Energy risks override bearish fundamentals

- Sugar prices surged on conflict escalation, energy spillovers, and fund short covering.

- Iranian attacks on energy infrastructure lifted oil/LNG prices, boosting global inflation risks.

- Central banks turned cautious: Fed on hold; COPOM cut 25 bp amid a cooling economy.

- Energy-driven cost pressures and firmer ethanol parity may support sugar in the short term.

- Although India has reported lower production prospects, yields in Thailand showed significant improvement.

- Fundamentals remain bearish; support is fragile and conflict-dependent.

Energy risks override bearish fundamentals

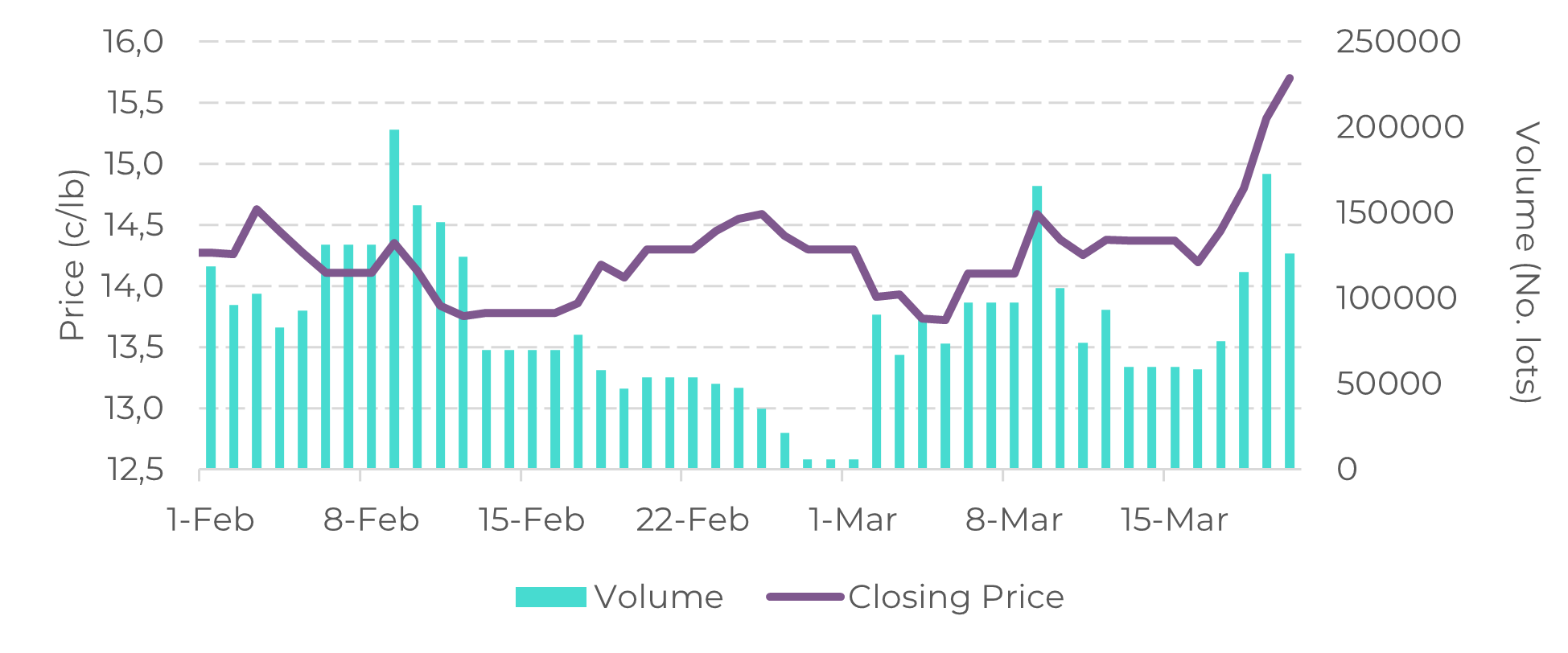

Sugar prices surged during the week amid the intensification of the U.S.-Iran conflict and its spillover into the energy complex, triggering technical buying and fund short covering. On Thursday, 19, this flow pushed the raw contract above the 15 c/lb level, with prices jumping 4.2% on the session, allowing a weekly closure at 15.7 by Friday.

Figure 1 – Raw sugar: a technical movement with plenty of volume

Source: LSEG, Hedgepoint

The move was reinforced by news of Iranian attacks on Qatar’s energy facilities, which further deepened the energy crisis. According to QatarEnergy, roughly 17% of the country’s LNG capacity could be disrupted for at least five years. As a key LNG supplier to Europe and parts of Asia, the disruption raises concerns over renewed economic deterioration and inflationary pressures. Similar attacks on oil infrastructure also drove crude prices higher.

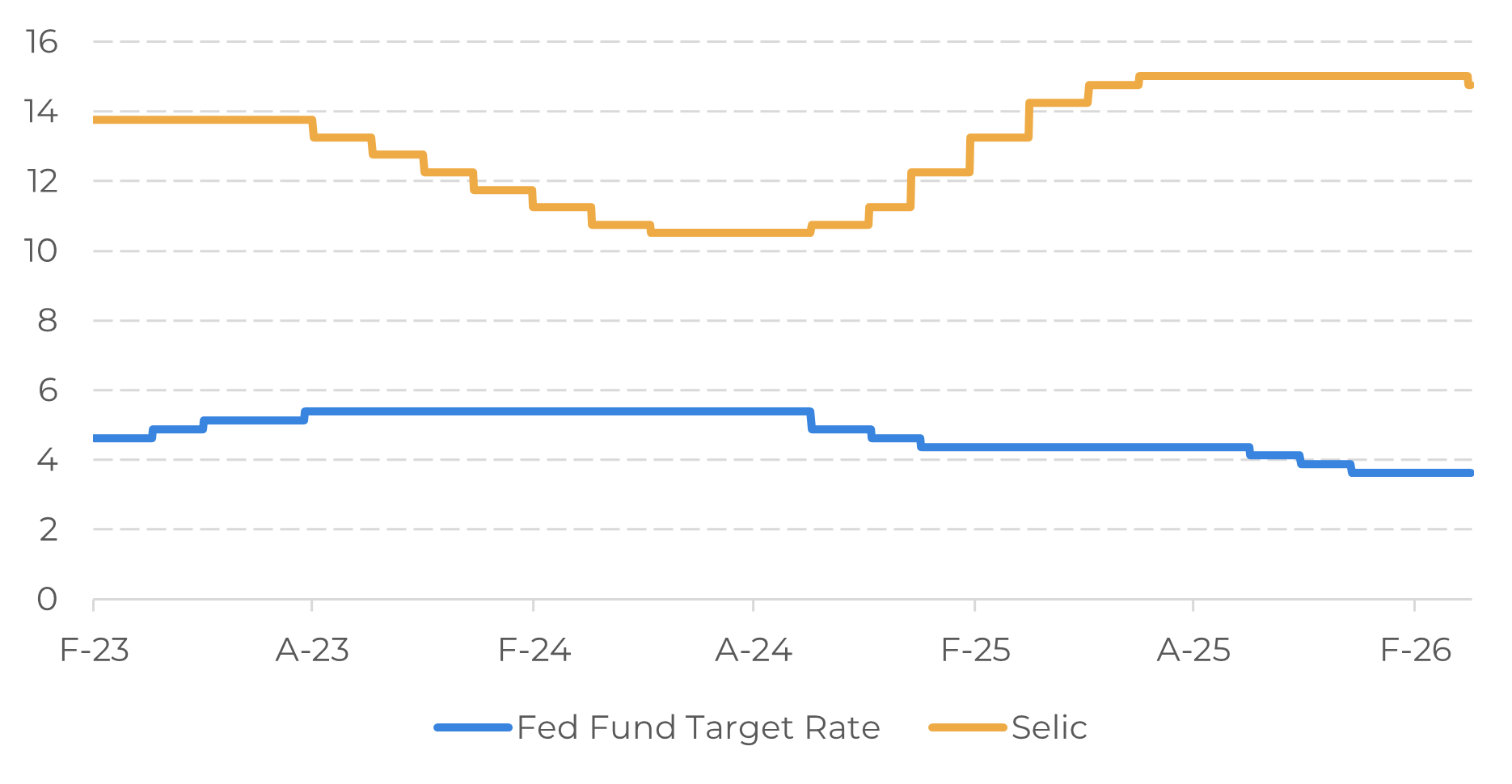

Against this backdrop, central banks have turned more cautious. The Fed highlighted risks of inflation running higher than previously anticipated, which could jeopardize market expectations of a 25 bp rate cut later in 2026 and therefore opted to keep rates unchanged on Wednesday (18). In contrast, Brazil’s COPOM delivered a 25 bp cut on the same day, lowering the Selic rate to 14.75%, citing a cooling economy despite inflation remaining above target. While the interest rate differential may still help keep the BRL supported, heightened geopolitical risk and elevated uncertainty continue to pose challenges for emerging markets.

Figure 2 – Interest rate differential between the US and Brazil (%)

Source: LSEG, Hedgepoint

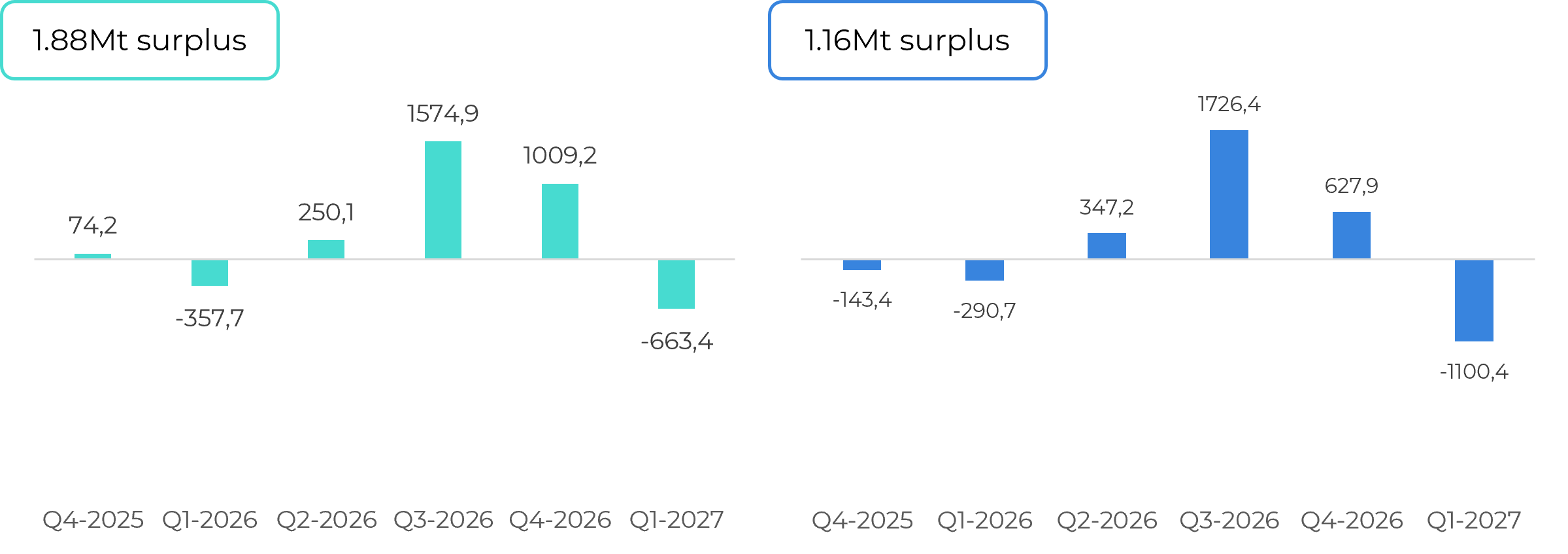

Figure 3 – Total Trade Flow (‘000t tq) – before (left) and after* (right)

Source: GreenPool, Hedgepoint

*After major adjustments to India and Thailand and some residual update to other countries realized data.

Summary

Sugar prices jumped on intensified geopolitics spilling into energy markets, triggering technical buying and fund short covering, but the rally is largely exogenous and fragile. While higher energy and fertilizer costs and firmer Brazilian ethanol parity could offer near-term support, fundamentals remain bearish, with India’s lower output partly offset by improved Thai production and Brazil’s mix flexibility capping rallies. Any de escalation could unwind recent gains.

Weekly Report — Sugar

Reviewed by Laleska Moda

laleska.moda@hedgepointglobal.com

Disclaimer

This document has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without intending to create obligations or commitments to third parties. It is not intended to promote or solicit an offer for the sale or purchase of any securities, commodities interests, or investment products.