Petrobras decisions might shift sugar floor

- Geopolitical tensions and macro uncertainty increased volatility and reinforced risk premiums across commodities.

- US February CPI failed to calm markets, as it predated the oil shock and the USD remained firm.

- Sugar prices spiked early in the week on fund buying and short covering amid Middle East risks and logistical disruptions, then quickly reversed as fundamentals reasserted global oversupply.

- Looking ahead, a sustained rally in energy could support a higher sugar price floor via costs and via changing the Brazilian fuel dynamics, but this support remains fragile and headline‑driven.

Petrobras decisions might shift sugar floor

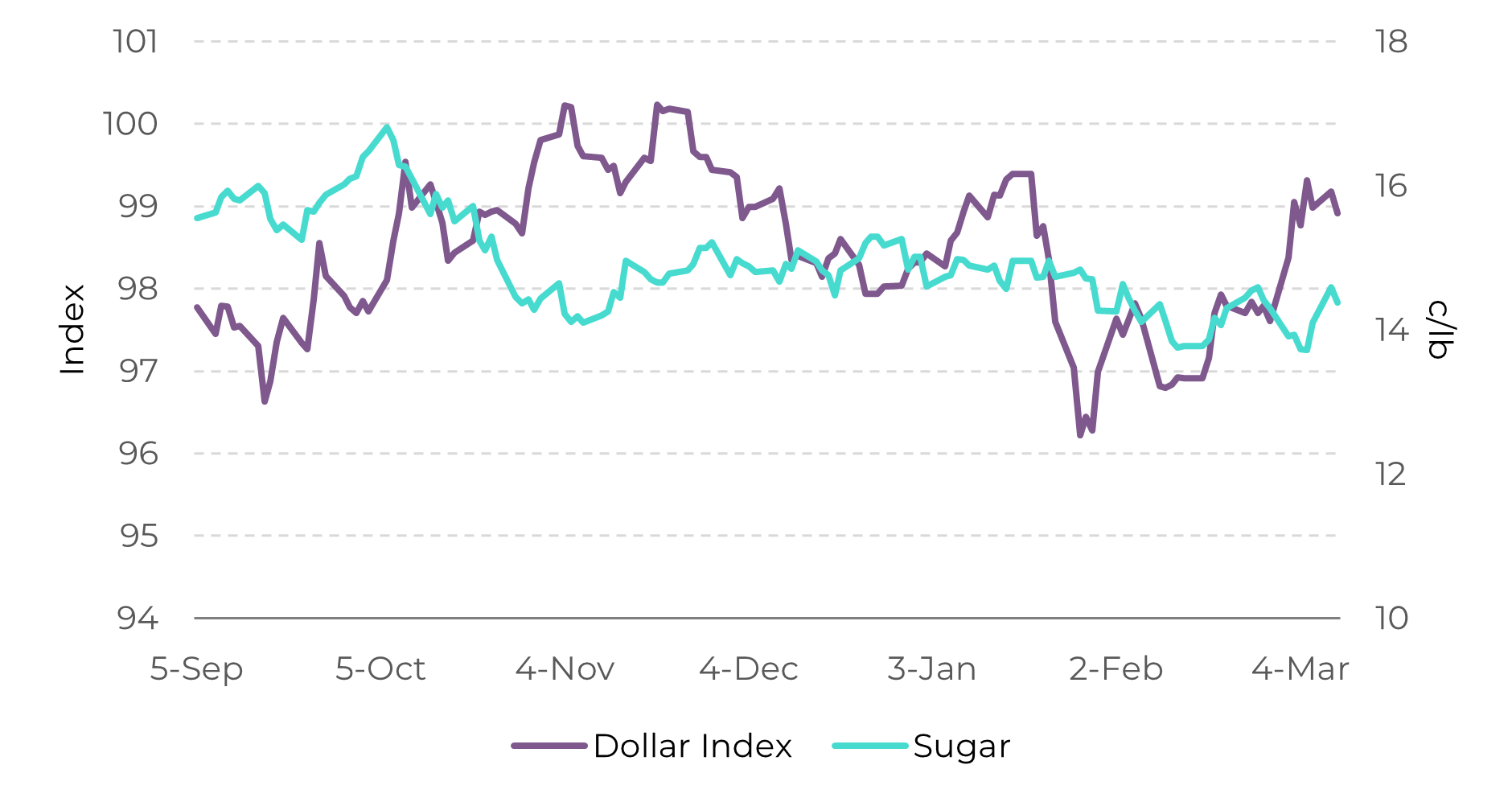

Geopolitics and the macroeconomic environment have taken a toll on the commodities market, adding strong volatility and reinforcing a risk premium environment. Even a US February CPI print in line with expectations failed to soothe markets, as it preceded the oil shock, further strengthening the dollar’s resilience. Meanwhile, firmer energy prices have increased expectations that the Federal Reserve will keep rates unchanged at the March 17–18 FOMC meeting, pushing US Treasury yields higher and further supporting the dollar through the interest rate channel.

Figure 1 – Dollar Index vs Raw Sugar

Source: LSEG

During the week, the sugar market experienced a mild roller coaster. Prices surged sharply on Monday (9) as heightened geopolitical risk in the Middle East triggered fund buying and aggressive short covering – a typical response during periods of elevated risk perception. This move was amplified in the sugar market given the record net short positioning reported by the CFTC. As discussed in our previous report, disruptions to maritime routes, particularly through the Strait of Hormuz, pushed oil prices to levels not seen since 2022, supporting the broader commodity complex via higher cost expectations. Sugar was also directly affected by logistical disruptions, as shipments from Brazil and other origins such as Central America and India into the Middle East faced constraints, which proved supportive not only for raw sugar but for the white market as key refineries, including Al Khaleej from Dubai, sought alternative ports. Raw sugar rose 3.5% to 14.6 c/lb during the session.

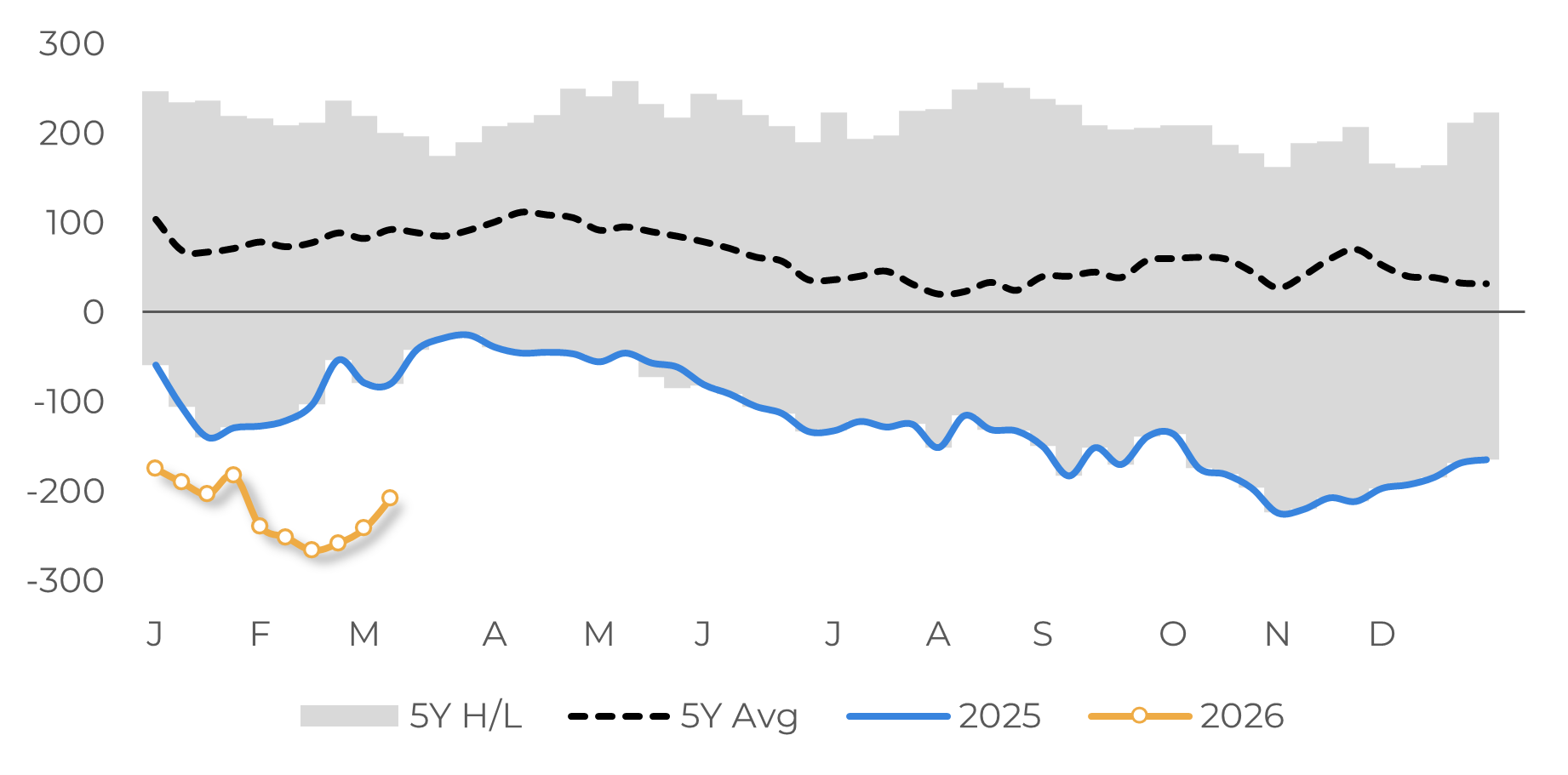

Figure 2 – Raw Sugar Speculative Net Position (‘000 lots)

Source: CFTC

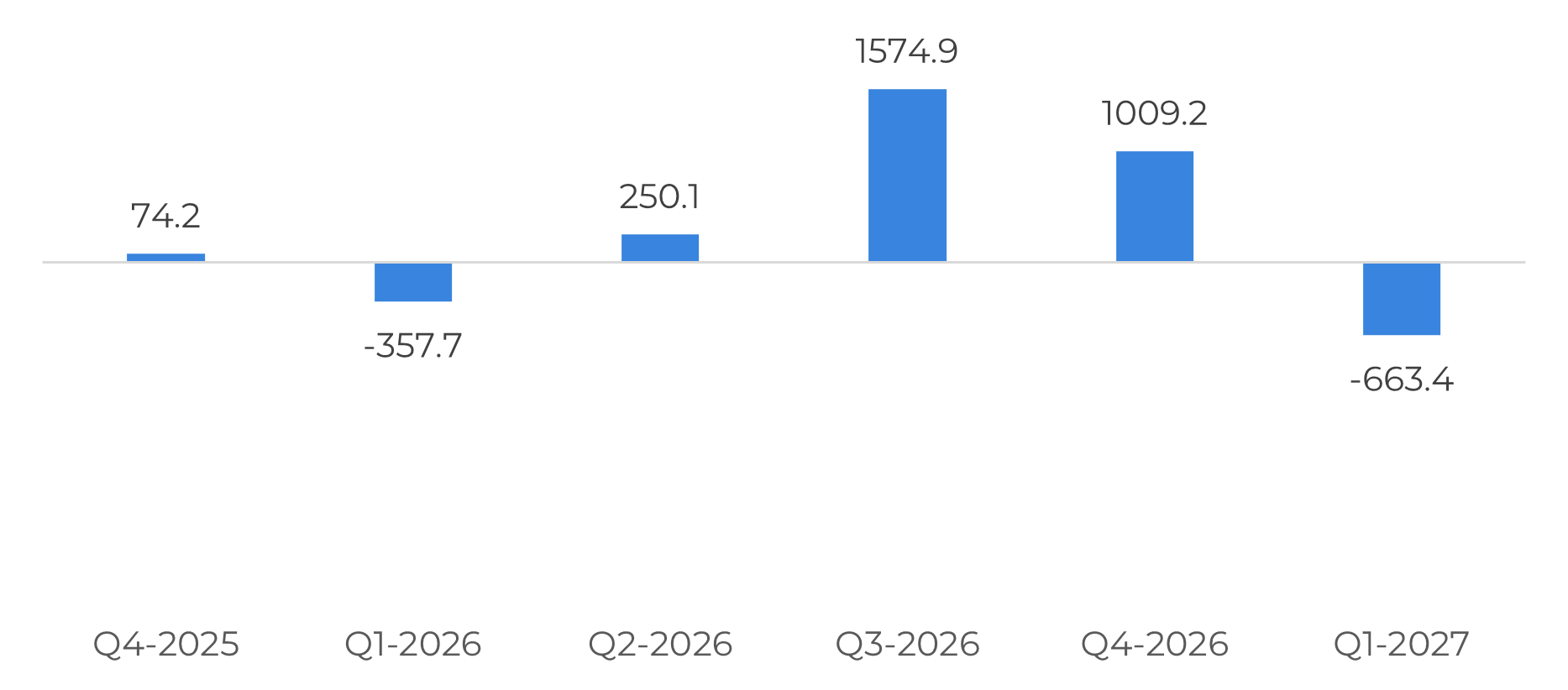

Figure 3 – Raw Sugar Total Trade Flows (‘000t tq)

Source: GreenPool, Hedgepoint

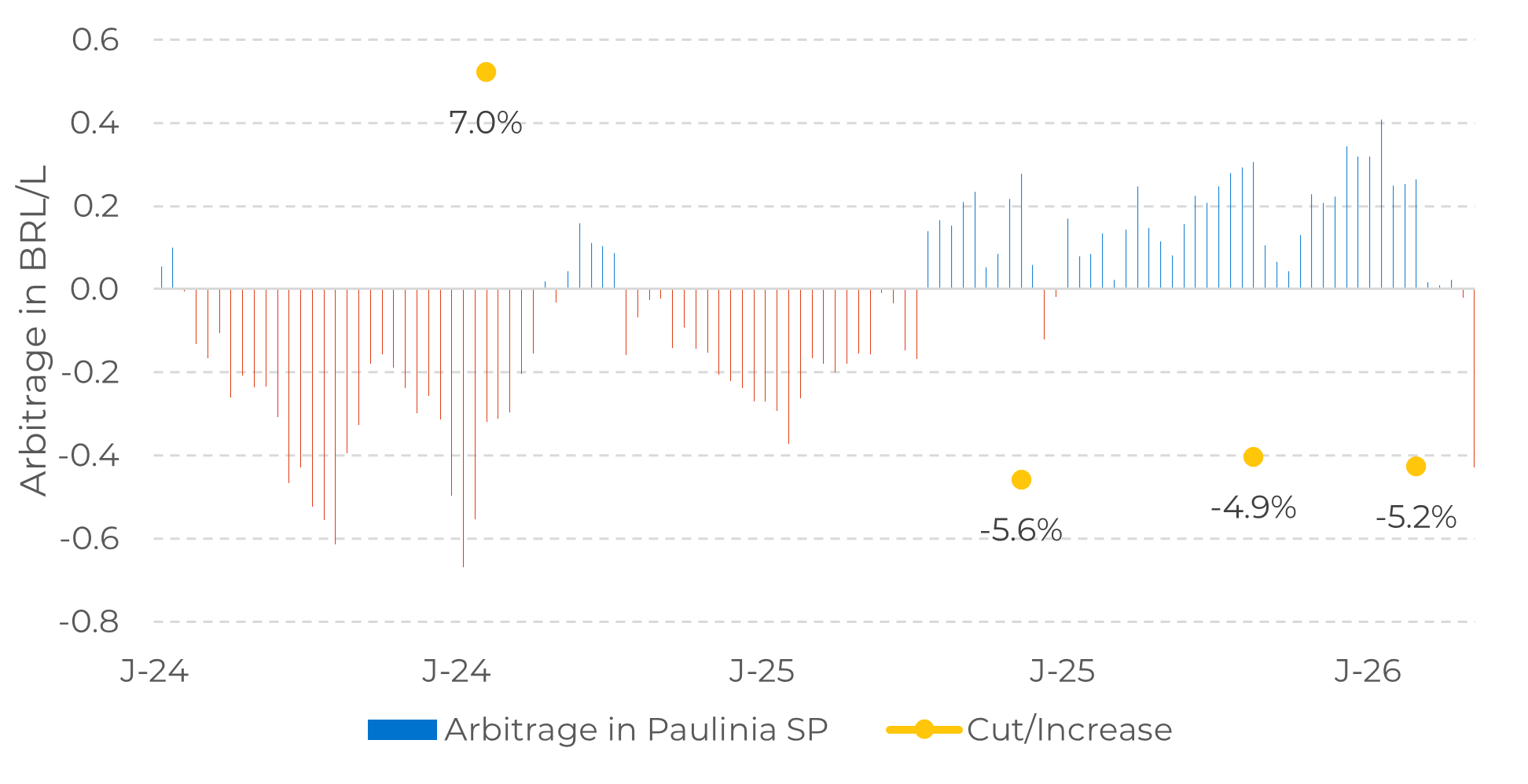

Figure 4 – Petrobras Import Arbitrage History (Paulínia SP)

Source: ANP, Bloomberg, Hedgepoint

Summary

Geopolitical tensions and a fragile macro backdrop drove volatility and reinforced risk premiums across commodities. In sugar, prices spiked early in the week on fund buying and short covering linked to Middle East risks, higher oil prices, and logistical disruptions, before quickly reversing as the move proved largely technical and fundamentals continued to point to global oversupply.

Looking ahead, sustained strength in the energy complex could provide some support to the sugar price floor via higher costs and Brazilian fuel dynamics, but this support would remain fragile, headline driven, and dependent on the duration of the conflict and Petrobras’ pricing decisions.

Weekly Report — Sugar

Reviewed by Laleska Moda

laleska.moda@hedgepointglobal.com

Disclaimer

This document has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without intending to create obligations or commitments to third parties. It is not intended to promote or solicit an offer for the sale or purchase of any securities, commodities interests, or investment products.