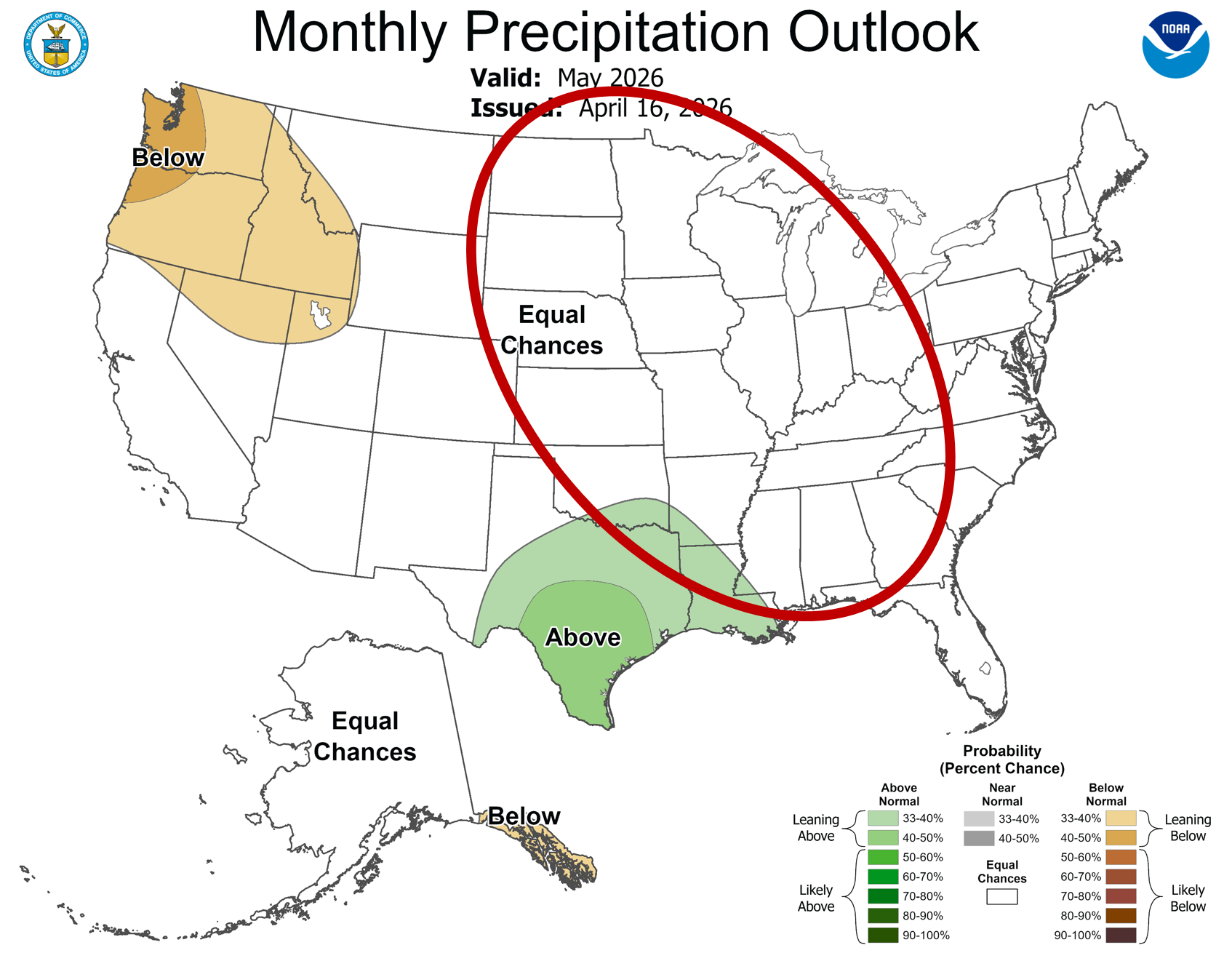

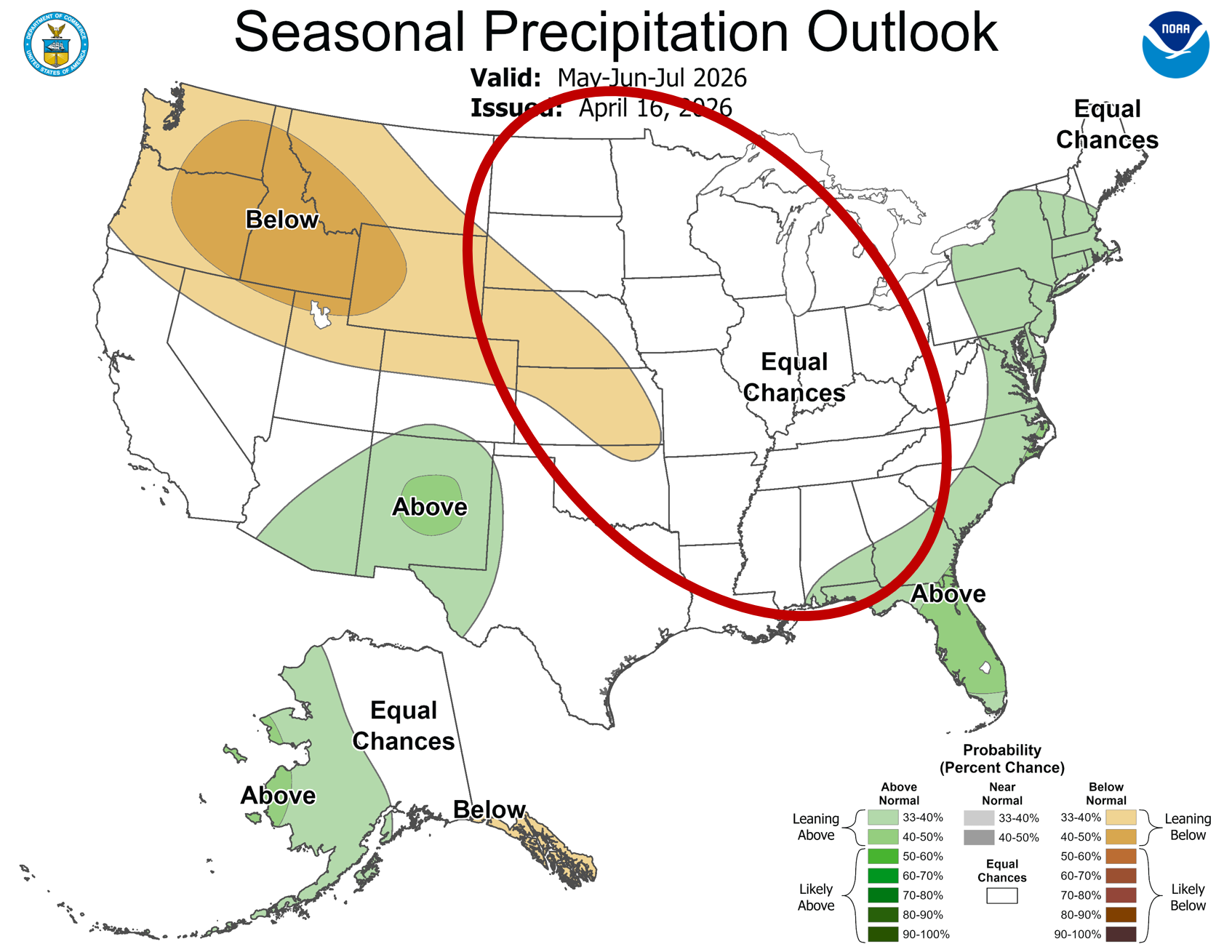

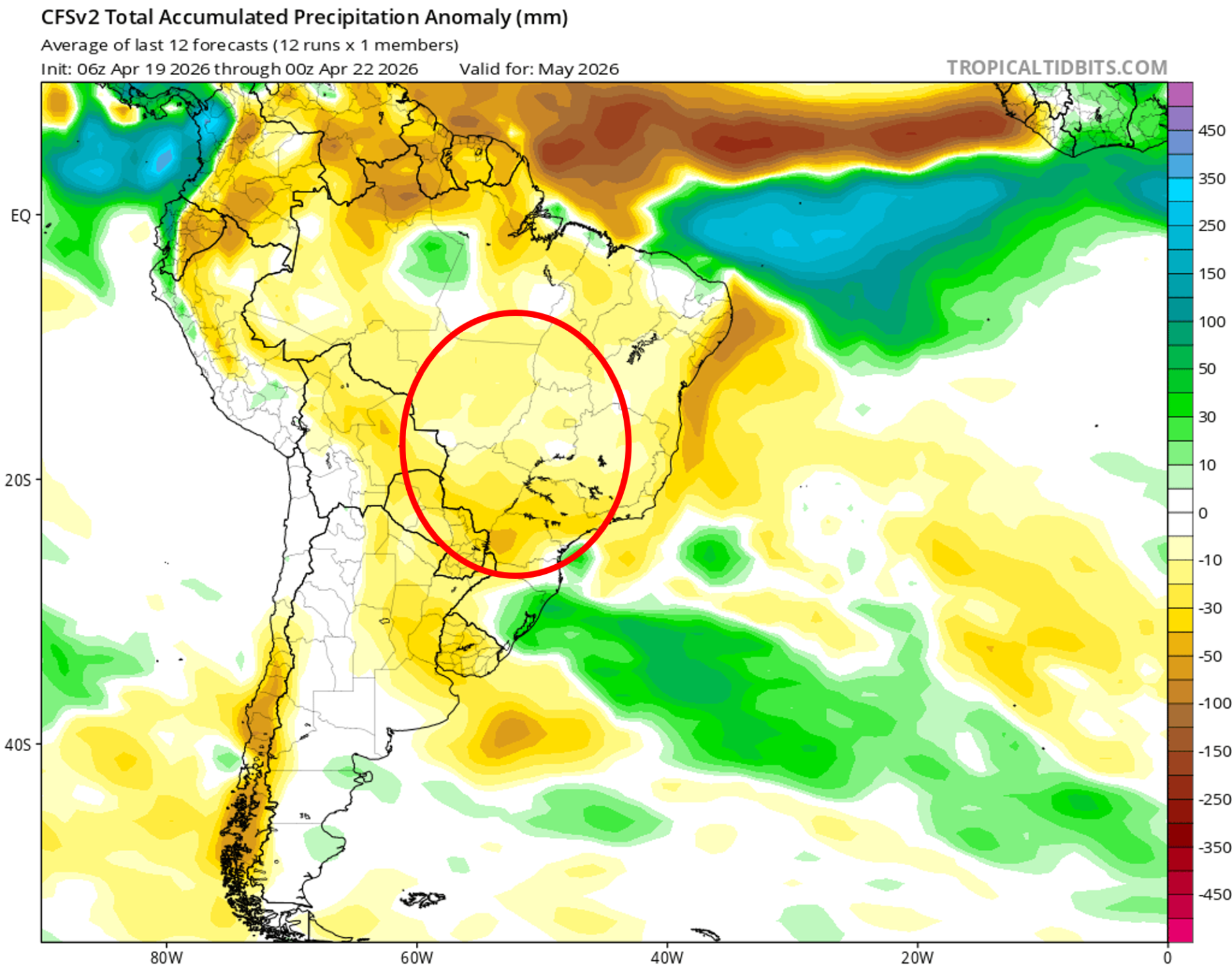

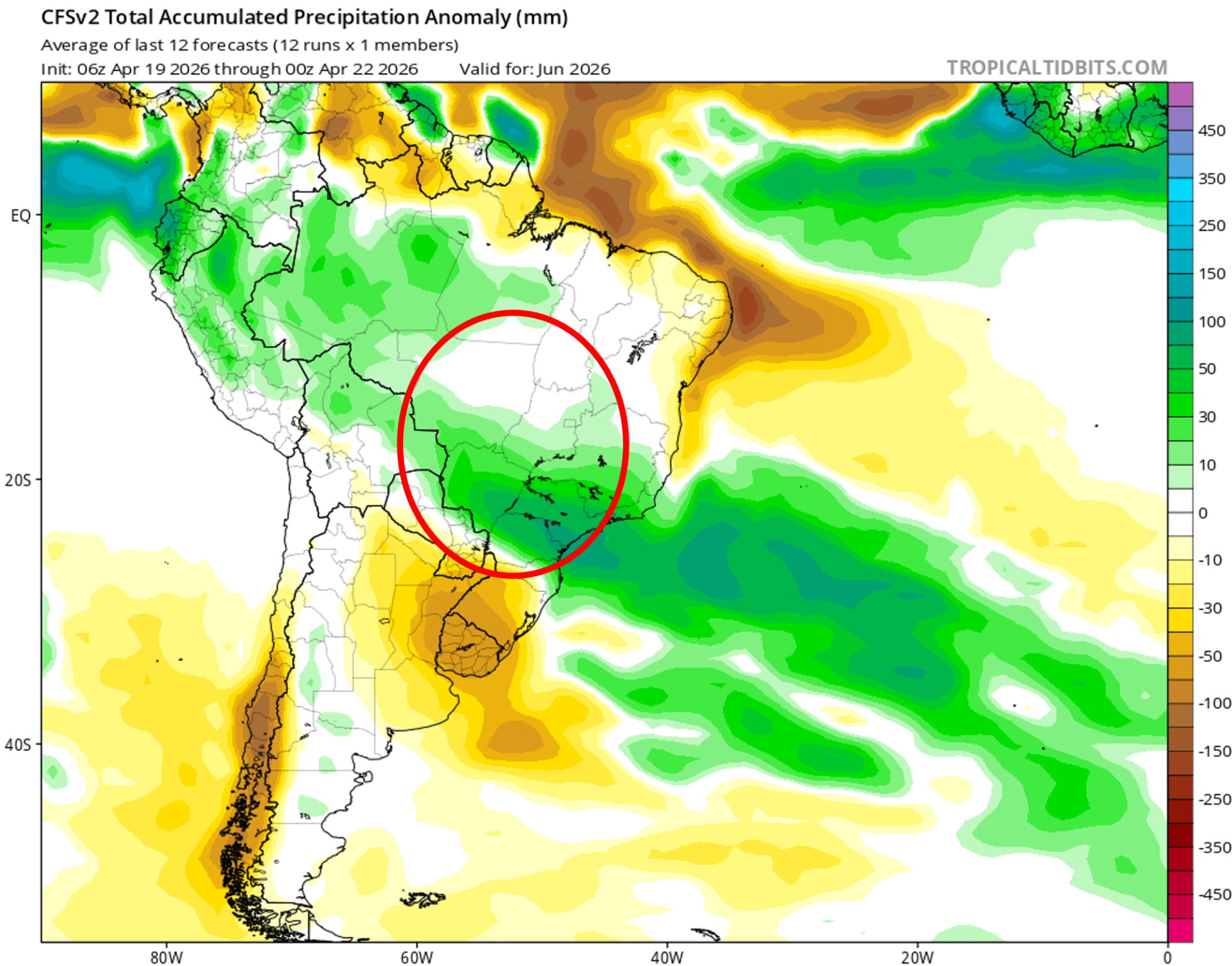

The global weather scenario is in transition:

• End of La Niña → neutral phase (March to May);

• Strong probability of an early onset of El Niño (May/June);

• Increasing chance of a strong to very strong event.

In South America, the expected impacts follow the historical pattern:

• North-central Brazil:

- Higher risk of water shortages;

- Recent history of significant losses during El Niño years (e.g., 2023/24 crop);

• Southern Brazil and Argentina:

- Trend of above-average rainfall;

- Potential for higher yields, but with a risk of excess depending on intensity.

In the short term, the focus is on the Brazilian second crop:

• April/May showing signs of irregular rainfall;

• May is a critical month for crop development.

The weather is the main risk factor of the year. The combination of a strong El Niño and delayed planting of the second corn crop in Brazil significantly increases uncertainty regarding the South American crop 25/26 (Brazilian corn) and, especially, the 26/27 crop (corn and soybeans).

China is experiencing a structural shift toward increased consumption and reduced stocks, following years of maintaining high levels (>200 M tons). Recently:

• Stocks have fallen below 200 million tons;

• Consumption remains steady.

This paves the way for:

• Stock replenishment;

• A potential increase in imports (still moderate at the moment).

However, the country is still far from the peak import levels seen in recent years.

China is a potential future bullish factor, but it does not yet act as a dominant driver in the short term. The market is monitoring signs of a shift in stock rebuilding policy.

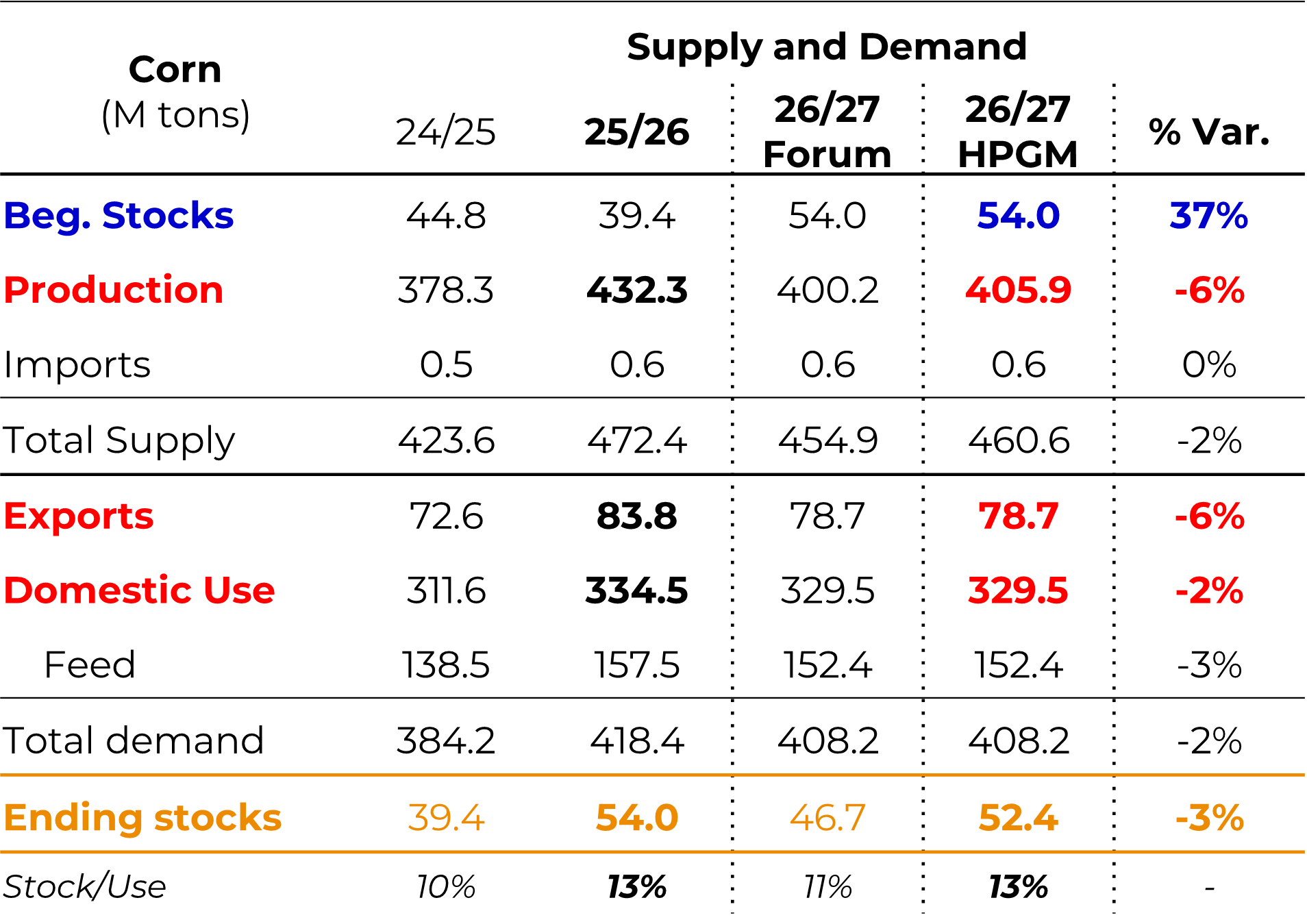

• Recent record production in 25/26 led to an increase in stocks;

• Trend toward reduced acreage in 26/27, due to a shift to soybeans;

• Nevertheless, potential production remains high (~406 M tons).

• Extremely strong exports (potential historic record);

• Main factor currently supporting prices.

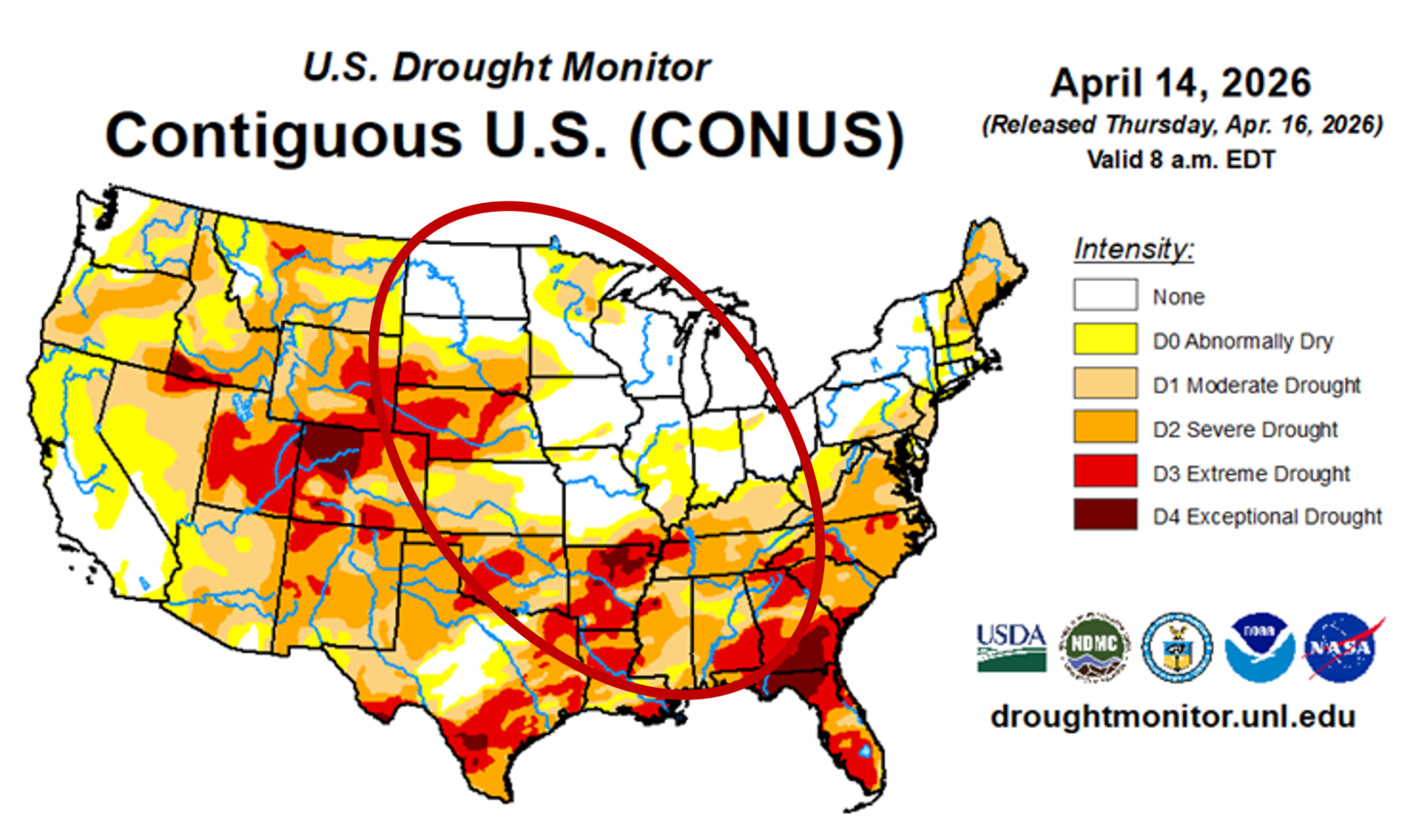

• Early planting;

• Drier soils in key regions (Western/Southern Corn Belt);

• Forecast:

- Short term: beneficial rains;

- Medium term: slight risk of water deficit in the western part.

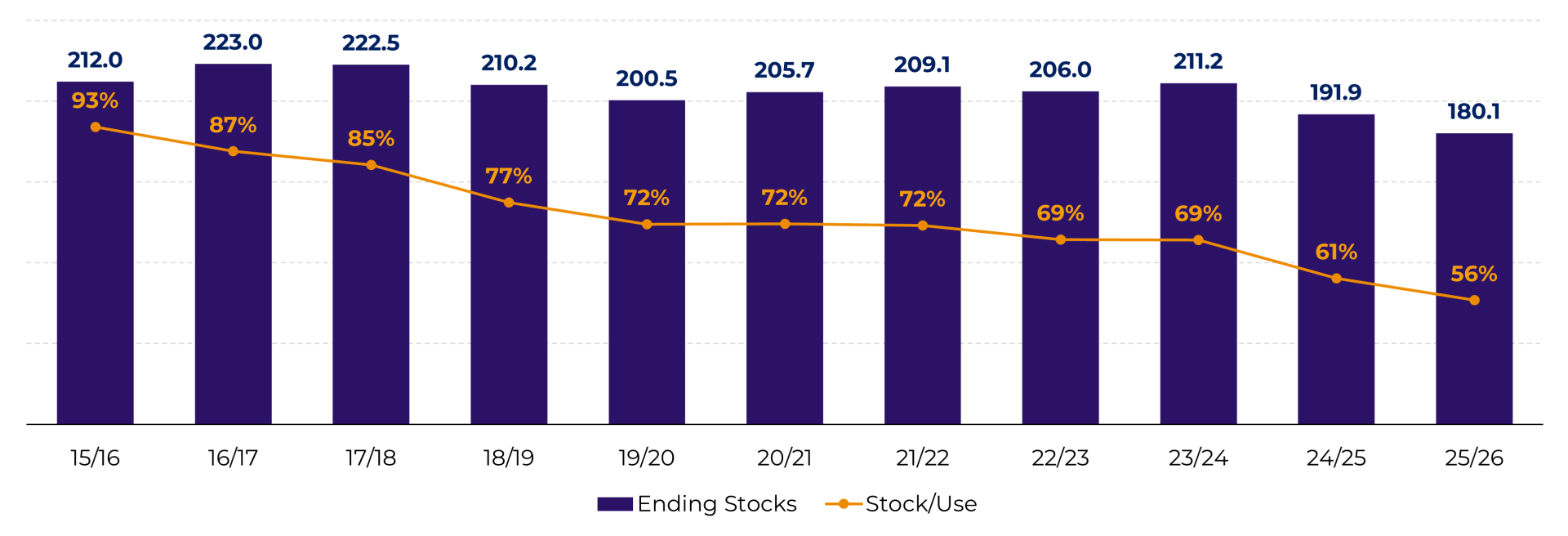

• Room for downside corrections, given current stock levels;

• Support from demand and fund positioning.

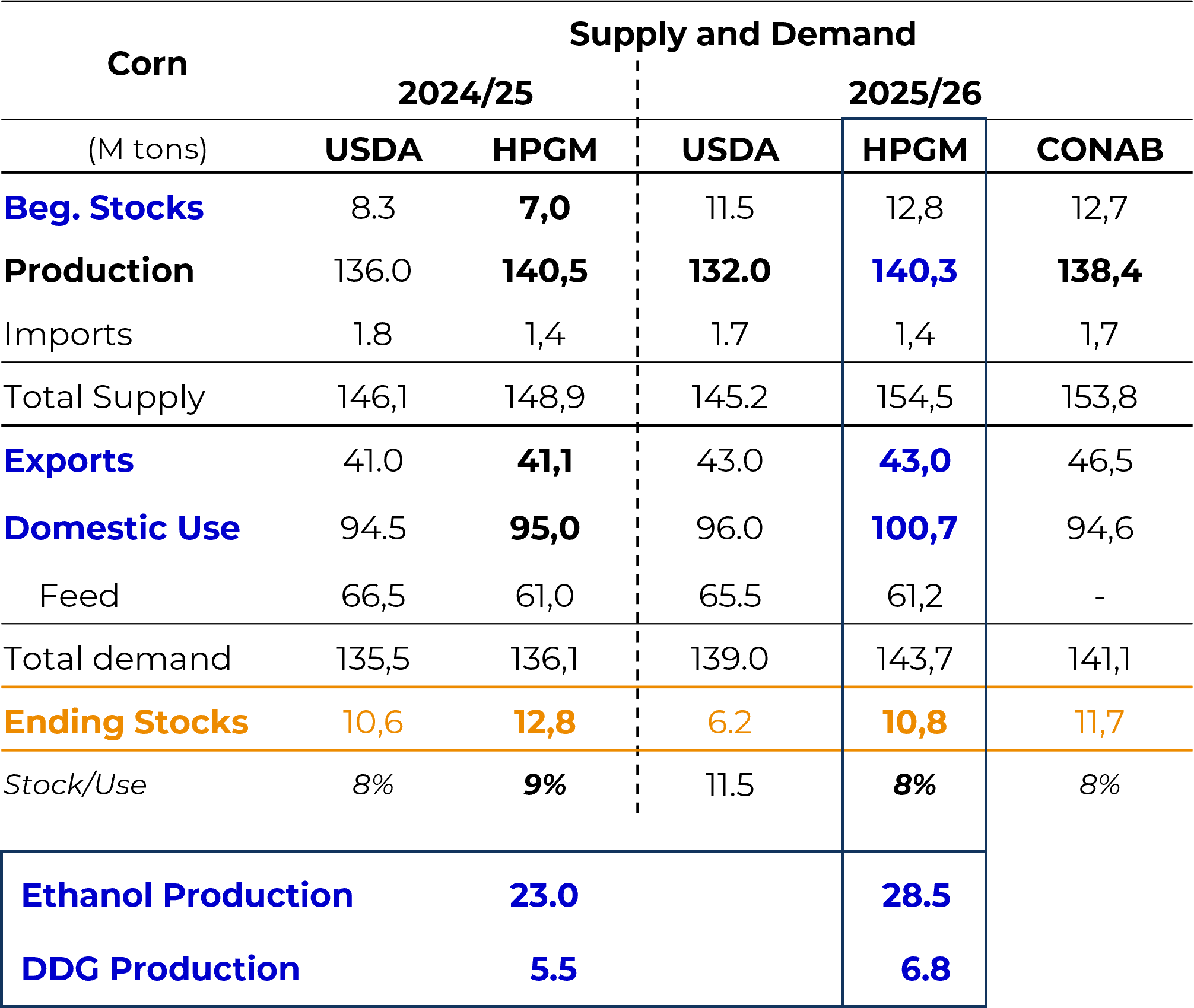

U.S. corn has a comfortable supply-demand balance, with a structural bearish bias on the supply side, partially offset by exceptionally strong external demand.

• Potential crop: ~140 M tons (above initial official estimates);

• Second crop:

- Planting complete, but outside the ideal window;

- Strong dependence on weather in May/June.

• Record domestic consumption (~100 M tons);

• Structural growth in corn ethanol:

- Rapid expansion of mills;

- Shift of industrial demand for corn to the interior (no longer restricted to the Midwest).

• Potential: record of ~43 M tons;

• Dependence on:

- International logistics;

- Competition with Argentina and the U.S.

Source: USDA, Conab, Hedgepoint

• Support above seasonal levels;

• Structural shift driven by new industrial demand;

• The “full” second crop could still weigh on prices.

Brazil is undergoing a structural transformation in corn demand, with ethanol altering the floor of domestic prices. In the short term, the weather risk for the second crop is the main determinant.

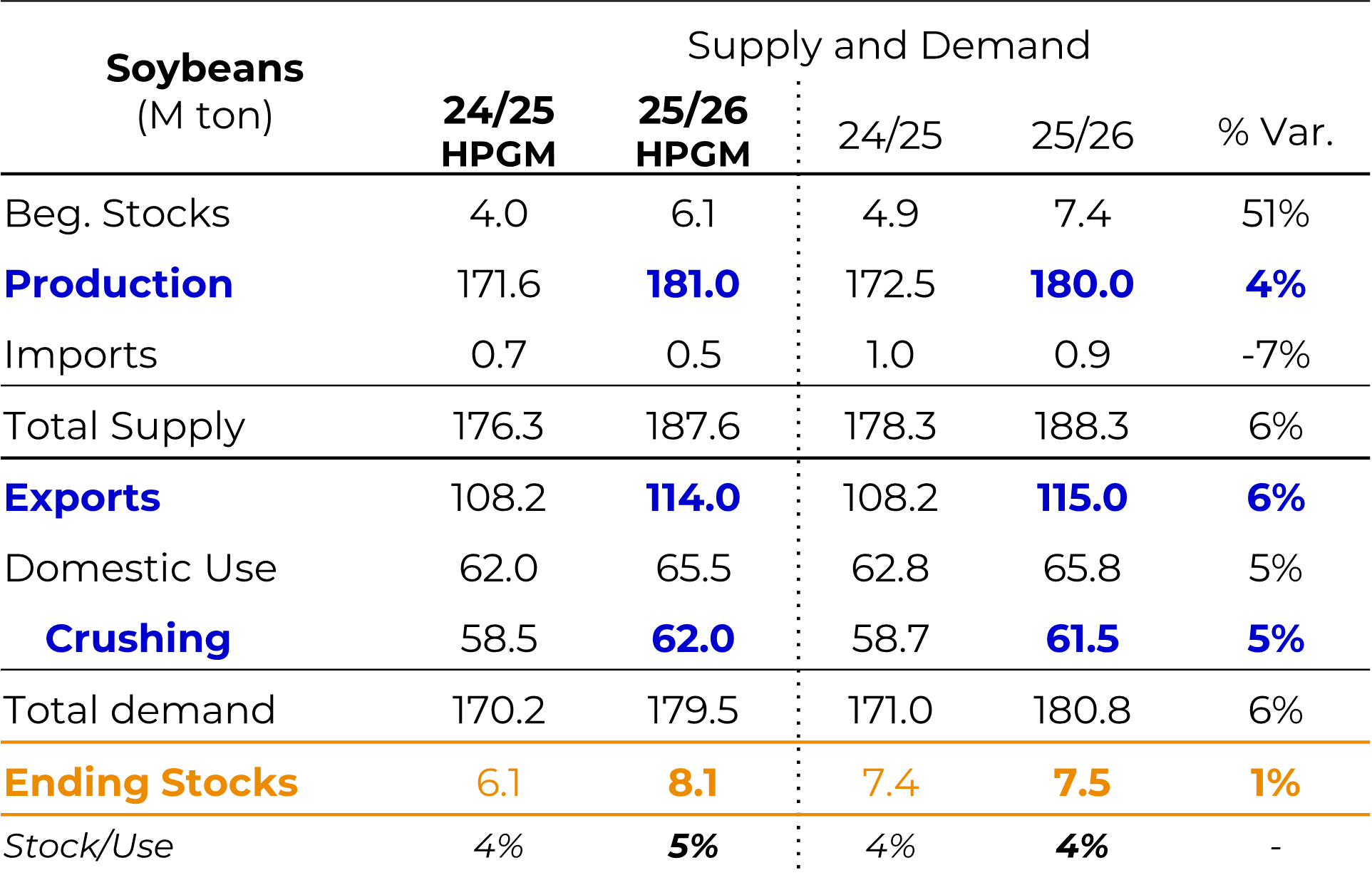

• Potential production significantly higher than the USDA estimate (67 M tons vs. 53 M tons);

• Low domestic consumption → high exportable surplus;

• A more favorable economic environment stimulates sales.

Argentina is the main competitive risk for Brazil in the international market, with the capacity to put downward pressure on prices through increased exportable supply.

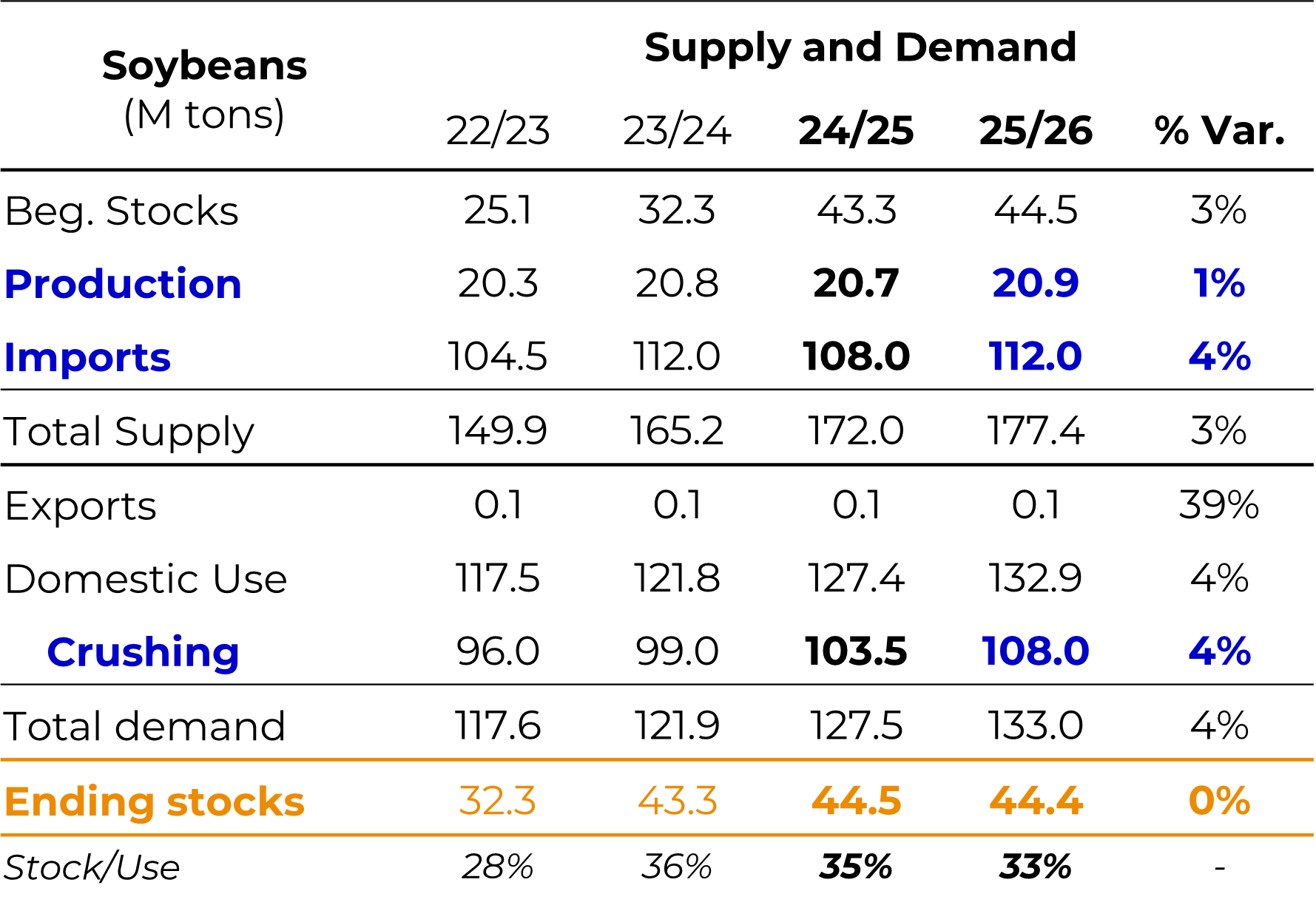

Structural situation distinct from that of corn:

• High stocks (~43–44 M tons) and recovering in recent years;

• Comfortable stock-to-use ratio (~33%);

• High port stocks.

Consequences:

• Less urgency to buy;

• More measured import pace;

• Crushing margins do not encourage aggressive buying.

China acts as a neutral factor for soybeans in the short term, given its comfortable supply position. However, potential talks between the U.S. and China in May could bring new developments.

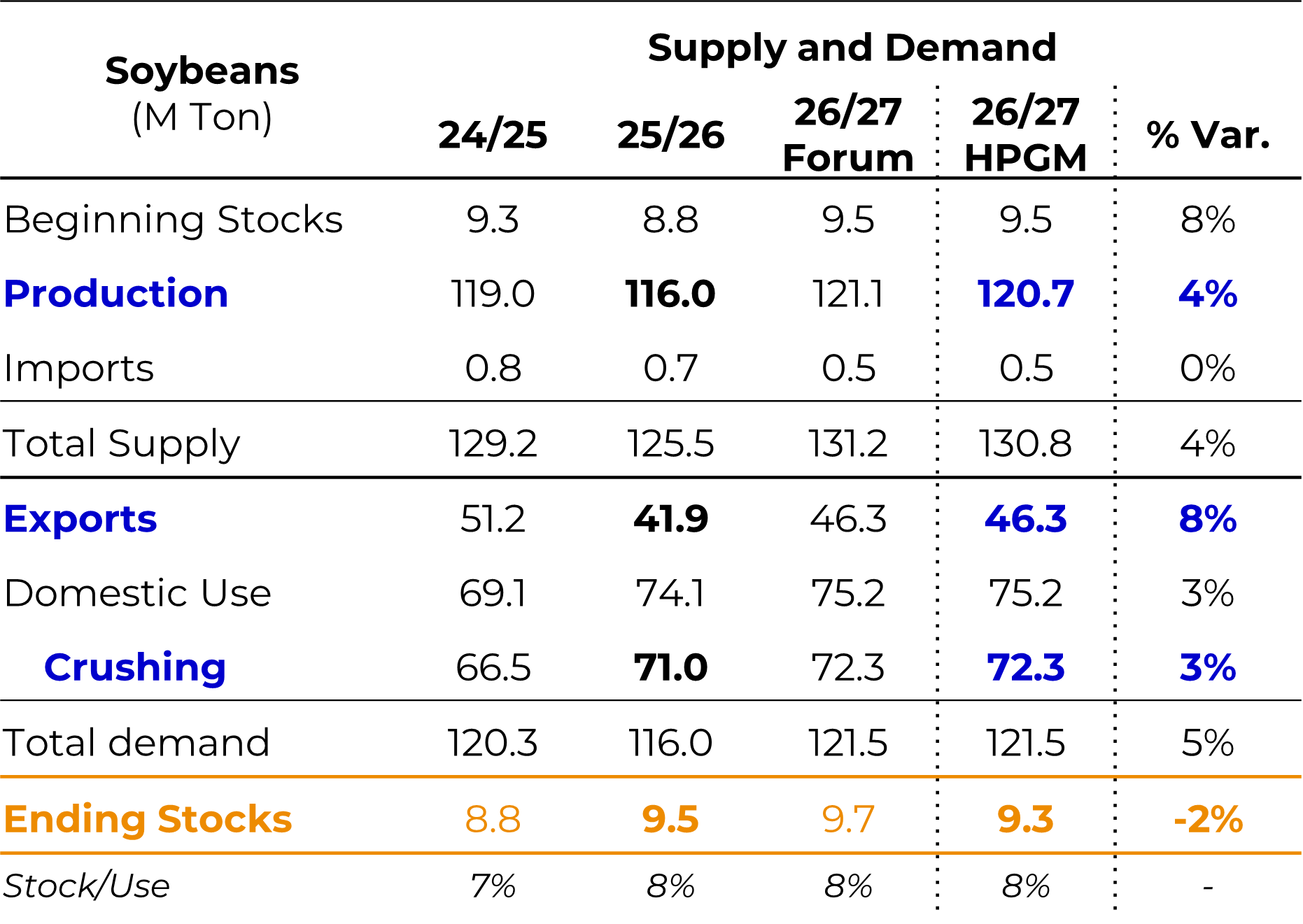

• Significant increase in planted area in 26/27;

• High potential production (~121 M tons).

• Key highlight: record crush;

• Strong growth in demand for soybean oil:

- Increased biodiesel blend;

- Expansion of industrial capacity.

• High oil share supports margins;

• Stocks remain stable despite higher production, with supply-demand balance maintained by domestic demand.

• Current range: $11.40 to $11.80/bushel;

• Room for correction, but with structural support.

U.S. soybeans have solid structural fundamentals driven by demand for oil, which may limit sharper declines even in a scenario of higher supply.

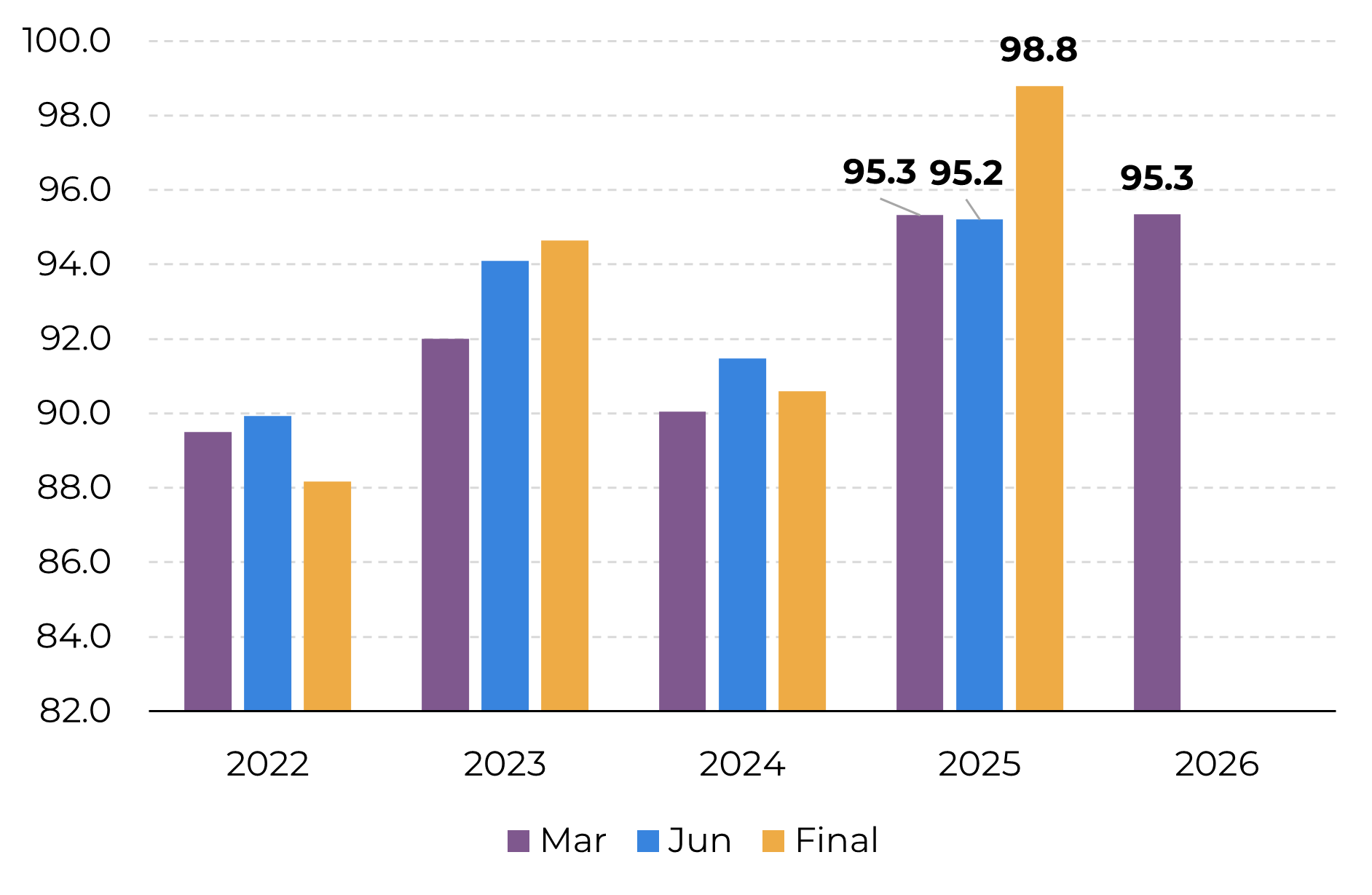

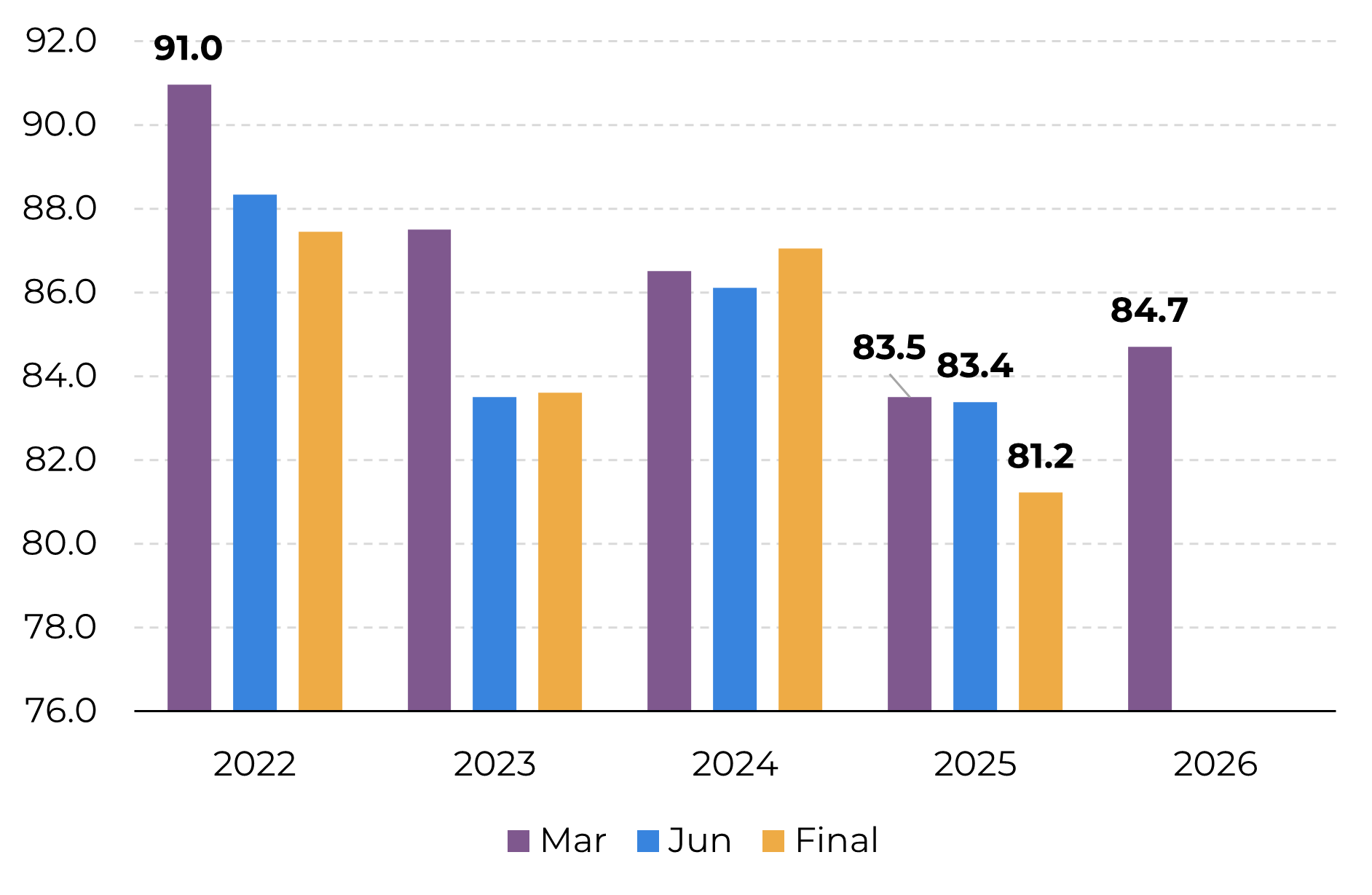

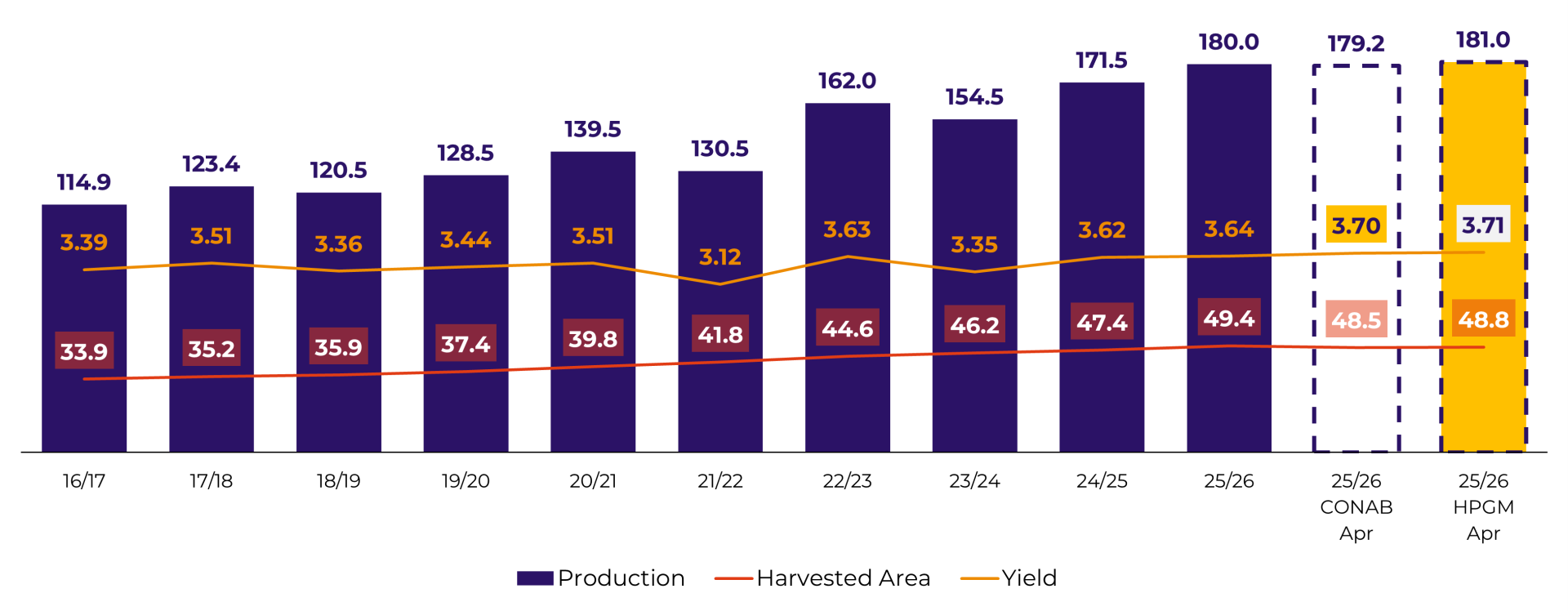

• 25/26 bumper crop: ~181 M tons (Hedgepoint);

• High yields in the Midwest offsetting losses in the South.

Source: USDA, Conab, Hedgepoint

• Record potential (~114 M tons).

• Slow, but picking up pace as the harvest progresses.

• Pressured by:

- High supply;

- A stronger real;

• Soybean prices below R$ 100/bag in the interior of the country.

• High freight costs impacting producer margins.

Brazil faces short-term price pressure, with oversupply and an unfavorable exchange rate, despite more constructive global fundamentals.

• Decline in production (shift to corn);

• Trend of strong decline in soybean grain exports by 2026;

• Greater focus on domestic processing.

Argentina is no longer a major player in soybean exports, making room for Brazil and the U.S. in global trade.

• Strong corn exports (U.S.)

• Expansion of biofuels:

- Corn ethanol

- Biodiesel (soybean oil)

• Reduction in corn acreage in the US

• Possible increase in imports from China (corn)

• Structural growth in soybean crush in the US

• High production:

- Corn (US, Brazil, Argentina)

- Soybeans (Brazil, US)

• Adequate soybean stocks in China

• Increase in soybean acreage in the U.S.

• Possible end to the US-Iran conflict

The market is in a balance between short-term oversupply and structural strengthening of demand (biofuels). The dominant trend will depend on weather, geopolitics, and China’s behavior.

The current scenario for the corn and soybean complex markets is marked by an imbalance between short- and medium-term fundamentals. In the short term, the combination of high supply—notably Brazil’s soybean bumper crop and robust production in the United States—and more subdued demand from China, especially for soybeans, continues to put pressure on prices. On the other hand, a structural support vector is consolidating, led by the expansion of biofuels, which drives soybean crushing and corn consumption for ethanol, reducing the risk of sharper and prolonged declines.

In this context, the market tends to operate with high volatility and sensitivity to exogenous factors, particularly weather and geopolitics. The potential development of a strong El Niño represents the main upside risk, while normal weather conditions and a possible easing of international tensions could amplify corrective movements.

Thus, the current balance is unstable: there is room for downward adjustments in the short term, but strengthening structural demand and the absence of significant clim l risks limit the depth of these declines and maintain a more constructive medium-term outlook.