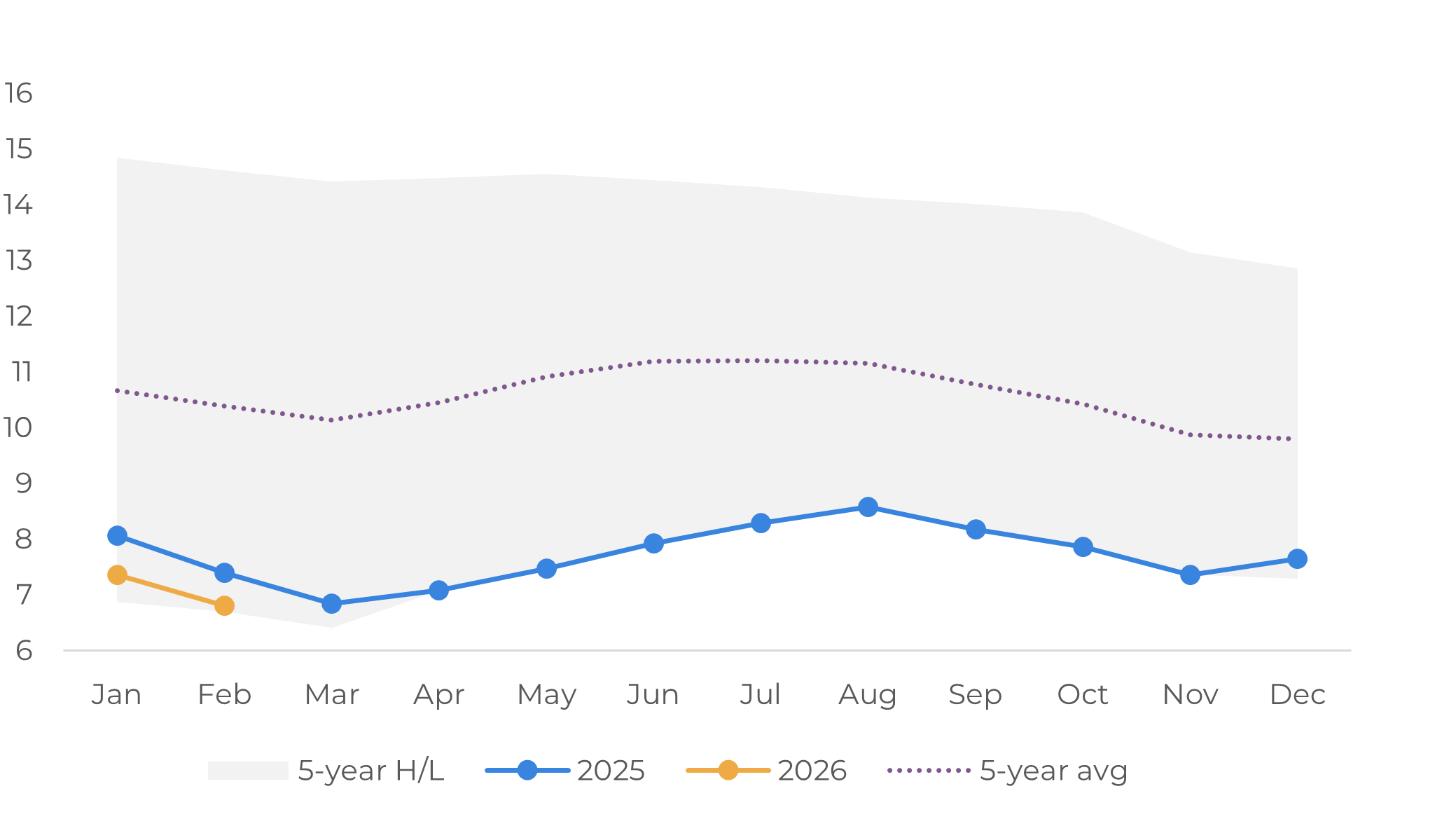

European coffee stocks decline in early 2026 amid weak imports

- The European Coffee Federation stocks fell during the first two months of 2026, reaching their lowest level since March 2024. Inventories declined across all coffee varieties, reflecting lower net imports (imports minus re-exports) in recent months, alongside higher financing costs.

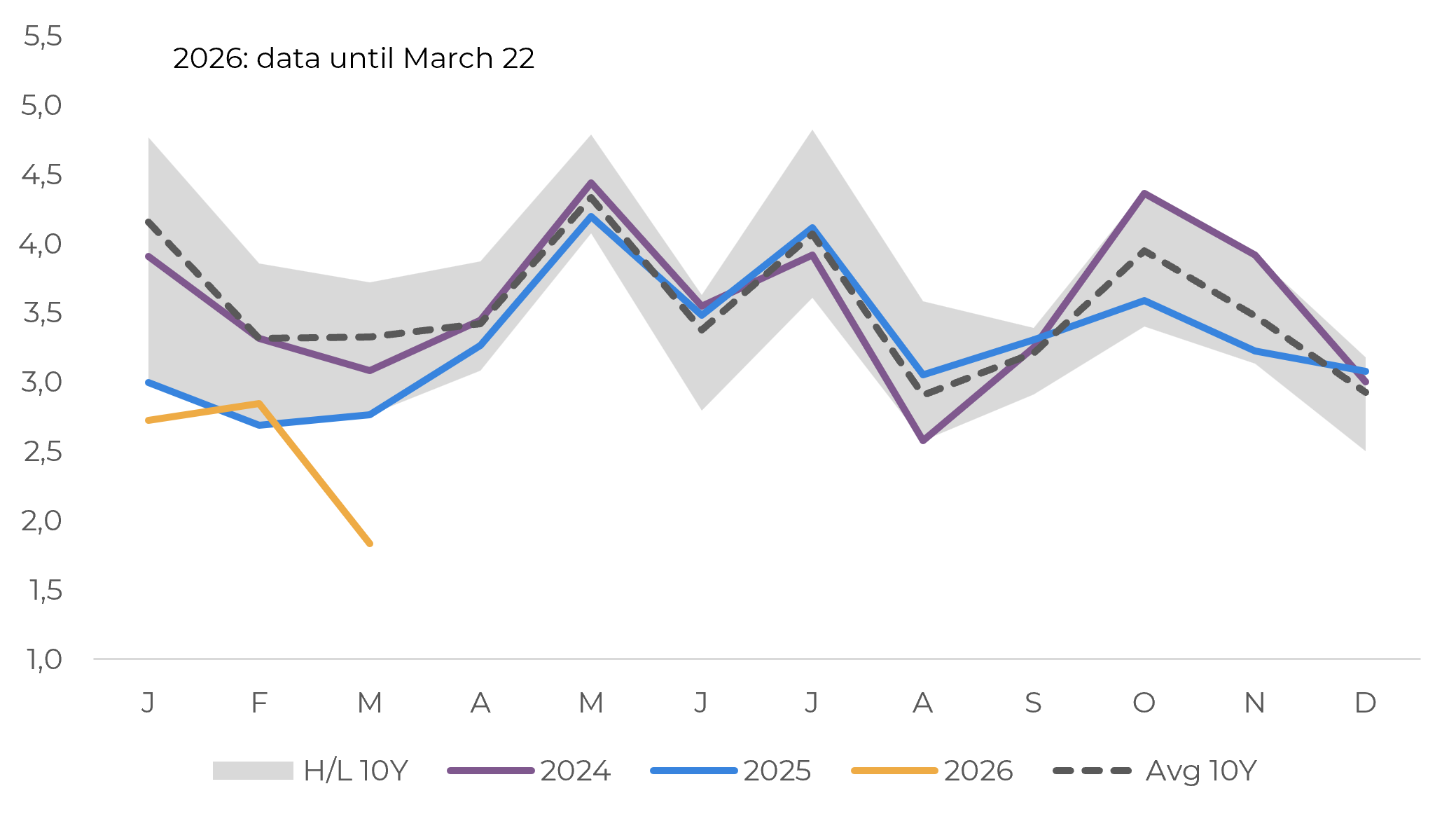

- While total imports remained above historical averages for most of 2025, an increase in re-exports last year reduced net import volumes. Meanwhile, in 2026, imports decreased significantly, further weighing on stock levels.

- At the origins, many farmers - particularly those in Brazil - have become more reluctant sellers following the price downturn since late 2025. With most producing regions currently in the off-season and logistics further strained by the US-Iran conflict, EU imports are likely to remain limited until the Brazilian 26/27 season reaches the market.

- Disappearance figures also point to weakness in the 25/26 cycle, likely to reflect lower net imports in recent months, as elevated coffee prices last year impacted EU demand.

European coffee stocks decline in early 2026 amid weak imports

European Coffee Federation Stocks (M bags)

Source: ECF

European Union Coffee Net Imports (M bags)

Source: European Commission

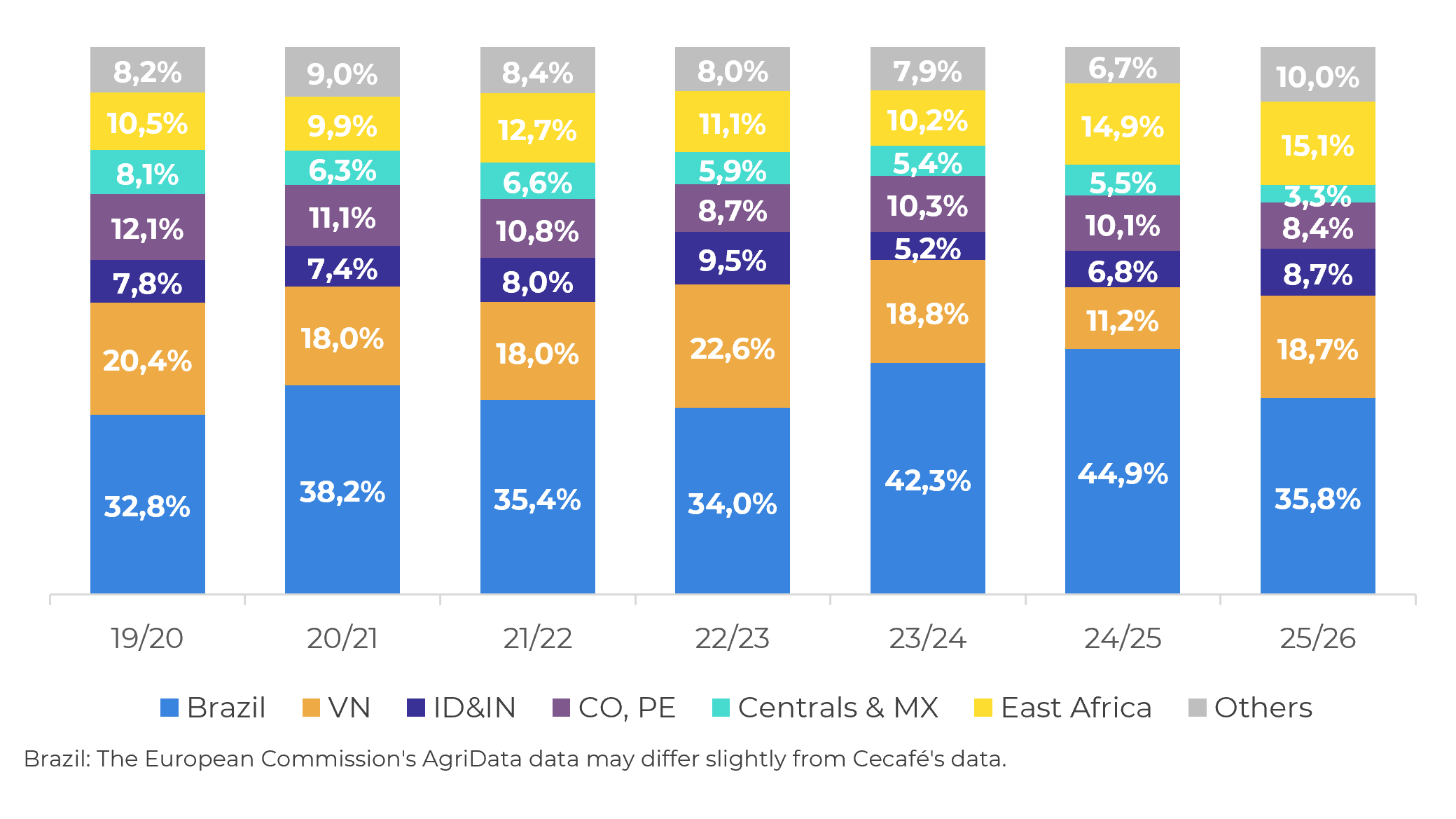

This shift was also reflected in the EU’s import composition. Brazil’s share of EU coffee imports declined compared with the 23/24 and 24/25 seasons, while shipments from other origins gained ground. The most notable increases came from Indonesia and Vietnam, whose export flows moved closer to historical norms. On the other hand, with most producing origins currently in the off-season and logistics constrained by the US–Iran conflict, EU import volumes are likely to remain limited until the arrival of the Brazilian 26/27 crop. In addition, expectations of persistently high financial costs across the coffee market may continue to limit stockholding in destination markets such as the EU, keeping import volumes subdued.

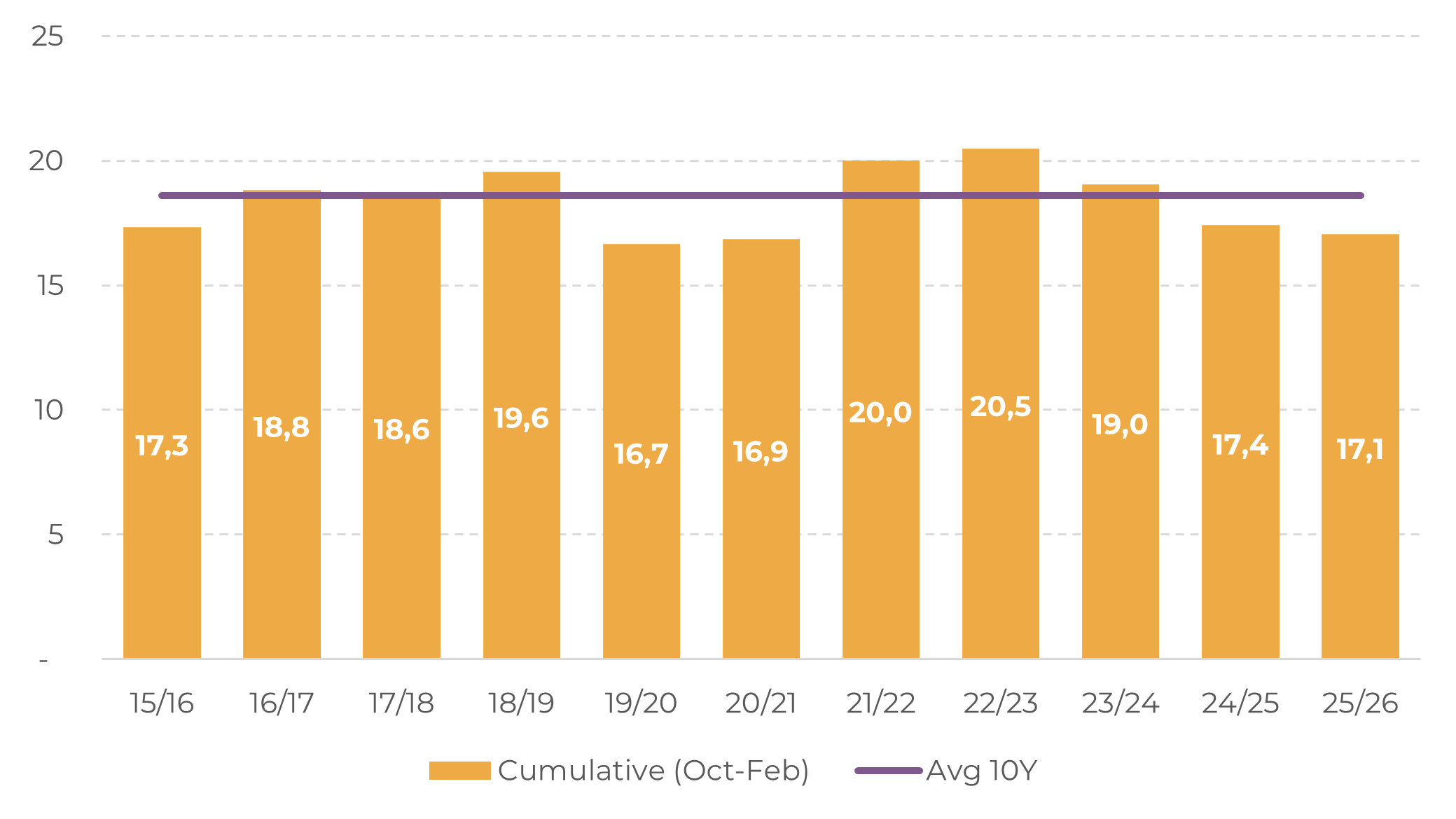

At the same time, the disappearance (or apparent consumption), which measures the balance between stock changes and net imports, points to potential demand-side weakness in the bloc. Cumulative disappearance from October to February of the 25/26 season reached 17.1 million bags, slightly below the 17.4 million bags recorded in the same period of 24/25 and well under the 10-year average of 18.6 million bags. This outcome likely reflects elevated coffee prices in the EU since 2024. The Harmonized Index of Consumer Prices (HICP) for coffee reached successive record highs in 2025, amid rising macroeconomic uncertainty, including US tariffs and their broader economic impacts.

European Union Coffee Imports by Region (Oct-Feb) (M bags)

Source: European Commission

European Union cumulative disappearance (M bags)

Source: ECF, European Commission, Hedgepoint

This trend is also consistent with financial disclosures from major coffee companies in 2025. Several players reported growth in nominal sales revenues, largely driven by higher prices, while volumes declined amid increased consumer price sensitivity. In addition, prolonged price negotiations between coffee companies and retailers across several European markets – particularly in the second half of last year – likely weighed on import demand, reinforcing the downward pressure on stocks observed in recent months.

Looking ahead to 2026, the outlook remains challenging. Escalating geopolitical tensions related to the US–Iran conflict are adding inflationary pressures and raising concerns over a potential stagflationary environment. Higher oil prices are expected to fuel inflation in the EU, while consumer confidence declined sharply in March and employment expectations remain under pressure. Together, these factors are likely to continue capping any near-term recovery in coffee demand, especially as prices remain elevated.

There is, however, some upside potential on the European demand side later this year. As Brazil heads toward a potentially record 26/27 crop, increased supply could help ease prices. That outcome, nonetheless, will largely depend on farmers’ willingness to sell and the pace at which supply materializes in the market.

In Summary

Weekly Report — Coffee

laleska.moda@hedgepointglobal.com

thais.italiani@hedgepointglobal.com

Disclaimer

This document has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without intending to create obligations or commitments to third parties. It is not intended to promote or solicit an offer for the sale or purchase of any securities, commodities interests, or investment products. Hedgepoint and its associates expressly disclaim any liability for the use of the information contained herein that directly or indirectly results in any kind of damages. Information is obtained from sources which we believe to be reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. The trading of commodities interests, such as futures, options, and swaps, involves substantial risk of loss and may not be suitable for all investors. You should carefully consider wither such trading is suitable for you in light of your financial condition. Past performance is not necessarily indicative of future results. Customers should rely on their own independent judgment and/or consult advisors before entering into any transactions. Hedgepoint does not provide legal, tax or accounting advice and you are responsible for seeking any such advice separately. Hedgepoint Schweiz AG is organized, incorporated, and existing under the laws of Switzerland, is filiated to ARIF, the Association Romande des Intermédiaires Financiers, which is a FINMA-authorized Self-Regulatory Organization. Hedgepoint Commodities LLC is organized, incorporated, and existing under the laws of the USA, and is authorized and regulated by the Commodity Futures Trading Commission (CFTC) and a member of the National Futures Association (NFA) to act as an Introducing Broker and Commodity Trading Advisor. HedgePoint Global Markets Limited is Regulated by the Dubai Financial Services Authority. The content is directed at Professional Clients and not Retail Clients. Hedgepoint Global Markets PTE. Ltd is organized, incorporated, and existing under the laws of Singapore, exempted from obtaining a financial services license as per the Second Schedule of the Securities and Futures (Licensing and Conduct of Business) Act, by the Monetary Authority of Singapore (MAS). Hedgepoint Global Markets DTVM Ltda. is authorized and regulated in Brazil by the Central Bank of Brazil (BCB) and the Brazilian Securities Commission (CVM). Hedgepoint Serviços Ltda. is organized, incorporated, and existing under the laws of Brazil. Hedgepoint Global Markets S.A. is organized, incorporated, and existing under the laws of Uruguay. In case of questions not resolved by the first instance of customer contact (client.services@Hedgepointglobal.com), please contact internal ombudsman channel (ombudsman@hedgepointglobal.com – global or ouvidoria@hedgepointglobal.com – Brazil only) or call 0800-8788408 (Brazil only). Integrity, ethics, and transparency are values that guide our culture. To further strengthen our practices, Hedgepoint has a whistleblower channel for employees and third-parties by e-mail ethicline@hedgepointglobal.com or forms Ethic Line – Hedgepoint Global Markets. “HedgePoint” and the “HedgePoint” logo are marks for the exclusive use of HedgePoint and/or its affiliates. Use or reproduction is prohibited, unless expressly authorized by HedgePoint. Furthermore, the use of any other marks in this document has been authorized for identification purposes only. It does not, therefore, imply any rights of HedgePoint in these marks or imply endorsement, association or seal by the owners of these marks with HedgePoint or its affiliates.

Contact us

Check our general terms and important notices.

We have updated our Terms & Conditions to reflect improvements to our platform, data handling practices, and the overall experience we provide to our clients.