Cocoa market remains unstable with focus on weather and consumption

- The cocoa market remains volatile, with September futures contracts accumulating weekly declines of 3% in New York and 5% in London through June 26.

- Improved weather conditions in West Africa, especially in Ghana, have raised expectations for the next season, contributing to the bearish trend. However, the market remains cautious.

- The market is expecting second-quarter grind data from major processing regions, which will be key to assessing the impact of high prices on global consumption and possible short-term price developments.

- Net cocoa imports by Europe have fallen 9.53% since the start of the current harvest compared to the same period in the previous cycle, indicating a possible slowdown in demand in the face of high prices.

Cocoa market remains unstable with focus on weather and consumption

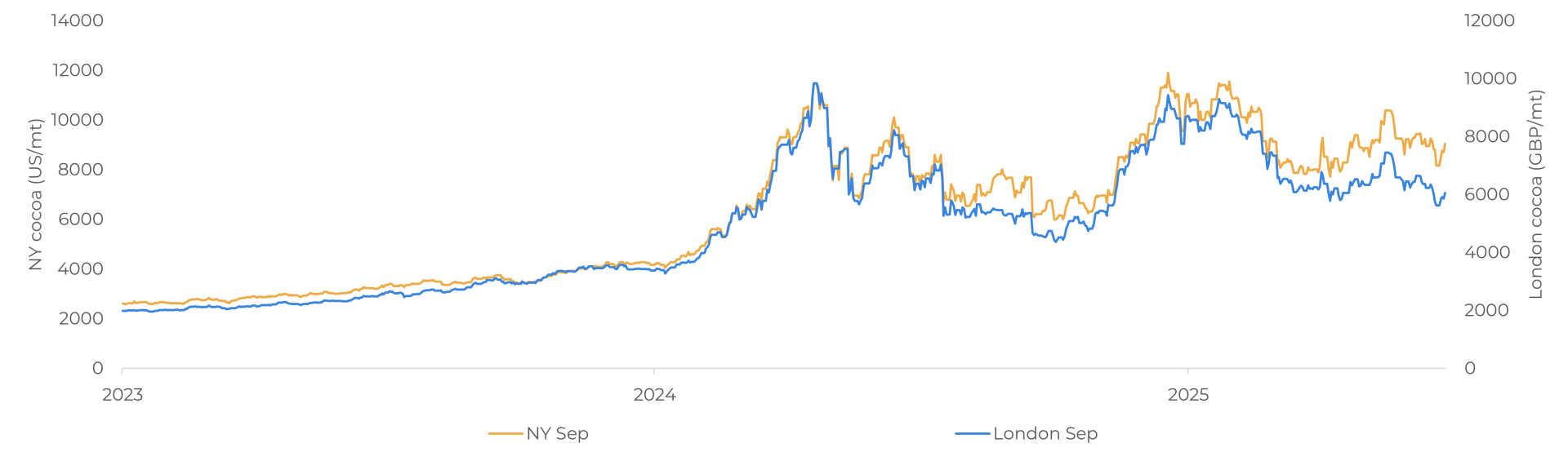

The cocoa market remains volatile. In New York, September contract prices rose last Thursday (26) and broke through the resistance level of USD 8,770/t after Ghana announced that it had reduced its estimate for the current harvest from 610,000 tons to 600,000 tons. The devaluation of the dollar may also have contributed to this scenario. Although the cut was already expected, the adjustment reinforced concerns about supply and provided support to the market. Even so, as of June 26, September futures contracts were down 3% in New York and 5% in London on a weekly basis.

Cocoa Prices

Source: LSEG

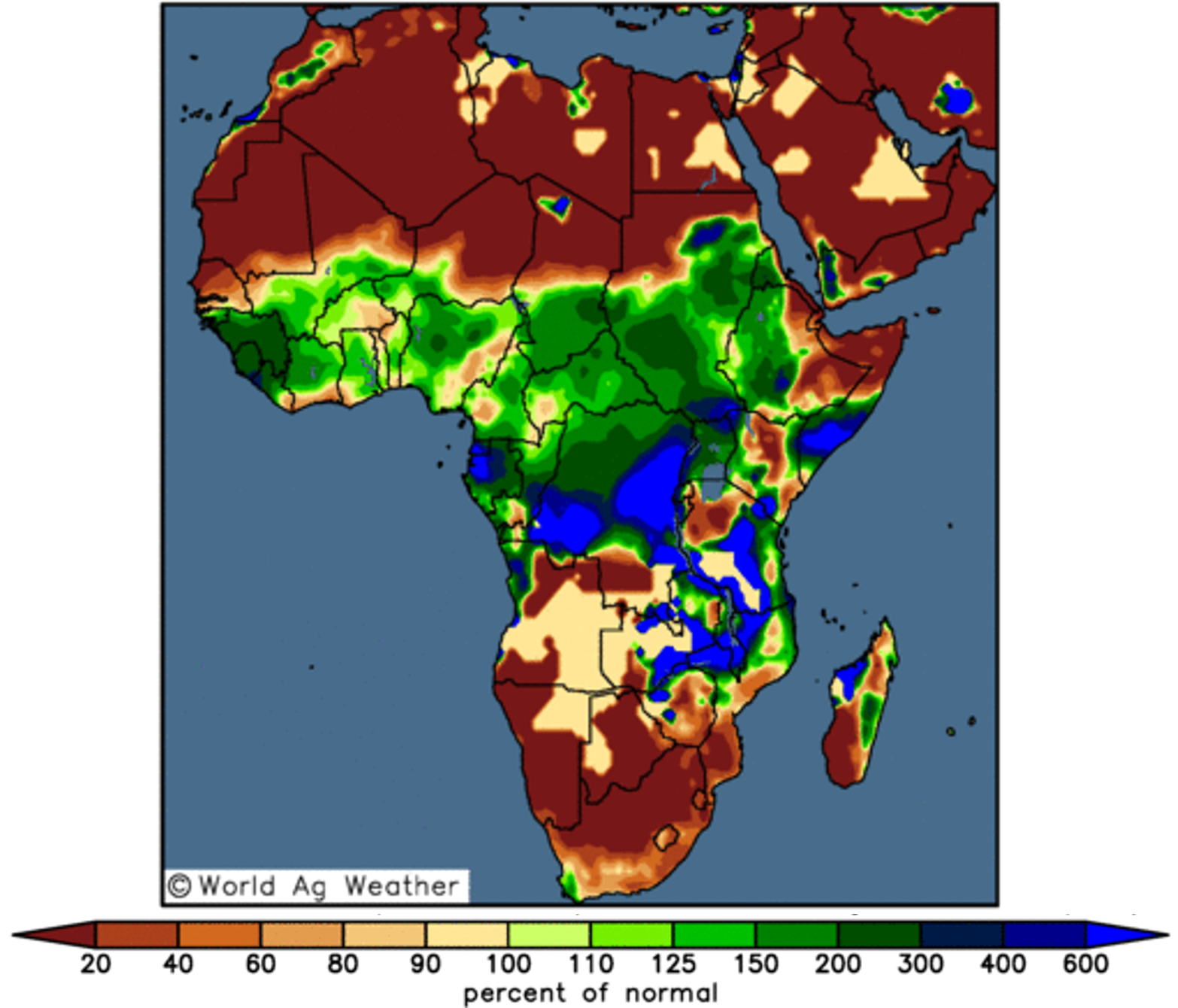

Among the main factors supporting this bearish trend in the short to medium term is the improvement in weather forecasts for West Africa, a region responsible for a large part of global cocoa production. Weather models indicate the possibility of above-average rainfall in key African production areas, generating cautious optimism among producers, especially in Ghana. The agronomic conditions of the country's plantations have also shown signs of recovery, reinforcing more positive expectations for the next crop. Despite this more favorable scenario, official estimates for the 25/26 season in Ghana and Ivory Coast have not yet been released, keeping the market attentive to further developments.

EC Precipitation Anomaly - Next 14 Days (% of normal)

Source: World Ag Weather

With few updates, the market is awaiting the results of cocoa grinding by processing associations in the US, Asia, and Europe for the second quarter of 2025, an important indicator related to demand. This will make it possible to verify the impact of cocoa prices, which, even after corrections, are still well above historical levels, on global bean consumption.

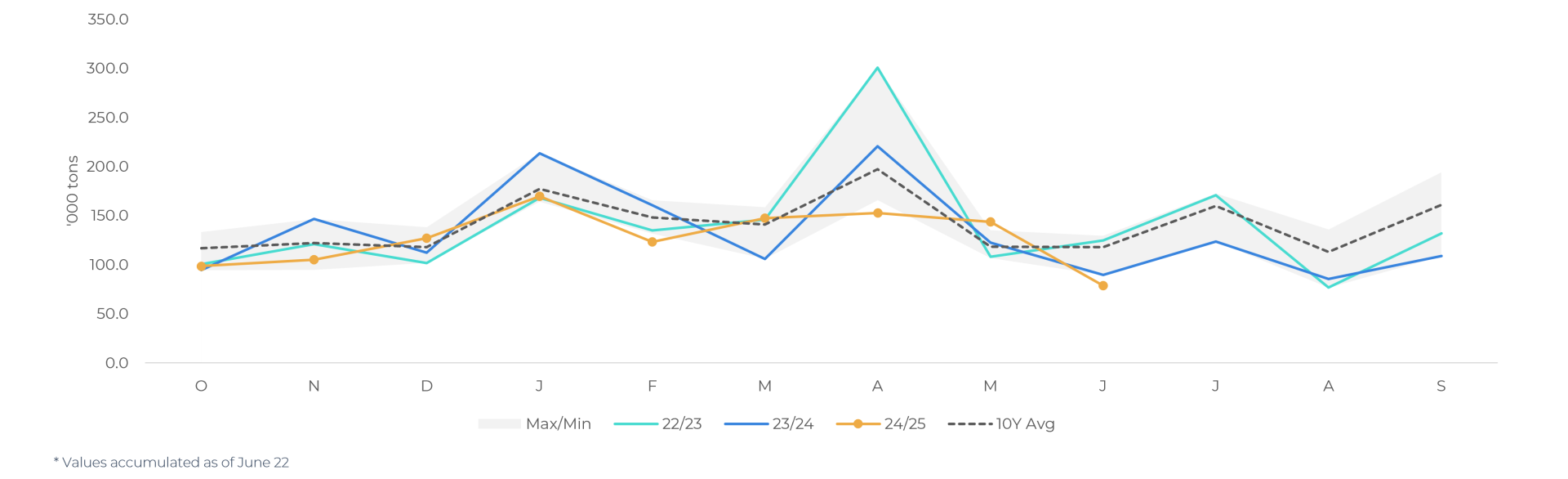

In this sense, when analyzing imports from Europe, one of the main markets for the commodity, the data shows a decline. Since the beginning of the current season (Oct/24 to Jun/25*), the volume of total net cocoa imports (beans, paste, butter, and powder) was 9.53% lower than in the corresponding period of the 23/24 cycle. This reduction may be associated with the limited supply of the commodity in recent crops, which resulted in higher prices for beans and their by-products.

EU: Net Cocoa Imports ('000 tons)

Source: European Comission

This trend has already been confirmed by cocoa grinding data for the first quarter of this year, which showed a decline compared to the same period last year. Additionally, the recent financial results of some of the main processors in the sector also indicated a decline.

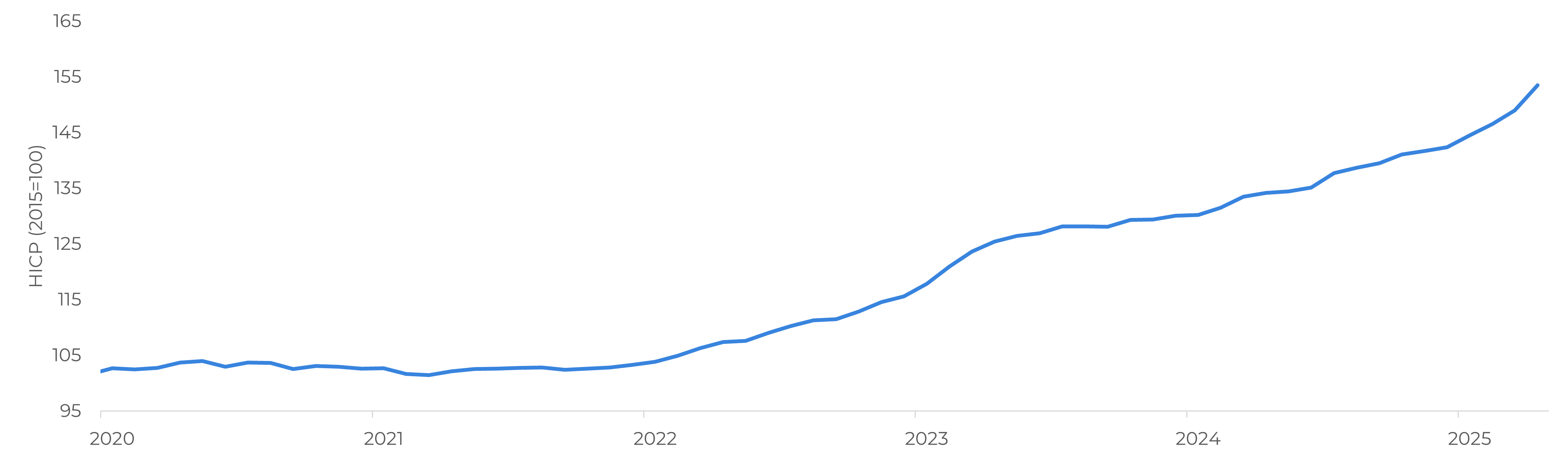

These signs reinforce the impact of restricted supply and high prices on the production chain. The Harmonised European Consumer Price Index also highlights this scenario, pointing to a significant increase in the prices of cocoa and its derivatives in the European market.

Europe: Harmonised Index of Consumer Prices (HICP) for Cocoa and Powdered Chocolate

Source: Eurostat

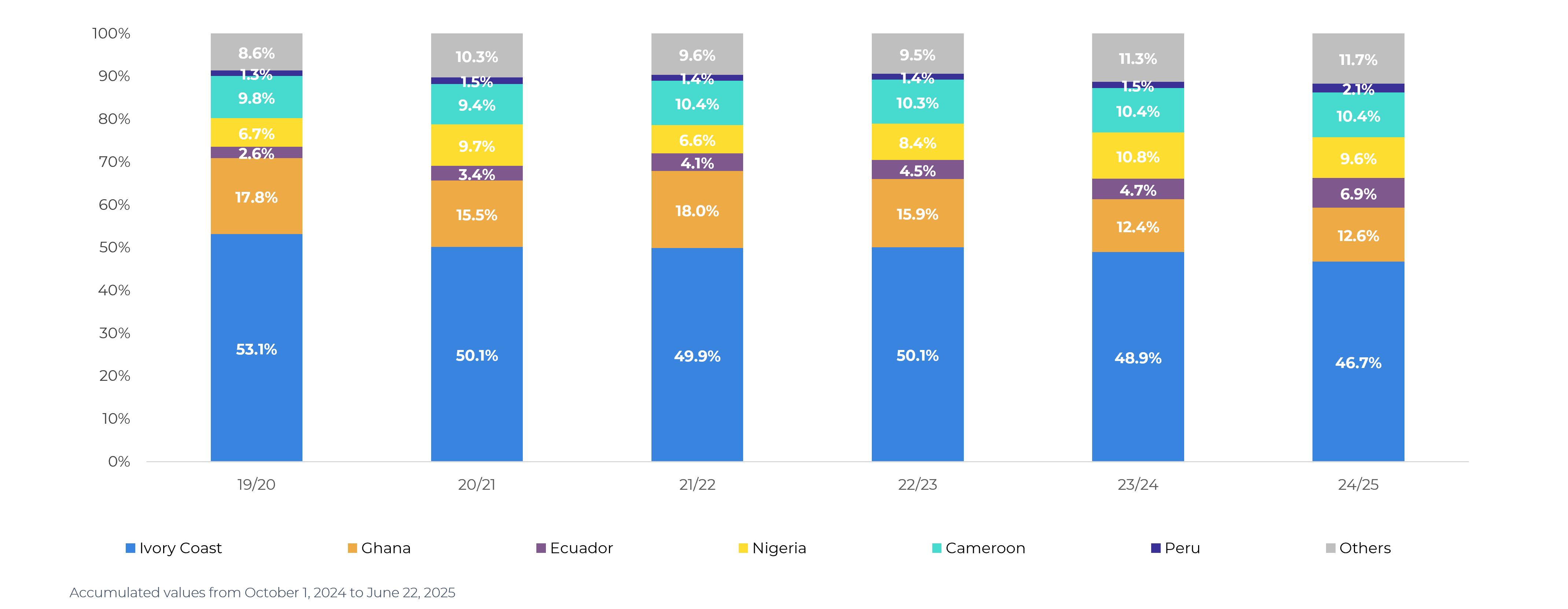

Thus, the results of the grindings may contribute to a scenario of bearish pressure on prices, especially if further reductions are observed in the coming quarters. In terms of origins, there has been a decrease in Ivory Coast's share of European imports. This movement may be a consequence of problems related to the quality of beans and the slowdown in cocoa deliveries at Ivorian ports, factors that have already been addressed in previous analyses.

EU: Participation of Origins in Cocoa Imports (% of total)

Source: European Comission

Finally, agents remain attentive to any signs that may alter the dynamics of global supply and demand, with volatility remaining a hallmark of the current moment.

In Summary

The cocoa market remains volatile, with September futures contracts recording weekly declines of 3% in New York and 5% in London through June 26. Among the factors pushing prices down are more favorable weather forecasts for West Africa, especially in Ghana, where production is expected to recover. However, official estimates for the 2025/26 crop have not yet been released.

The market is awaiting second quarter grinding data, which will indicate the impact of high prices on demand. European cocoa imports have already fallen by 9.53% since the start of the current harvest, which may reflect tight supply and high prices. Agents remain attentive to any changes in supply and demand, with volatility remaining the main feature at the moment.

Weekly Report — Cocoa

carolina.frança@hedgepointglobal.com

livea.coda@hedgepointglobal.com

Disclaimer

This document has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without intending to create obligations or commitments to third parties. It is not intended to promote or solicit an offer for the sale or purchase of any securities, commodities interests, or investment products. Hedgepoint and its associates expressly disclaim any liability for the use of the information contained herein that directly or indirectly results in any kind of damages. Information is obtained from sources which we believe to be reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. The trading of commodities interests, such as futures, options, and swaps, involves substantial risk of loss and may not be suitable for all investors. You should carefully consider wither such trading is suitable for you in light of your financial condition. Past performance is not necessarily indicative of future results. Customers should rely on their own independent judgment and/or consult advisors before entering into any transactions. Hedgepoint does not provide legal, tax or accounting advice and you are responsible for seeking any such advice separately. Hedgepoint Schweiz AG is organized, incorporated, and existing under the laws of Switzerland, is filiated to ARIF, the Association Romande des Intermédiaires Financiers, which is a FINMA-authorized Self-Regulatory Organization. Hedgepoint Commodities LLC is organized, incorporated, and existing under the laws of the USA, and is authorized and regulated by the Commodity Futures Trading Commission (CFTC) and a member of the National Futures Association (NFA) to act as an Introducing Broker and Commodity Trading Advisor. HedgePoint Global Markets Limited is Regulated by the Dubai Financial Services Authority. The content is directed at Professional Clients and not Retail Clients. Hedgepoint Global Markets PTE. Ltd is organized, incorporated, and existing under the laws of Singapore, exempted from obtaining a financial services license as per the Second Schedule of the Securities and Futures (Licensing and Conduct of Business) Act, by the Monetary Authority of Singapore (MAS). Hedgepoint Global Markets DTVM Ltda. is authorized and regulated in Brazil by the Central Bank of Brazil (BCB) and the Brazilian Securities Commission (CVM). Hedgepoint Serviços Ltda. is organized, incorporated, and existing under the laws of Brazil. Hedgepoint Global Markets S.A. is organized, incorporated, and existing under the laws of Uruguay. In case of questions not resolved by the first instance of customer contact (client.services@Hedgepointglobal.com), please contact internal ombudsman channel (ombudsman@hedgepointglobal.com – global or ouvidoria@hedgepointglobal.com – Brazil only) or call 0800-8788408 (Brazil only). Integrity, ethics, and transparency are values that guide our culture. To further strengthen our practices, Hedgepoint has a whistleblower channel for employees and third-parties by e-mail ethicline@hedgepointglobal.com or forms Ethic Line – Hedgepoint Global Markets. “HedgePoint” and the “HedgePoint” logo are marks for the exclusive use of HedgePoint and/or its affiliates. Use or reproduction is prohibited, unless expressly authorized by HedgePoint. Furthermore, the use of any other marks in this document has been authorized for identification purposes only. It does not, therefore, imply any rights of HedgePoint in these marks or imply endorsement, association or seal by the owners of these marks with HedgePoint or its affiliates.