Some fundamentals shifts, but no actual change

- No material change in sugar fundamentals, even with some supply developments.

- India's shortfalls could be offset by Thailand and potentially higher Brazilian availability.

- Weather supports upside risks for Brazil’s next crop.

- Recent price support stems from speculative short covering and energy-driven spillovers.

- The 15.4–15.9 c/lb range reflects a temporary balance, with prices likely to fall if energy support fades or geopolitical risks ease.

Some fundamentals shifts, but no actual change

There have been no material changes to the effective fundamentals of the sugar market. Nevertheless, market attention has tilted toward recent supplyside developments. As discussed in our previous report, any reduction in India’s availability could be partially offset by improved prospects in Thailand, or even higher mix from Brazil. Regarding the latter, the latest UNICA release, published on Friday (27), brought figures that allowed us to keep our estimates that the 2025/26 crop could reach approximately 610 Mt of cane, translating into around 40.5 Mt of sugar, depending on the pace of the start of the 2026/27 season. Notably, UNICA has not published data for February, with the most recent report focusing its analysis on the first half of March. This gap raises concerns regarding data availability and consistency for the Center South region.

Even so, weather conditions have been largely supportive of cane development, suggesting potential upside risks to our current 630 Mt estimate for the 2026/27 crop. If confirmed, higher Brazilian availability would reinforce the prevailing bearish fundamentals, as potential disruptions elsewhere could be accommodated through adjustments in the sugar ethanol mix, which is expected to decline in the upcoming season due to prevailing price-dynamics. In fact, Friday’s report already points to a bullish trend for 2026/27, contributing to the short-term rise in prices.

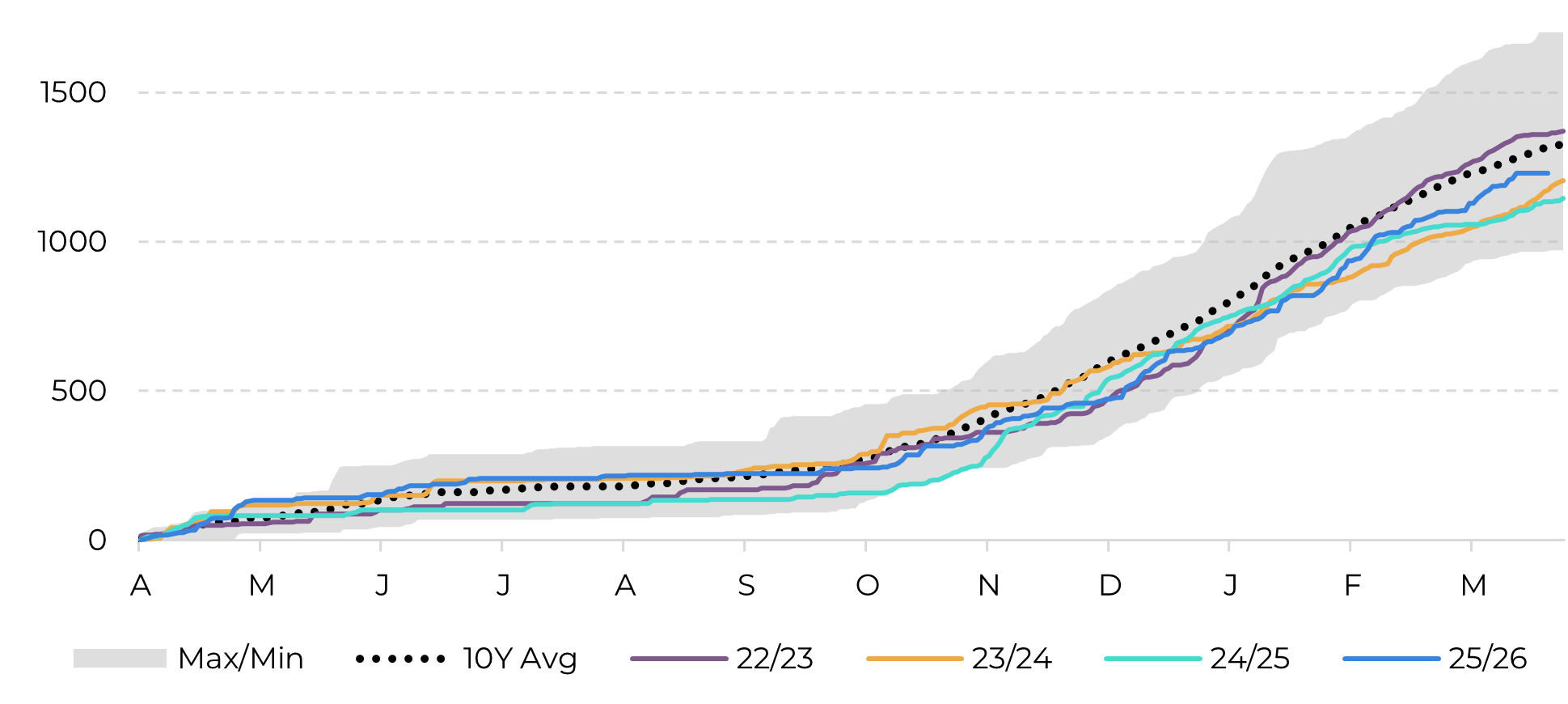

Figure 1 – Center-South Cumulative Precipitation (mm)

Source: Bloomberg, Hedgepoint

Nevertheless, price support has continued to originate primarily from outside the sugar market itself. Last week’s rally was driven largely by short covering by hedge funds, which reduced their positions by more than 100 thousand contracts, according to the CFTC report, which was also updated on Friday, dating movements up until Tuesday (24). For instance, prices reached 15.8 c/lb on Tuesday, accompanied by a rather stable trading volume. However, the market appears to have found resistance near this level, indicating the formation of a short term trading range between 15.4 and 15.9 c/lb. While this range is relatively constructive, it rests on fragile foundations, being driven mainly by speculative positioning amid heightened macroeconomic and geopolitical volatility.

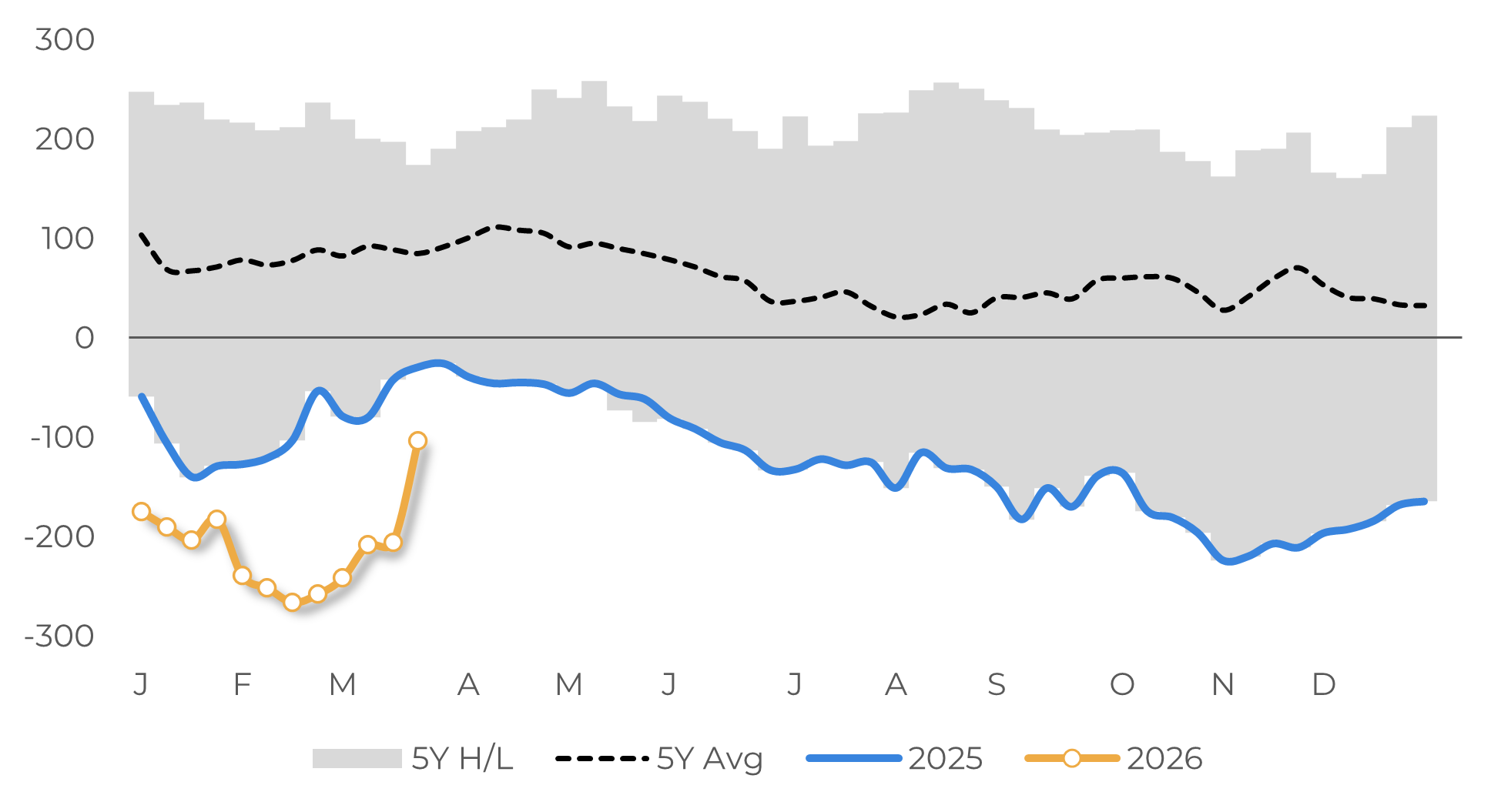

Figure 2 – Speculative Net Positioning (‘000 lots)

Source: CFTC, Hedgepoint

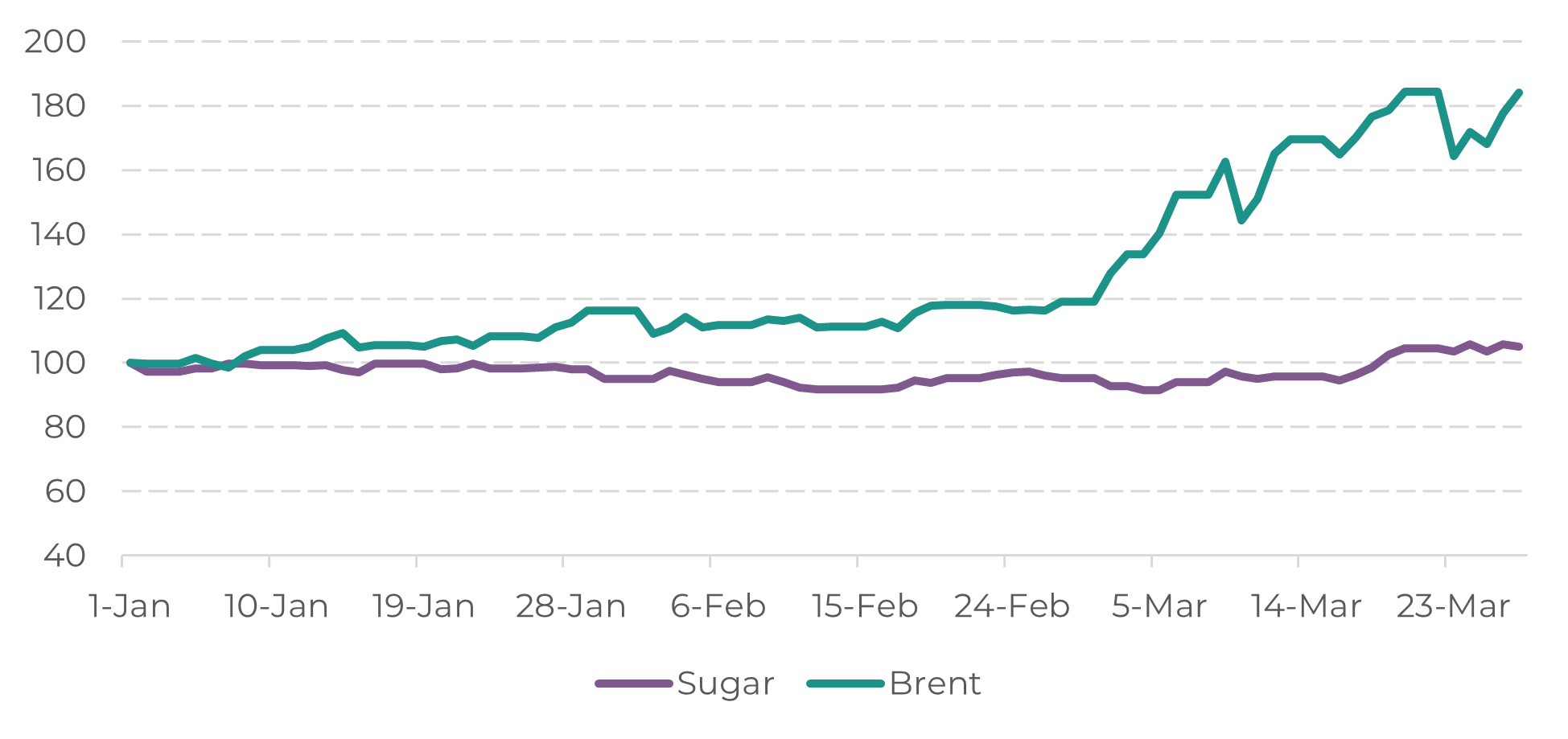

Figure 3 – Raw Sugar vs Oil Price Index (Jan 1st =100)

Source: LSEG, Hedgepoint

Summary

Sugar market fundamentals remain broadly unchanged, with attention shifting to supply developments, particularly Brazil, where supportive weather and stable UNICA’s estimates reinforce a bearish outlook. Price action has been driven mainly by speculative short covering and external factors, notably elevated energy prices linked to the escalating US–Iran conflict, which have supported sugar through cost spillovers and ethanol parity. As a result, prices are consolidating in a fragile 15.4–15.9 c/lb range, already reflecting expectations of a lower sugar mix, with upside dependent on sustained energy support and downside risks tied to conflict resolution and limited cost pass-through by Petrobras.

Weekly Report — Sugar

Reviewed by Laleska Moda

laleska.moda@hedgepointglobal.com

Disclaimer

This document has been prepared by Hedgepoint Schweiz AG and its affiliates (“Hedgepoint”) solely for informational and instructional purposes, without intending to create obligations or commitments to third parties. It is not intended to promote or solicit an offer for the sale or purchase of any securities, commodities interests, or investment products.