Middle East conflict reshapes energy, freight and sugar market dynamics

- The U.S.–Iran conflict has escalated into a global macro shock, disrupting energy markets, trade routes, and raising geopolitical risk across commodities, including sugar.

- Brent crude surged over 16% as Hormuz traffic stalled and Suez/Red Sea routes were suspended, forcing rerouting via the Cape of Good Hope and sharply increasing freight and insurance costs.

- Sugar trade is indirectly impacted, with longer and costlier routes into the Middle East disrupting flows from Brazil, Central America, and Europe and weakening the reliability of regional refining hubs.

- Higher oil prices raise sugar production and logistics costs globally; India has cut its output outlook, though limited export allowances cap the impact on global trade flows.

- In Brazil, higher energy prices can support ethanol parity, possibly lifting the effective floor for sugar prices and partly offsetting bearish pressures from oversupply and a stronger U.S. dollar.

Middle East conflict reshapes energy, freight, and sugar market dynamics

The current conflict between the United States and Iran represents the most serious escalation in their long-standing rivalry in years and has rapidly evolved from a regional military confrontation into a global economic and trade shock. The crisis intensified in late February 2026 after coordinated U.S. and Israeli strikes targeted Iranian military infrastructure and senior figures, prompting Iran to retaliate.

As hostilities widened, several countries became directly or indirectly involved. Beyond the United States, Iran, and Israel, the conflict has spilled over into neighboring states that host U.S. bases or critical energy assets, including Iraq, Saudi Arabia, the United Arab Emirates, Kuwait, Qatar, and Bahrain. Drone incidents and missile activity have also affected areas near Lebanon, Syria, and Azerbaijan, underscoring the regional nature of the escalation. While not military participants, Europe, Japan, China, and India are deeply exposed due to their dependence on Middle Eastern energy supplies and maritime trade routes.

Thus, global macro and commodity shock, with clear implications for the sugar market. The confrontation has drawn in key Middle Eastern energy producers and disrupted critical maritime routes, sharply increasing geopolitical risk premiums across energy, freight, and currencies.

Energy markets reacted first and most strongly. Brent crude surged more than 20% in a few days as shipping through the Strait of Hormuz, responsible for about one-fifth of global oil and LNG flows, was effectively halted, leaving hundreds of vessels stranded. At the same time, the passage through the Red Sea and the Suez Canal has been suspended, forcing ships to reroute around the Cape of Good Hope. This has increased voyage times, fuel consumption, insurance costs, and freight rates across global trade, including agricultural commodities.

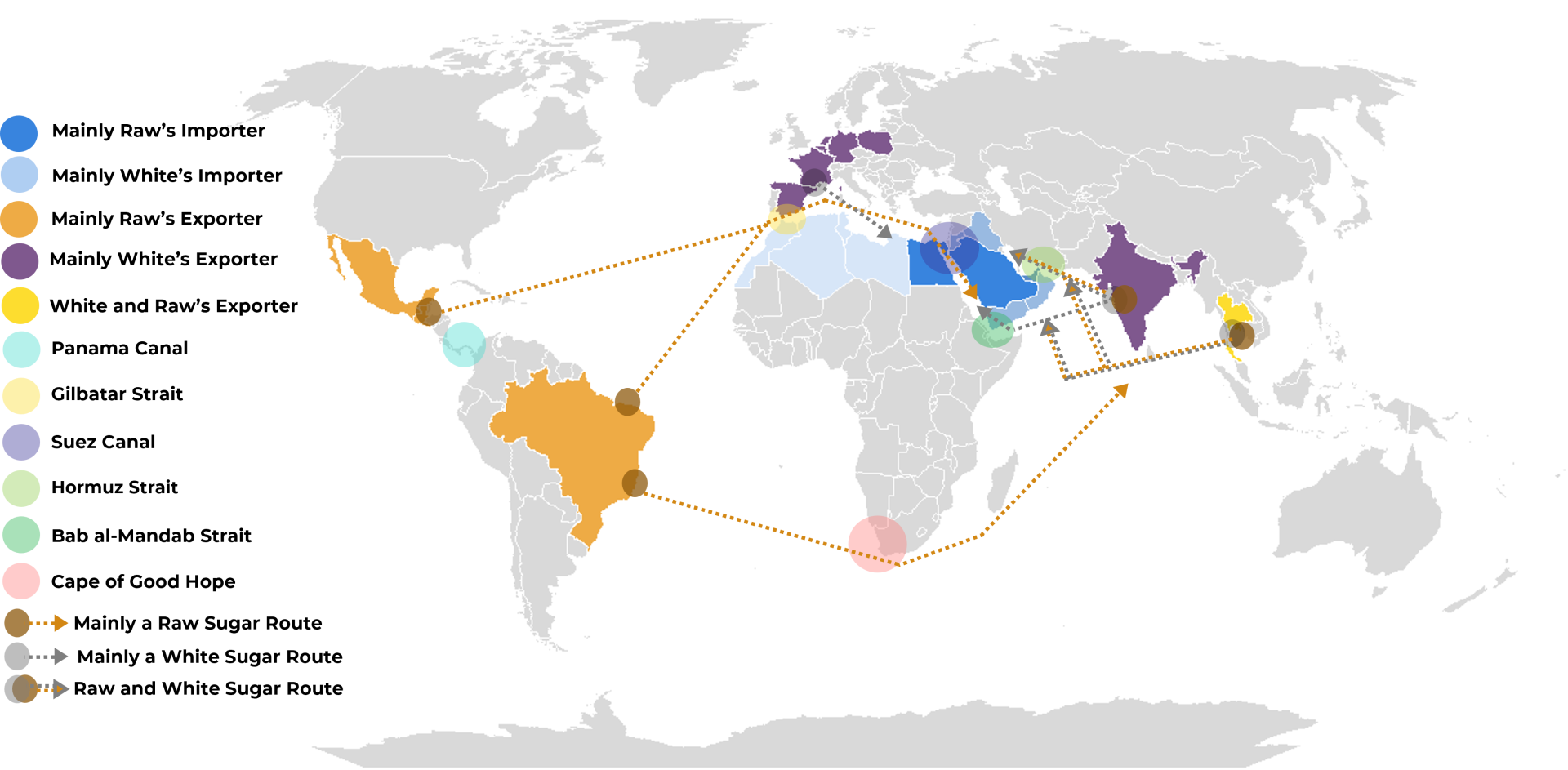

Figure 1 – Main maritime routs that could be disrupted

Source: Hedgepoint

For sugar, the impact is indirect but increasingly relevant. From a logistics perspective, the suspension of traffic through the Suez Canal and the Red Sea has materially altered trade flows into the Middle East. With the main gateway from the Atlantic basin disrupted, shipments from Brazil and Central America, which supply most of the region’s raw sugar imports, are now forced into a longer and more expensive detour around the Cape of Good Hope. The same applies, to a lesser extent, to white sugar exports from Europe, which also rely on Suez as the most efficient route.

These disruptions extend beyond longer transit times and higher freight costs, undermining the operational reliability of key refining hubs in the region. Major refineries, including those in Dubai, are facing increasingly fragile supply chains, regardless of the sugar’s origin, as inbound routes from both the Atlantic basin and Southeast Asia are affected. As a result, the Middle East sugar market is increasingly exposed to higher delivered costs, longer lead times, and elevated logistical uncertainty, even in the absence of any direct impact on physical sugar production.

Higher oil prices also affect the sugar market by raising production and logistics costs throughout the supply chain, from fertilizers and field operations to crushing, refining, and export freight. In oil-importing countries such as India, higher energy costs directly increase the cost base of sugar production and exports, reducing competitiveness and potentially tightening global supply. Elevated freight rates further pressure exporters that rely on long-haul routes to Asia, Africa, and the Middle East.

Besides higher costs, India has revised its production outlook. According to AISTA, abnormal weather patterns and flowering have already weighed on yields, leading to a sharp downward revision in output expectations. Total sugar production is now estimated by the Association at just 31.5 million tons. After accounting for an expected 3.2 million tons diverted to ethanol, final sugar availability is projected at 28.3 million tons, a level significantly lower than initial estimates at the beginning of the season.

However, it is important to note that India’s figures have a limited impact on global trade flows this year, as Brazil is set to achieve another positive result in its 2026/27 season. The Indian government authorized exports of only 1.5 million tons, and even if the country ultimately fails to ship this entire volume, the effect would likely be marginal. In such a scenario, the shortfall could be offset by a higher sugar mix in Brazil, which would help maintain the current bearish bias in the market.

On the other hand, some countries in the region that usually rely on India would now need to seek sugar elsewhere, and, as discussed previously, routes to Asia, Africa, and the Middle East coming from the West could need to detour through the Cape of Good Hope.

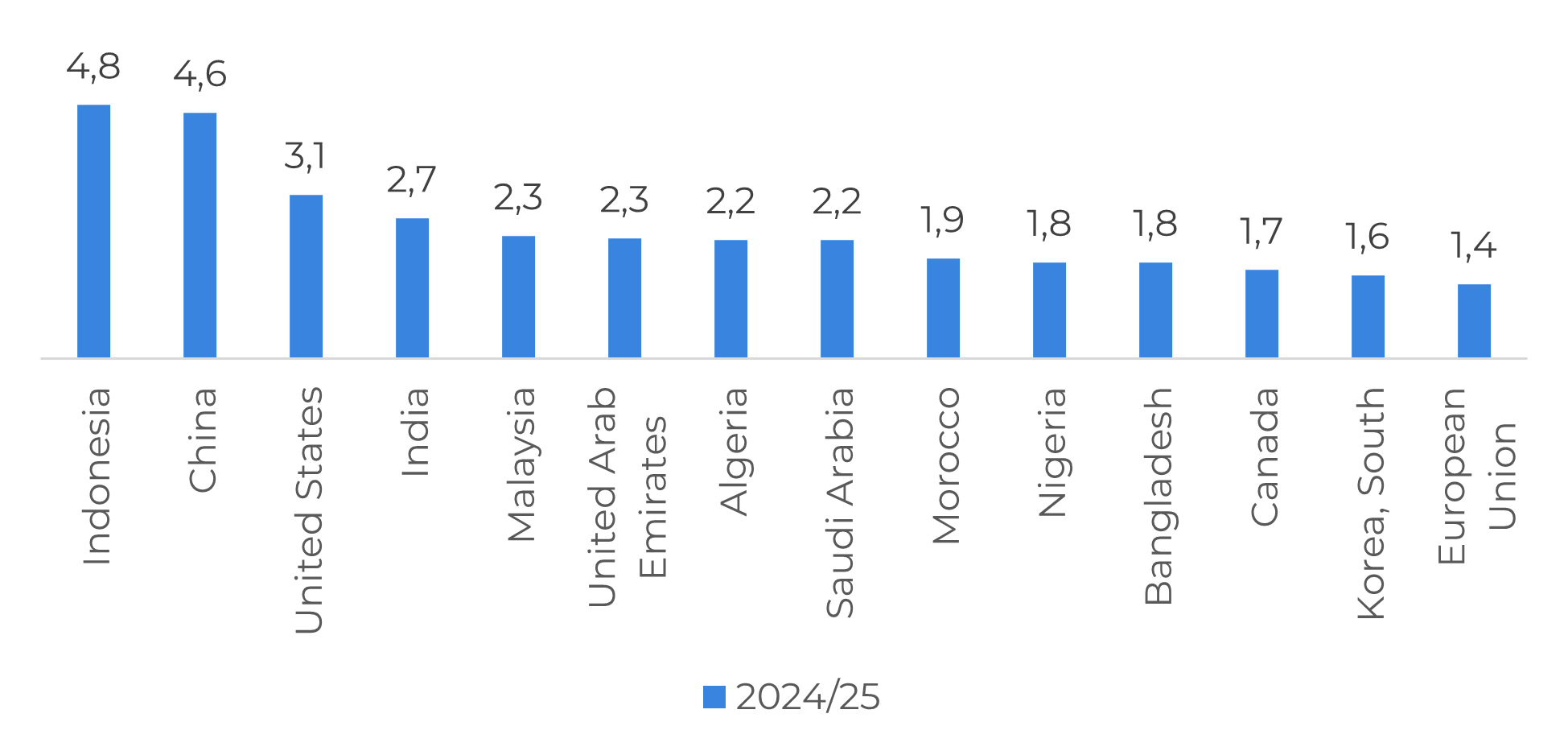

Figure 2 – Top 15 sugar importers in 2024/25 (Mt raw value)

Source: USDA

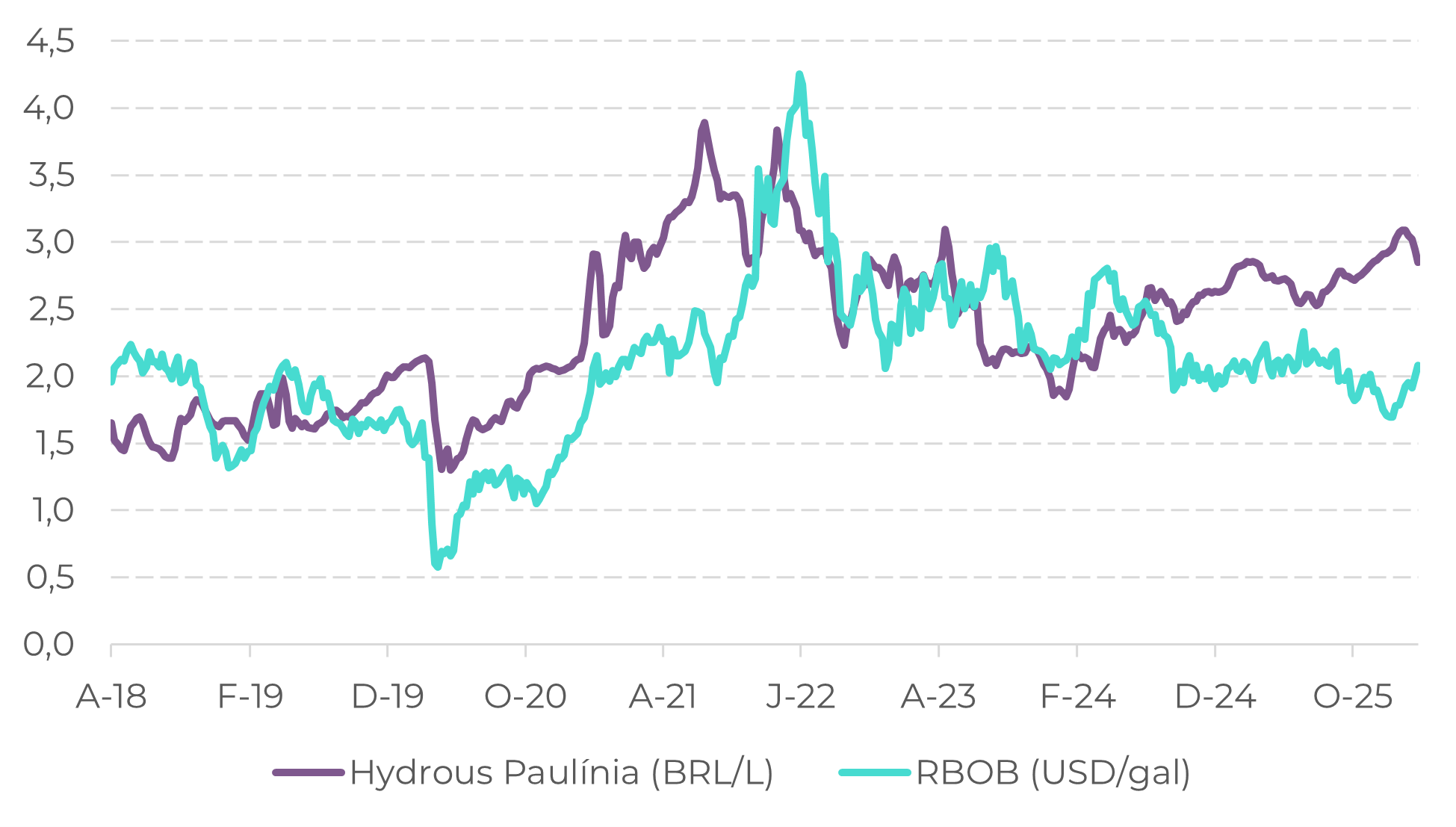

Figure 3 – RBOB vs Hydrous (Weekly CEPEA)

Source: LSEG, CEPEA

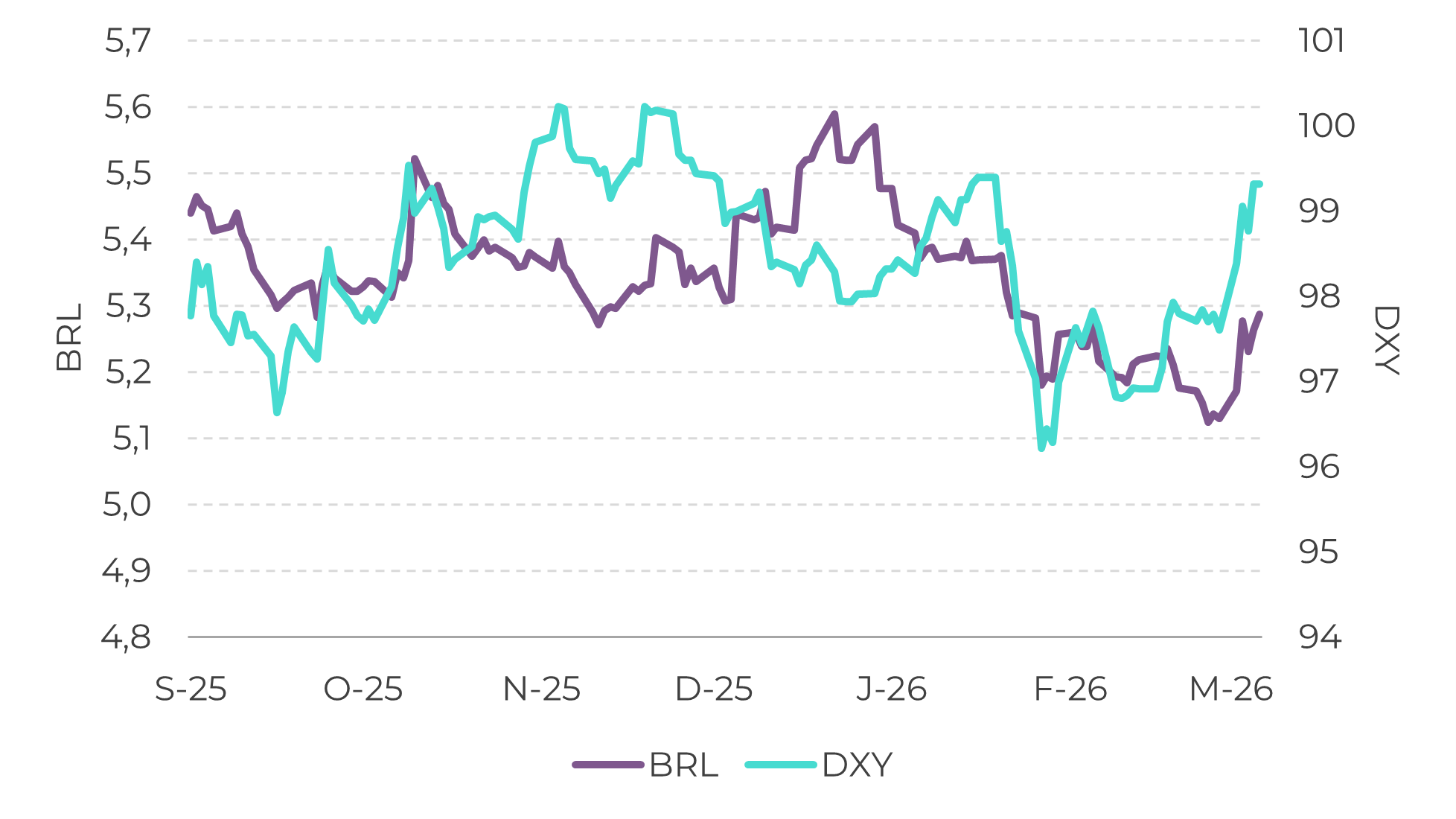

Figure 4 – BRL vs DXY

Source: LSEG

Summary

The conflict increases upside risks for sugar through higher energy costs, supportive ethanol prices in Brazil, rising freight and insurance costs, and potential disruptions to trade routes. Even without direct damage to sugar supply, the current geopolitical shock creates a more inflationary and cost driven environment that is broadly supportive for sugar prices, especially if disruptions in energy and shipping persist.

Weekly Report — Sugar

Reviewed by Laleska Moda

laleska.moda@hedgepointglobal.com

Disclaimer

This document has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without intending to create obligations or commitments to third parties. It is not intended to promote or solicit an offer for the sale or purchase of any securities, commodities interests, or investment products.