A bittersweet Easter for the cocoa market: high retail prices and uncertainty for the industry in Brazil

- Cocoa futures ended the week of March 27 lower, reversing some of their previous gains and remaining within a narrower trading range.

- In the absence of significant changes in fundamentals, recent movements continued to be driven primarily by technical factors and fluctuations in the macroeconomic environment and the energy market.

- Despite the sharp drop in cocoa beans compared to last year, prices for end consumers remain high in Europe, the United States, and also in Brazil.

- In the Brazilian market, Easter is likely to be bittersweet for consumers, who are still expected to face higher chocolate prices this season.

- At the same time, the Brazilian industry continues to monitor additional challenges related to bean supply, trade flows, and conditions for processing and exporting derivatives.

A bittersweet Easter for the cocoa market: high retail prices and uncertainty for the industry in Brazil

Reversing part of the previous week’s gains, cocoa futures closed the week of March 27 at 3,165 USD/t in New York and 2,370 GBP/t in London, with prices fluctuating within a narrower range. In the absence of significant changes in fundamentals, price movements were predominantly technical in nature, also influenced by fluctuations in the macroeconomic landscape and the energy market amid the conflict in the Middle East, as discussed in the previous week. In this analysis, we will discuss some key points regarding one of the most important periods for the cocoa market, from the perspective of demand and grinding.

On the eve of Easter, an important period for the cocoa market due to the seasonal nature of chocolate consumption in various countries, international cocoa bean prices have fallen by approximately 60% compared to the same period last year. However, this does not mean immediate relief for the final consumer, and in practice, chocolate prices are still likely to remain high this season.

This is explained, in part, by the fact that a significant portion of the industry purchased raw materials when cocoa was still trading at higher levels, in addition to current international prices remaining high by historical standards. As a result, measures such as portfolio adjustments, product reformulations, and price pass-throughs continued to be adopted throughout 2025. At the same time, higher retail prices have also been altering consumption patterns, keeping final-consumer demand under pressure.

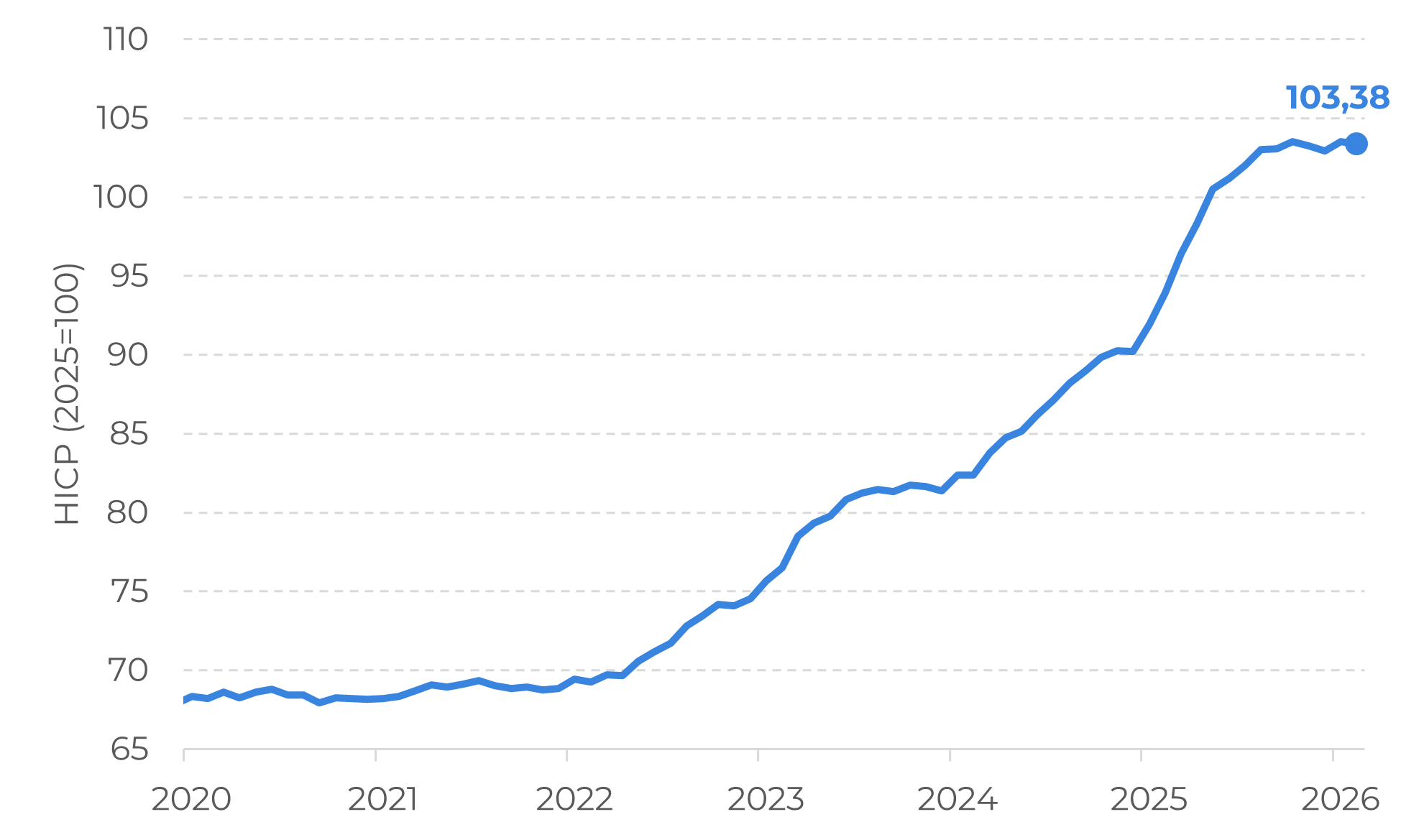

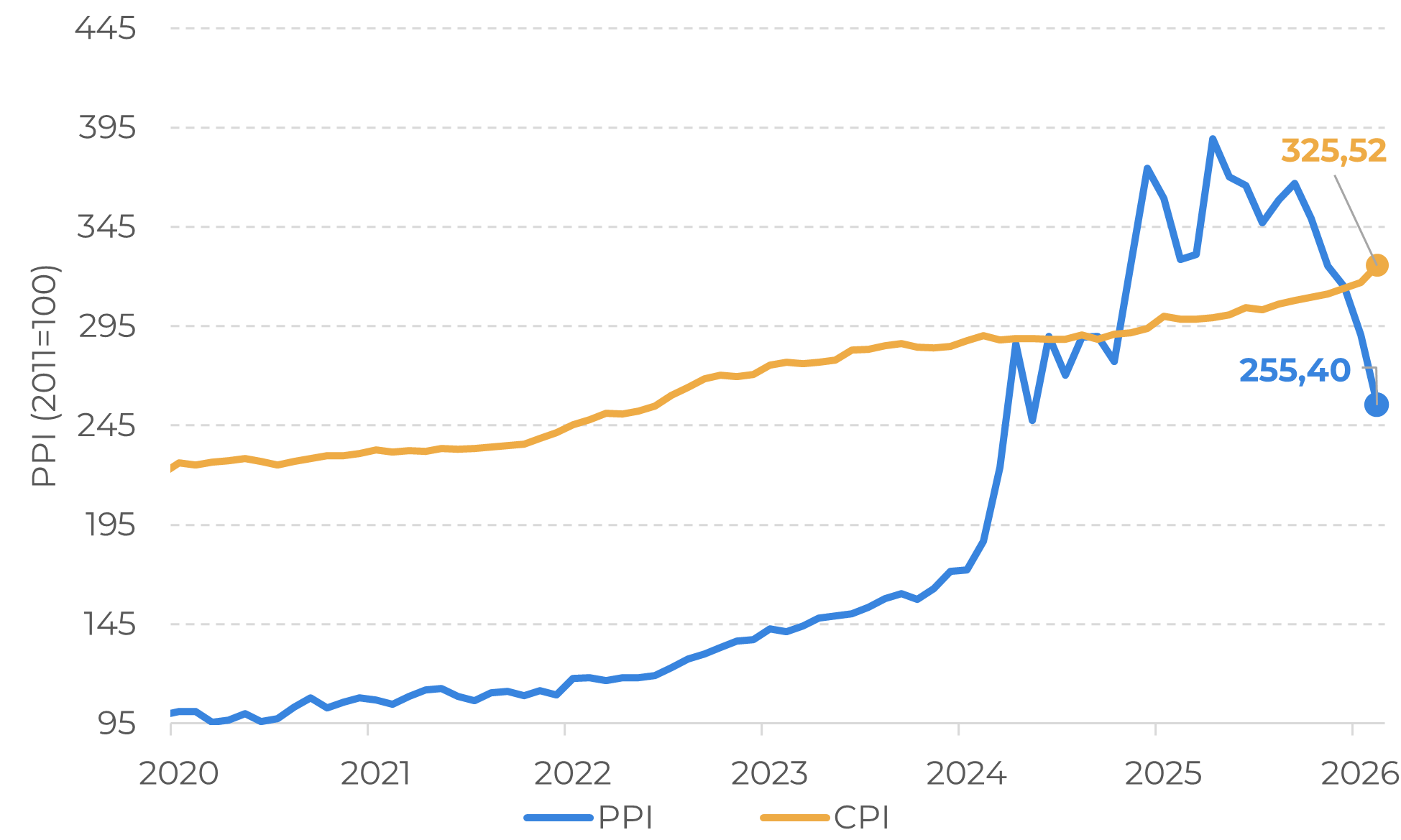

Price indicators reinforce this assessment. In Europe, the Harmonized Index of Consumer Prices shows that cocoa-based products remain at high levels, reaching their highest point in recent years. In the US, the Producer Price Index by Industry, which indirectly signals consumer price trends, also remains elevated, despite some recent corrections. The same is true of the Consumer Price Index for sugar and sweets, which complements this picture. Thus, even with the sharp drop in beans prices on the international market, the effects of this decline have not yet been fully passed on to final consumption.

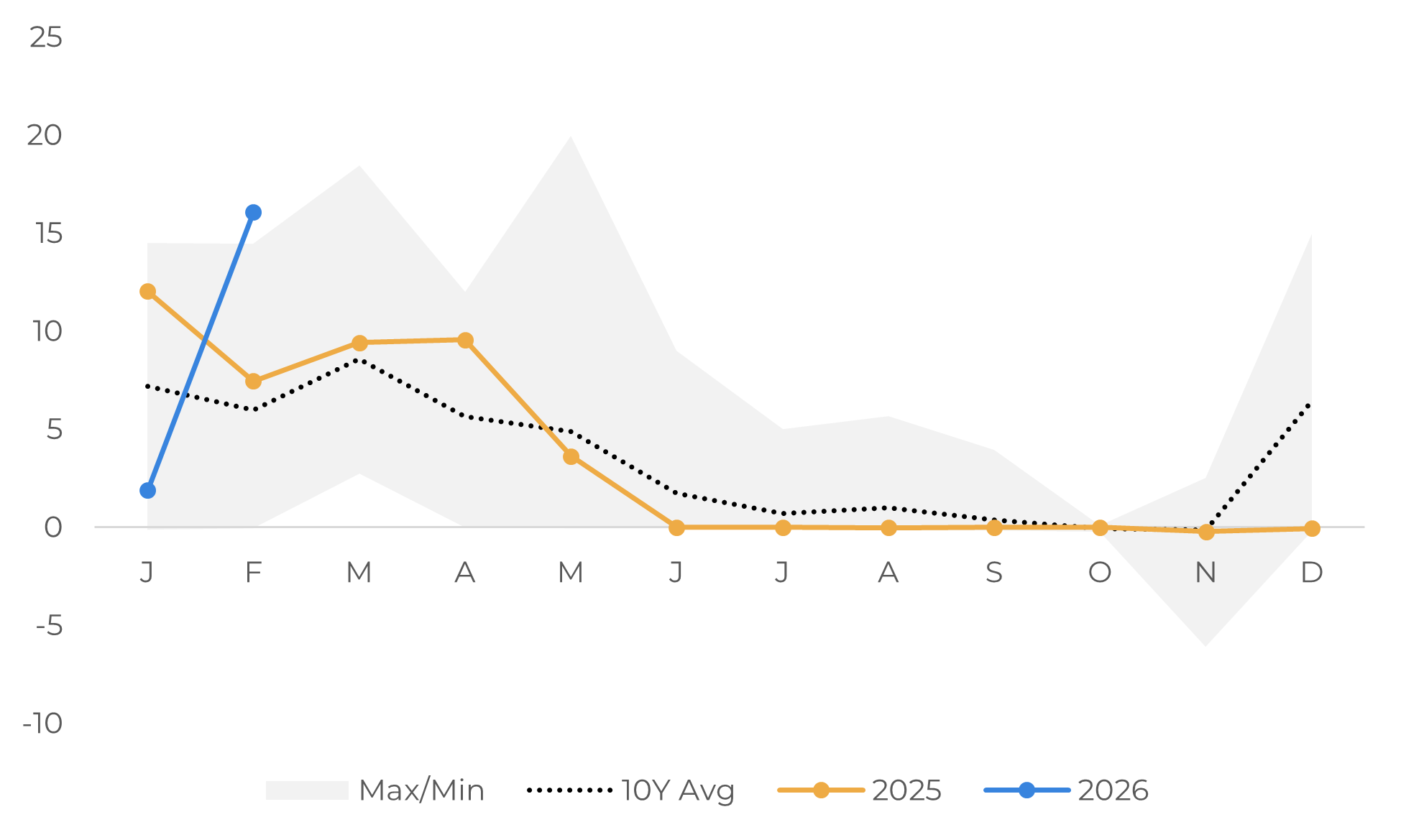

Europe: Harmonized Index of Consumer Prices (HICP) for chocolate and cocoa products

Source: Eurostat

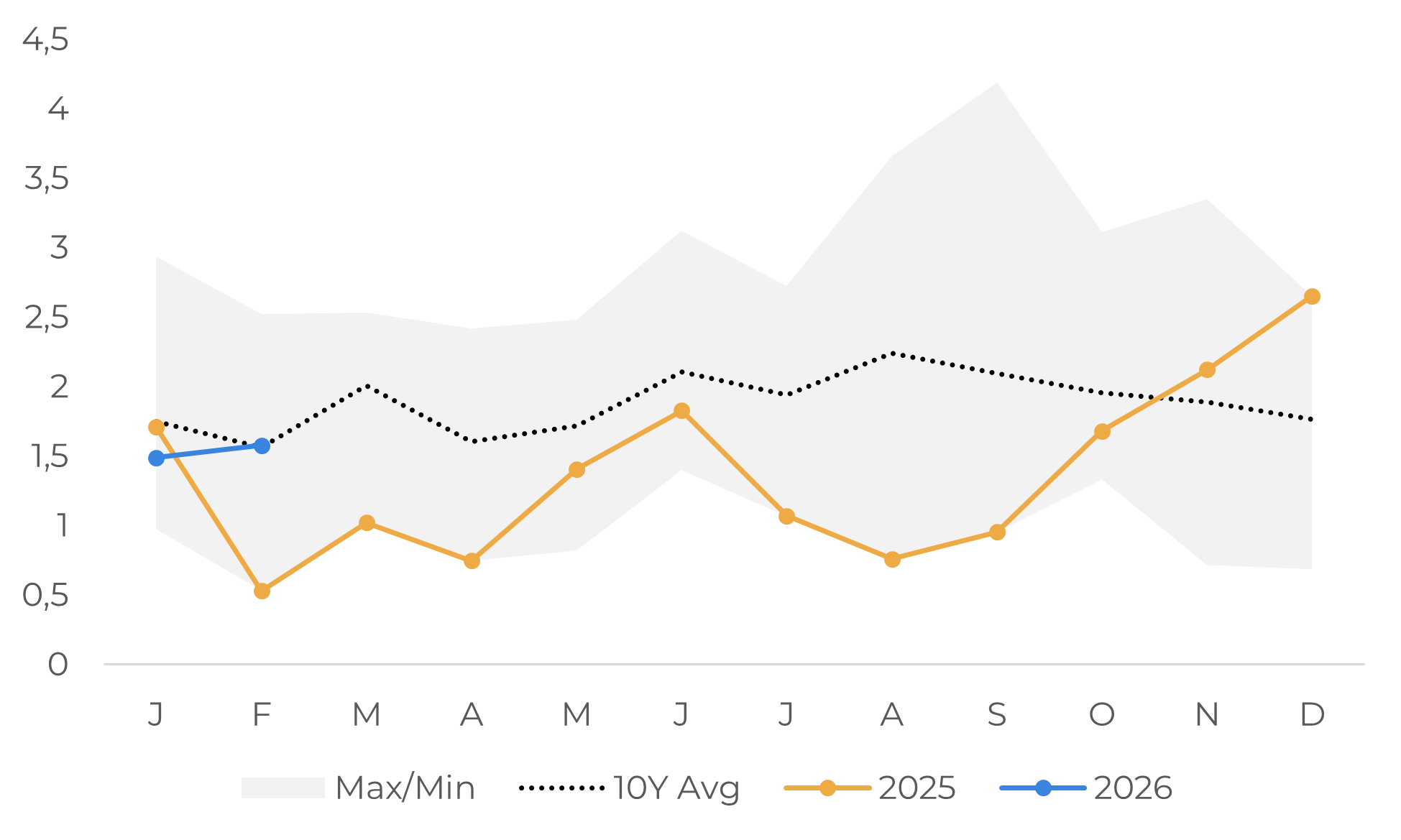

US: Producer Price Index for the chocolate and confectionery manufacturing sector, and Consumer Price Index for sugar and sweets

Source: Federal Reserve Economic Data, U.S. Bureau of Labor Statistics

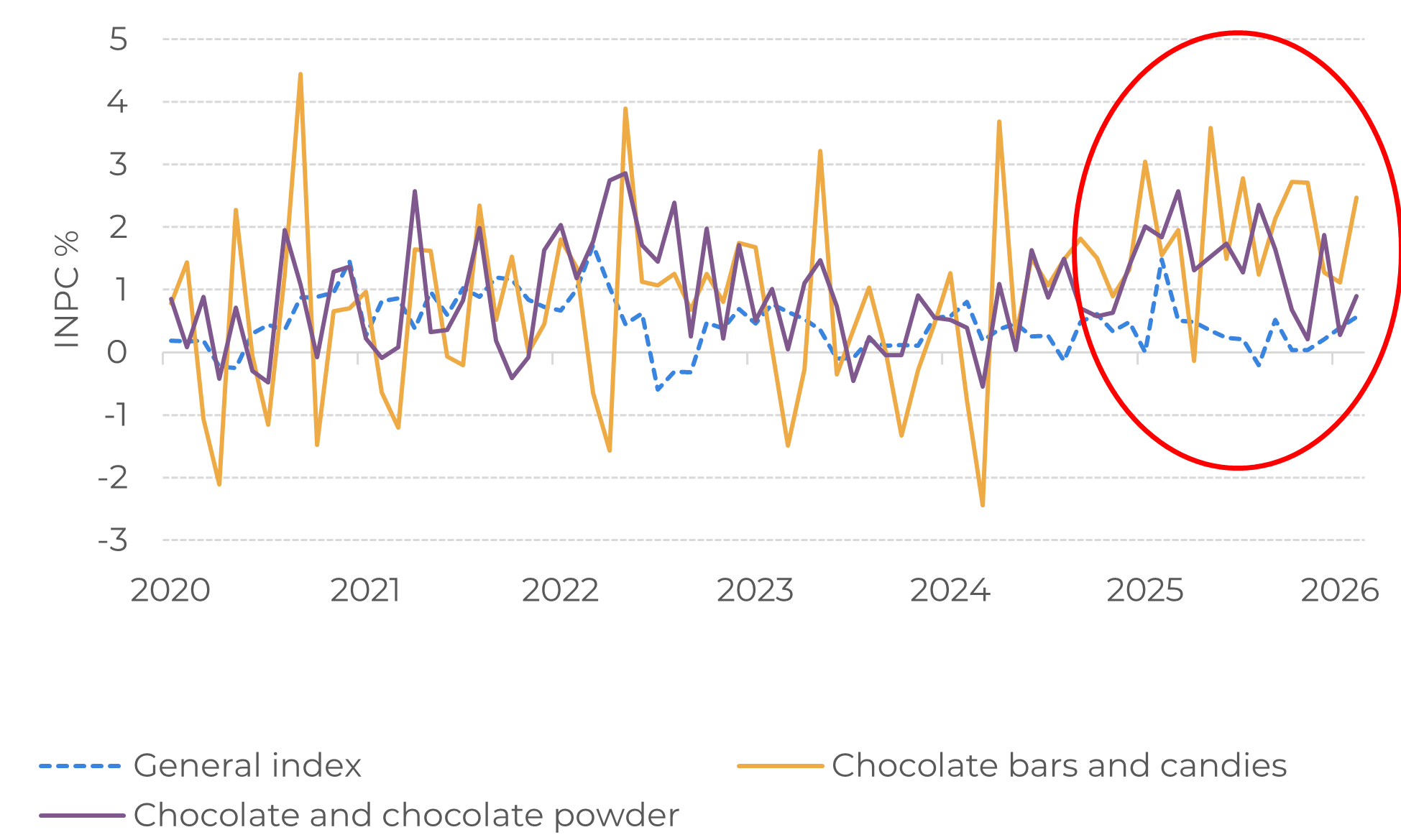

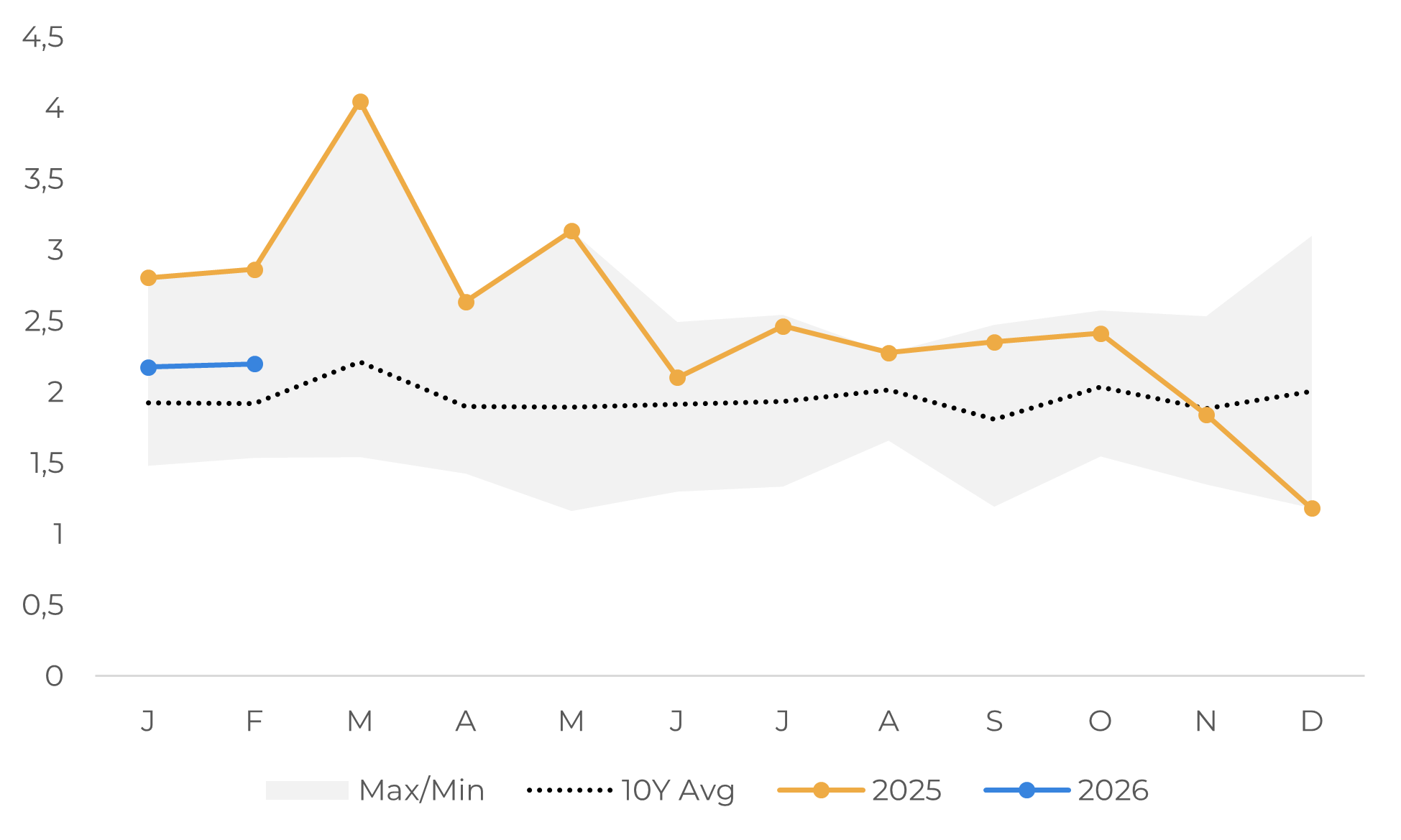

In Brazil, a country where Easter also plays a significant role in chocolate consumption, the holiday tends to be equally bittersweet from a pricing perspective. Data show that products such as chocolate bars and candies have seen price increases exceeding the National Consumer Price Index. Thus, even with the recent correction in international prices, Brazilian consumers are still likely to face higher prices this Easter.

Brazil: National Consumer Price Index (INPC)

Source: IBGE

Trade Flows

Beyond its importance in consumption, Brazil also holds a significant position in the global cocoa industry. Taking a broader view of the last five seasons, the country ranks eighth in the world in cocoa processing. This role makes recent discussions about Brazil’s cocoa trade flows even more relevant, especially at a time when the sector is already facing challenges related to costs, supply, and demand.

In this regard, recent developments have drawn attention within the sector. The suspension of cocoa bean imports from Ivory Coast and changes to the drawback regime, the primary mechanism used for importing cocoa beans intended for processing and subsequent export of derivatives, are heightening concerns regarding the country’s cocoa processing activity.

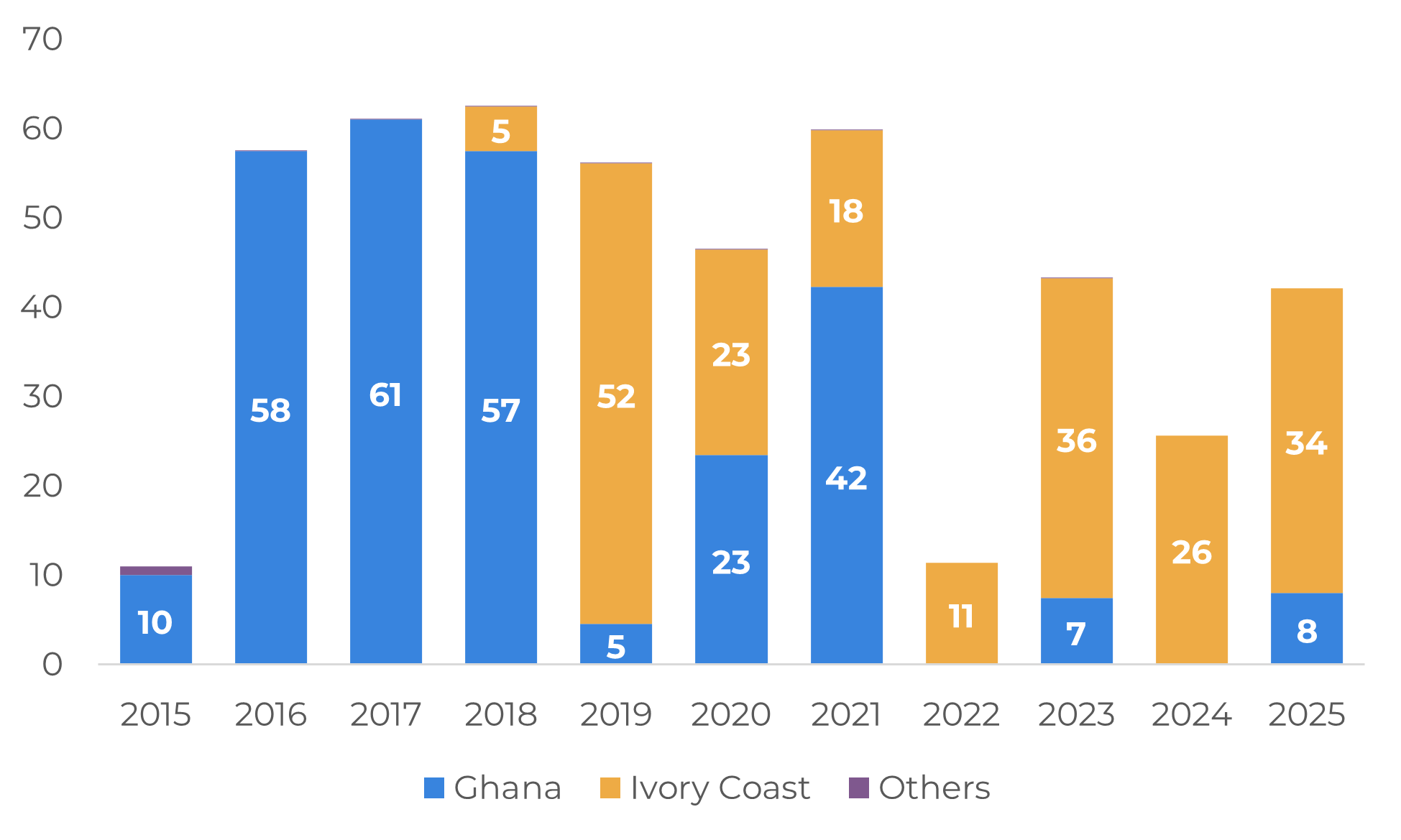

This concern stems from the fact that Brazil has a processing capacity that exceeds its domestic production and, as a result, relies on imports to supplement the industry’s supply. Over the past five years, an average of 17% of the beans processed in the country came from the external market. Of this volume, about 80% originated in Ivory Coast, a share that reached 100% in 2024, while the remainder came mainly from Ghana. Thus, any change that restricts or hinders this flow tends to have a significant impact on the domestic industry. In this scenario, recent measures have heightened market concerns, even at a time marked by lower domestic raw material prices , reports of higher inventories, and elevated imports in February, following a weaker start to the year in January.

Brazil: cocoa beans imports by origin (‘000 tons)

Source: Comex Stat

Brazil: net cocoa bean imports (‘000 tons)

Source: Comex Stat

When assessing Brazilian exports of cocoa powder and butter, which together accounted for an average of 86% of the country’s cocoa derivative exports in recent years, a mixed trend is observed at the start of 2026. Powder exports fell 23% year-over-year between January and February 2026, while cocoa butter exports rose 37% over the same period.

Brazil: cocoa butter exports (‘000 tons)

Source: Comex Stat

This trend contrasts with that observed throughout 2025, when total cocoa powder exports grew by 21% and cocoa butter exports declined by 13%. Assessing the situation, this difference may reflect the effects of market prices and industry adjustments, including changes in formulation and product mix. Still, it is also important to consider that the beginning of 2025 saw, in the case of powder, one of the highest export volumes of the past ten years, which raises the comparison base for 2026.

Brazil: cocoa powder exports (‘000 tons)

Source: Comex Stat

Thus, the announced measures regarding imports come at a particularly sensitive time. Even with cocoa powder and butter exports still above the historical average in February, the sector is now monitoring additional uncertainties regarding the supply of cocoa beans, trade flows, and industrial output. As a result, a scenario that already demanded attention remains challenging in the medium and long term.

In summary, this year’s Easter reinforces a bittersweet outlook for the cocoa market. Although the recent correction in international prices may signal some relief ahead, the effects have not yet clearly reached the final consumer, while the industry continues to face an environment of weakened demand and additional challenges for supply and operations in Brazil.

In Summary

In the week of March 27, cocoa futures gave back some of their previous gains and continued to fluctuate within a narrower range, in a predominantly technical movement also influenced by the macroeconomic and energy backdrop. On the eve of Easter, although international cocoa bean prices are well below last year’s levels, consumers are still likely to find more expensive chocolates, as price adjustments to the final consumer continue to reflect higher previous costs. In Brazil, in addition to this pricing context, the industry is closely monitoring discussions on imports and drawback, at a time when the country relies on imported beans to supplement its domestic production and sustain a significant portion of its derivative exports.

Weekly Report — Cocoa

carolina.frança@hedgepointglobal.com

livea.coda@hedgepointglobal.com

Disclaimer

This document has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without intending to create obligations or commitments to third parties. It is not intended to promote or solicit an offer for the sale or purchase of any securities, commodities interests, or investment products. Hedgepoint and its associates expressly disclaim any liability for the use of the information contained herein that directly or indirectly results in any kind of damages. Information is obtained from sources which we believe to be reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. The trading of commodities interests, such as futures, options, and swaps, involves substantial risk of loss and may not be suitable for all investors. You should carefully consider wither such trading is suitable for you in light of your financial condition. Past performance is not necessarily indicative of future results. Customers should rely on their own independent judgment and/or consult advisors before entering into any transactions. Hedgepoint does not provide legal, tax or accounting advice and you are responsible for seeking any such advice separately. Hedgepoint Schweiz AG is organized, incorporated, and existing under the laws of Switzerland, is filiated to ARIF, the Association Romande des Intermédiaires Financiers, which is a FINMA-authorized Self-Regulatory Organization. Hedgepoint Commodities LLC is organized, incorporated, and existing under the laws of the USA, and is authorized and regulated by the Commodity Futures Trading Commission (CFTC) and a member of the National Futures Association (NFA) to act as an Introducing Broker and Commodity Trading Advisor. HedgePoint Global Markets Limited is Regulated by the Dubai Financial Services Authority. The content is directed at Professional Clients and not Retail Clients. Hedgepoint Global Markets PTE. Ltd is organized, incorporated, and existing under the laws of Singapore, exempted from obtaining a financial services license as per the Second Schedule of the Securities and Futures (Licensing and Conduct of Business) Act, by the Monetary Authority of Singapore (MAS). Hedgepoint Global Markets DTVM Ltda. is authorized and regulated in Brazil by the Central Bank of Brazil (BCB) and the Brazilian Securities Commission (CVM). Hedgepoint Serviços Ltda. is organized, incorporated, and existing under the laws of Brazil. Hedgepoint Global Markets S.A. is organized, incorporated, and existing under the laws of Uruguay. In case of questions not resolved by the first instance of customer contact (client.services@Hedgepointglobal.com), please contact internal ombudsman channel (ombudsman@hedgepointglobal.com – global or ouvidoria@hedgepointglobal.com – Brazil only) or call 0800-8788408 (Brazil only). Integrity, ethics, and transparency are values that guide our culture. To further strengthen our practices, Hedgepoint has a whistleblower channel for employees and third-parties by e-mail ethicline@hedgepointglobal.com or forms Ethic Line – Hedgepoint Global Markets. “HedgePoint” and the “HedgePoint” logo are marks for the exclusive use of HedgePoint and/or its affiliates. Use or reproduction is prohibited, unless expressly authorized by HedgePoint. Furthermore, the use of any other marks in this document has been authorized for identification purposes only. It does not, therefore, imply any rights of HedgePoint in these marks or imply endorsement, association or seal by the owners of these marks with HedgePoint or its affiliates.

Contact us

Check our general terms and important notices.

We have updated our Terms & Conditions to reflect improvements to our platform, data handling practices, and the overall experience we provide to our clients.